yamuna is not yet consolidated

Also execution is not linear when i spoke to few biodiesel players. It is as per OMC schedule.

Disc : hold no position yet, evaluating

yamuna is not yet consolidated

Also execution is not linear when i spoke to few biodiesel players. It is as per OMC schedule.

Disc : hold no position yet, evaluating

in the area mentioned (paint shop) yes but the remaining field was still vacant. No civil works nothing yet. The yellow area (paint shop shed) had Civil work and steel columns setup already.

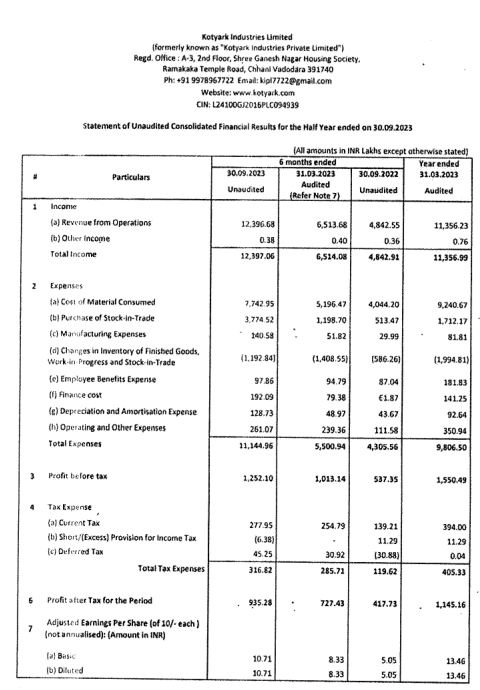

I do not think Yamuna is the reason. Company had announced two tender wins for Q1 and Q2. Even excluding Yamuna those tenders should have led to revenues of 270 crs (116 crs + 154 crs) for Kotyark standalone in H1. Against this expectation, the revenue was reported at Rs 124 crs. Goes to say that winning tenders doesn’t necessarily translate into revenues.

Also the CFO resignation is a dampener. In the last 15 months this is the fourth resignation of a KMP. Two company secretaries resigned within 3 months of each other (one in Jul 2022 and the other in Oct 2022). The earlier CFO resigned in Aug 2022. Goes on to say that the promoters might not be that easy to work with or there is something else behind the scenes.

Disc: exited my position today

From All time high to 16% down.

Kotyark has a wild day.

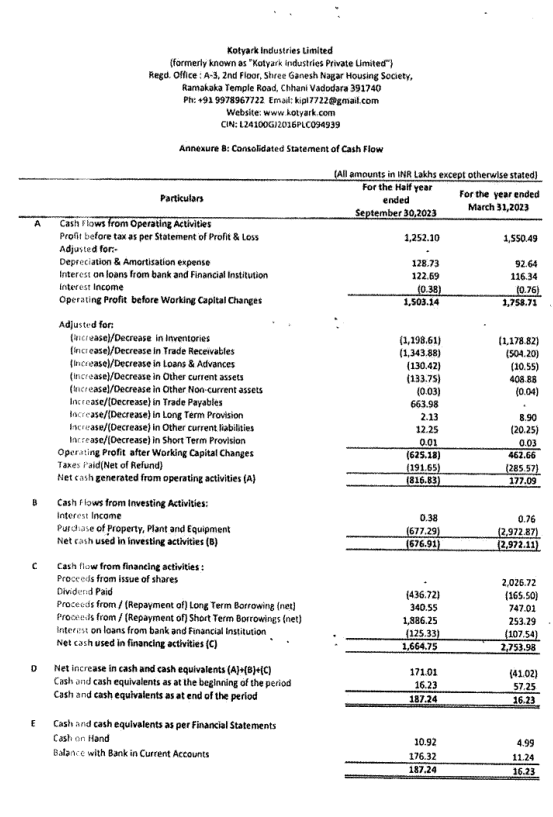

Profit & Loss looks good but Cash flow doesn’t look good.

Sales in current Half is more than PY whole year.

Reg_30_outcome_of_BM_30_oct_30102023134804.pdf (nseindia.com)

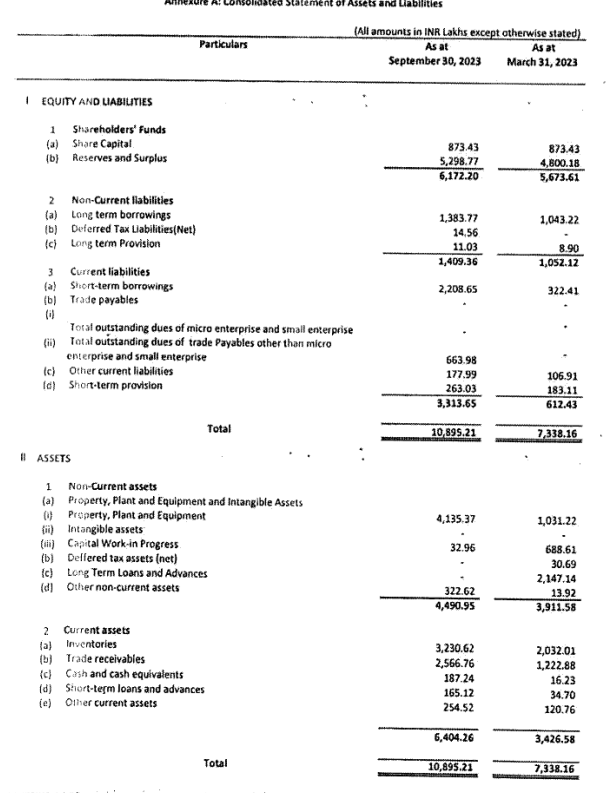

Capex is completed as per Balance Sheet.

Working cycle is absolutely stretched and funded by ST borrowings resulting in the increased Finance Cost.

NP ratio is lower.

Net Profit Ratio:

| H1 FY24 | H2 FY23 | H1 FY23 |

|---|---|---|

| 7.54% | 11.17% | 8.66% |

On Another Thought, the consolidation with Yamuna might be the reason.

Yamuna had high sales with very low margins.

I don’t know whether the related party approvals in AGM have already impacted the P&L in H1, but they shall definitely impact margins of H2.

If we compare batteries with Hy FuelCell or Hy ICE for mobility space.

The batteries have clearly won the race. With my limited understanding , Hy FC or Hy ICE wont be able to compete with batteris anytime soon.

Battery enjoys The economy of scale and chinese scale of manufacturing.

But both are fundamentally different technologies and Hy FC & ICE becomes necessary/advantageous over battery, for specific applications.

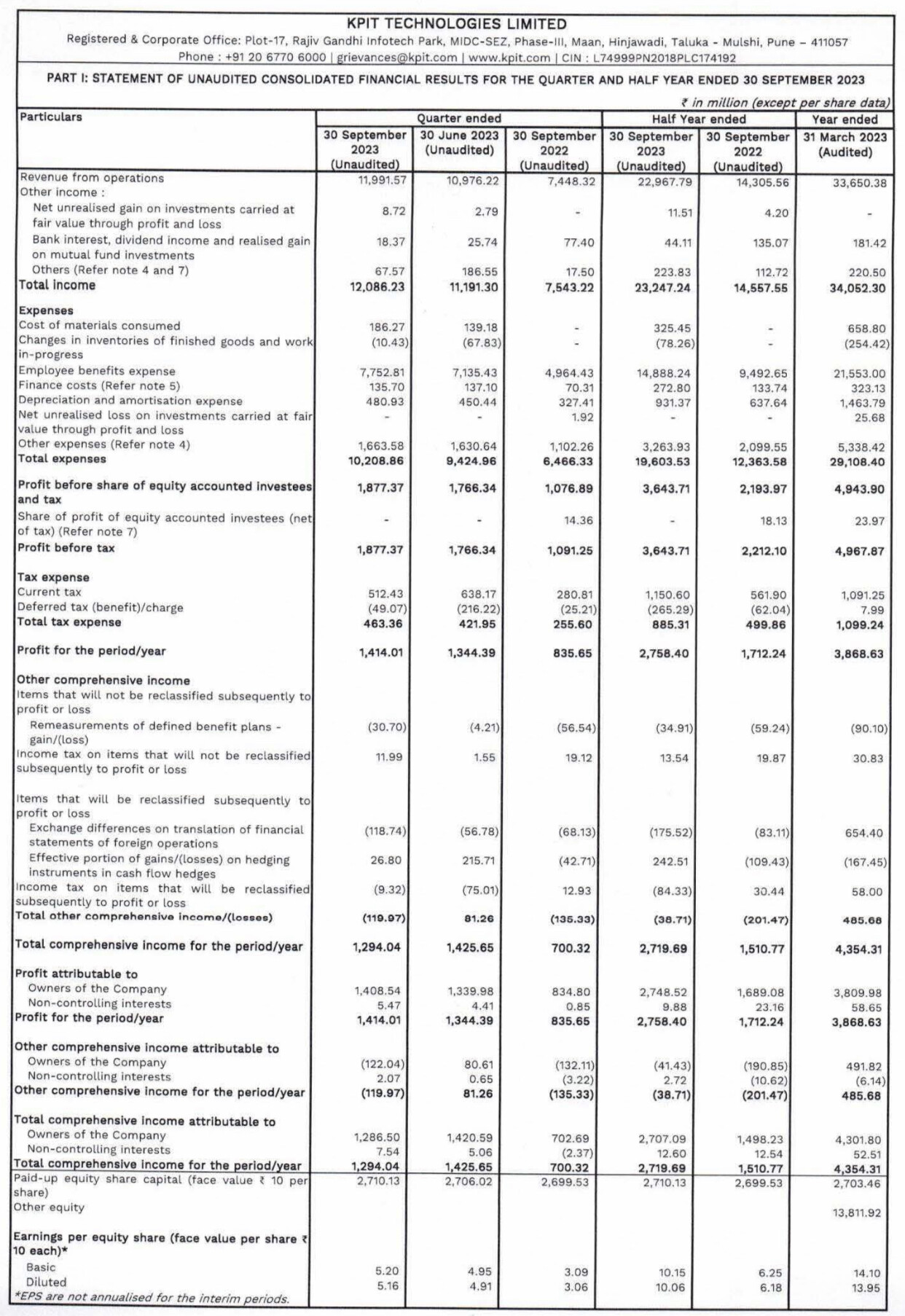

While LTTS results were flattish, KPIT delivers yet again. Keeps shining in the ER&D category

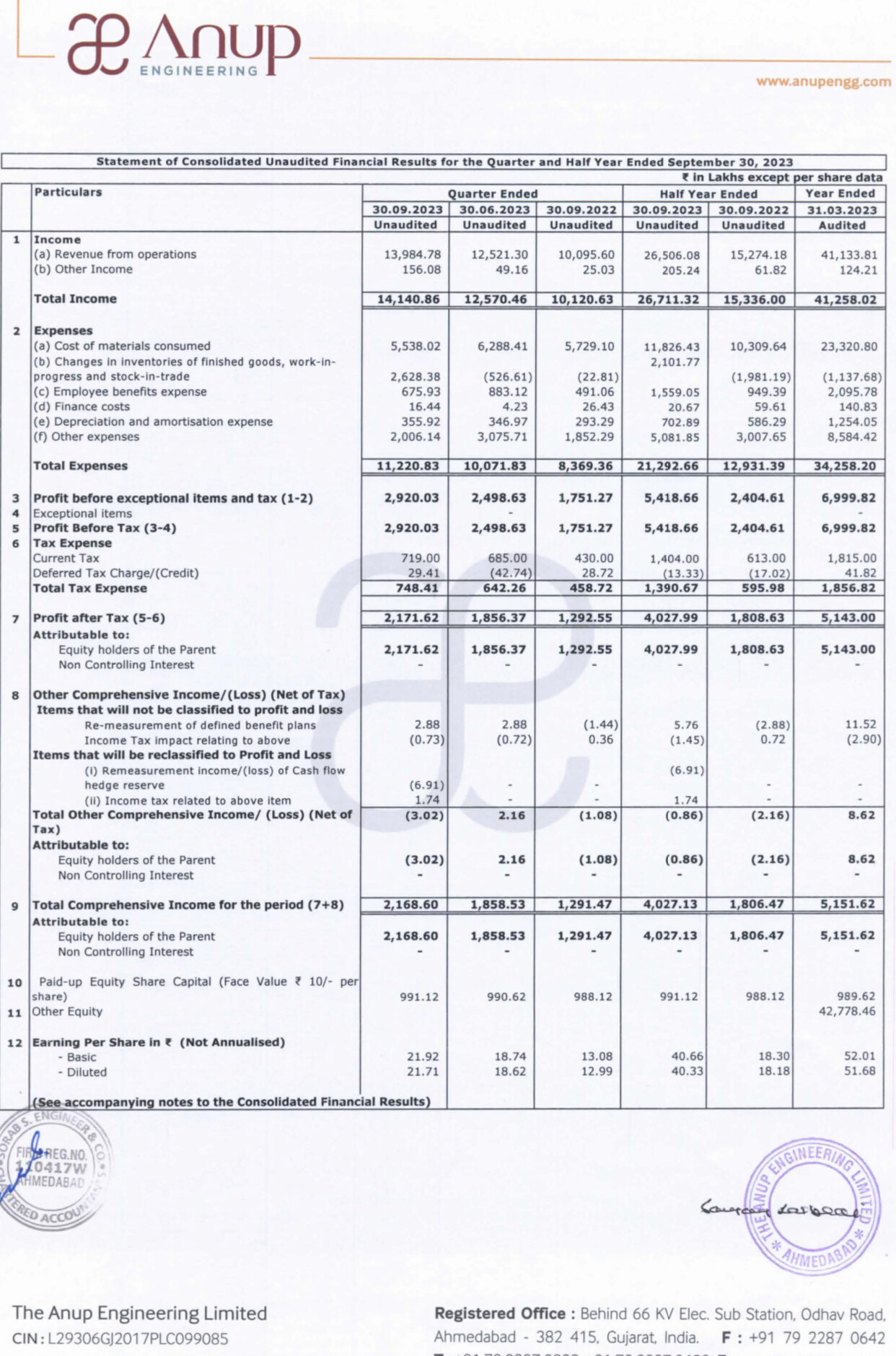

Brilliant set of numbers from Anup Engineering

Thanks for the plant visit update. In the greenfield area next to new painting unit, did you see any factory building construction coming up for next plant or is it still barren land?