SEBI has included all the required declarations in the Manual for RAs. When you start your application process, you will have access to the manual.

Posts tagged Value Pickr

How to register with SEBI as a Research Analyst? (30-10-2023)

SEBI has included all the required declarations in the Manual for RAs. When you start your application process, you will have access to the manual.

How to register with SEBI as a Research Analyst? (30-10-2023)

HI Gopi Krishna garu,

Thanks a lot for your immediate response,

I don’t sell Insurance products, Yes iam a Mutual Fund Distributor, also iam having franchise for Good will wealth management pvt ltd, deals with equity, currency and commodity segments, i had completed my NISM series 1, 5A, 7, 8, 10A, 15 and 17

Best Regards

Nukala Phani Krishna

9440051634

How to register with SEBI as a Research Analyst? (30-10-2023)

HI Gopi Krishna garu,

Thanks a lot for your immediate response,

I don’t sell Insurance products, Yes iam a Mutual Fund Distributor, also iam having franchise for Good will wealth management pvt ltd, deals with equity, currency and commodity segments, i had completed my NISM series 1, 5A, 7, 8, 10A, 15 and 17

Best Regards

Nukala Phani Krishna

9440051634

Ujjivan Financial – Small Finance Bank (30-10-2023)

Good question, one whose answer we will only get to know when the transformation is complete.

This is because the valuations are a factor of full cycle ROE/ROA and growth.

As the book becomes more secured, book yield will reduce, subsequently, NIMs will also contract, but across a full cycle credit cost, provisioning and LGD can also potentially reduce.

I write potentially because if one is doing risky lending in the secured segment the credit costs can still be high.

Modelling the above with incomplete information at the current juncture will not be right. There are a lot of moving parts.

The CEO is due to change, and while they may follow the direction of the old management which will be guiding from the BoD, the CEO could have their own direction as well.

If the “small” tag is removed, because they get a universal bank license, the OPEX, funding costs, and CAR, could change substantially.

Currently, the PAT, ROA, and ROE is at a cyclical high due to outlier credit costs. As the credit costs normalize next year the PAT may stagnate for that year (I use may because growth from the book will still be there, and higher NII will balance against higher provisioning costs), ROA, and ROE will reduce to cycle average, BVPS will keep growing.

How the market will react to the above is anyone’s guess, will it punish the valuations by focusing on PAT, or will the sector be in euphoria due to the growth potential, and bad memory of new market participants about COVID, and DEMON losses? Who knows?

Lastly, there is always the risk of the cycle turning bad and credit costs being elevated. That can happen anytime and needs to be watched like a hawk always. But if the cycle doesn’t turn for a 5-year period, it could be a golden period from an investment return perspective.

Many fingurus, have a recency bias and have been calling a credit cycle top for the past year. They have even taken a small data point for DEMON, and COVID which were man-made outlier events and modelled that such shocks come every 3 years. Go figure. They forget to look at the cycles from the 2000s.

To conclude, I am not saying something bad can’t happen, it can at any time. But if they don’t you will miss the opportunity of a lifetime.

Valuation premium you need to judge what is being priced in. Post-COVID at 0.7 PB the market was overpricing risk, IMO at 3x 1yr FWD PB the market will be underpricing risk for a 25% growth CAGR.

2x 1yr FWD PB may be fair valuations for a well-run MFI, SFB IMO. Well-run means they are transparent in reporting, aggressive in recognising NPAs, and write-offs and quick to turn around as the collection efficiency bounces back. All of which Ujjivan has displayed since its inception in 2006.

Ujjivan Financial – Small Finance Bank (30-10-2023)

Good question, one whose answer we will only get to know when the transformation is complete.

This is because the valuations are a factor of full cycle ROE/ROA and growth.

As the book becomes more secured, book yield will reduce, subsequently, NIMs will also contract, but across a full cycle credit cost, provisioning and LGD can also potentially reduce.

I write potentially because if one is doing risky lending in the secured segment the credit costs can still be high.

Modelling the above with incomplete information at the current juncture will not be right. There are a lot of moving parts.

The CEO is due to change, and while they may follow the direction of the old management which will be guiding from the BoD, the CEO could have their own direction as well.

If the “small” tag is removed, because they get a universal bank license, the OPEX, funding costs, and CAR, could change substantially.

Currently, the PAT, ROA, and ROE is at a cyclical high due to outlier credit costs. As the credit costs normalize next year the PAT may stagnate for that year (I use may because growth from the book will still be there, and higher NII will balance against higher provisioning costs), ROA, and ROE will reduce to cycle average, BVPS will keep growing.

How the market will react to the above is anyone’s guess, will it punish the valuations by focusing on PAT, or will the sector be in euphoria due to the growth potential, and bad memory of new market participants about COVID, and DEMON losses? Who knows?

Lastly, there is always the risk of the cycle turning bad and credit costs being elevated. That can happen anytime and needs to be watched like a hawk always. But if the cycle doesn’t turn for a 5-year period, it could be a golden period from an investment return perspective.

Many fingurus, have a recency bias and have been calling a credit cycle top for the past year. They have even taken a small data point for DEMON, and COVID which were man-made outlier events and modelled that such shocks come every 3 years. Go figure. They forget to look at the cycles from the 2000s.

To conclude, I am not saying something bad can’t happen, it can at any time. But if they don’t you will miss the opportunity of a lifetime.

Valuation premium you need to judge what is being priced in. Post-COVID at 0.7 PB the market was overpricing risk, IMO at 3x 1yr FWD PB the market will be underpricing risk for a 25% growth CAGR.

2x 1yr FWD PB may be fair valuations for a well-run MFI, SFB IMO. Well-run means they are transparent in reporting, aggressive in recognising NPAs, and write-offs and quick to turn around as the collection efficiency bounces back. All of which Ujjivan has displayed since its inception in 2006.

Hitesh portfolio (30-10-2023)

Hi @hitesh2710

Firstly thanks a ton for the wealth of knowledge that you keep sharing Hitesh bhai. I have picked hbl following you and it has been an almost 3x in less than year timeframe

The way i look at the story now onwards-

- On revenue gront

Fy26 revenue at 2900 cr, and giving it a 6/7 price to sales, cagr over next 2.75 years (q2 is not yet out) is 32%/39%.while revenues could overshoot management estimates…management estimates are not conservative as well. Hbl has developed capabilities through r&d but their execution capabilities are yet to be established. - On pe front…going by management guidance of 18% ebida on fy26 revenues,and assuming interest +depreciation of 60 cr pat is 350 cr. At 50 pe ,returns are 32%

Hence am expecting a 30%-35% cagr provided there is no negative surprise on revenue/margin.

Company being in twin positives of ev/ defense ensures buzz stays for some time…however i am not able to assign >7x price to sales.

Would be keen to understand your view on the story going forward.

Hitesh portfolio (30-10-2023)

Hi @hitesh2710

Firstly thanks a ton for the wealth of knowledge that you keep sharing Hitesh bhai. I have picked hbl following you and it has been an almost 3x in less than year timeframe

The way i look at the story now onwards-

- On revenue gront

Fy26 revenue at 2900 cr, and giving it a 6/7 price to sales, cagr over next 2.75 years (q2 is not yet out) is 32%/39%.while revenues could overshoot management estimates…management estimates are not conservative as well. Hbl has developed capabilities through r&d but their execution capabilities are yet to be established. - On pe front…going by management guidance of 18% ebida on fy26 revenues,and assuming interest +depreciation of 60 cr pat is 350 cr. At 50 pe ,returns are 32%

Hence am expecting a 30%-35% cagr provided there is no negative surprise on revenue/margin.

Company being in twin positives of ev/ defense ensures buzz stays for some time…however i am not able to assign >7x price to sales.

Would be keen to understand your view on the story going forward.

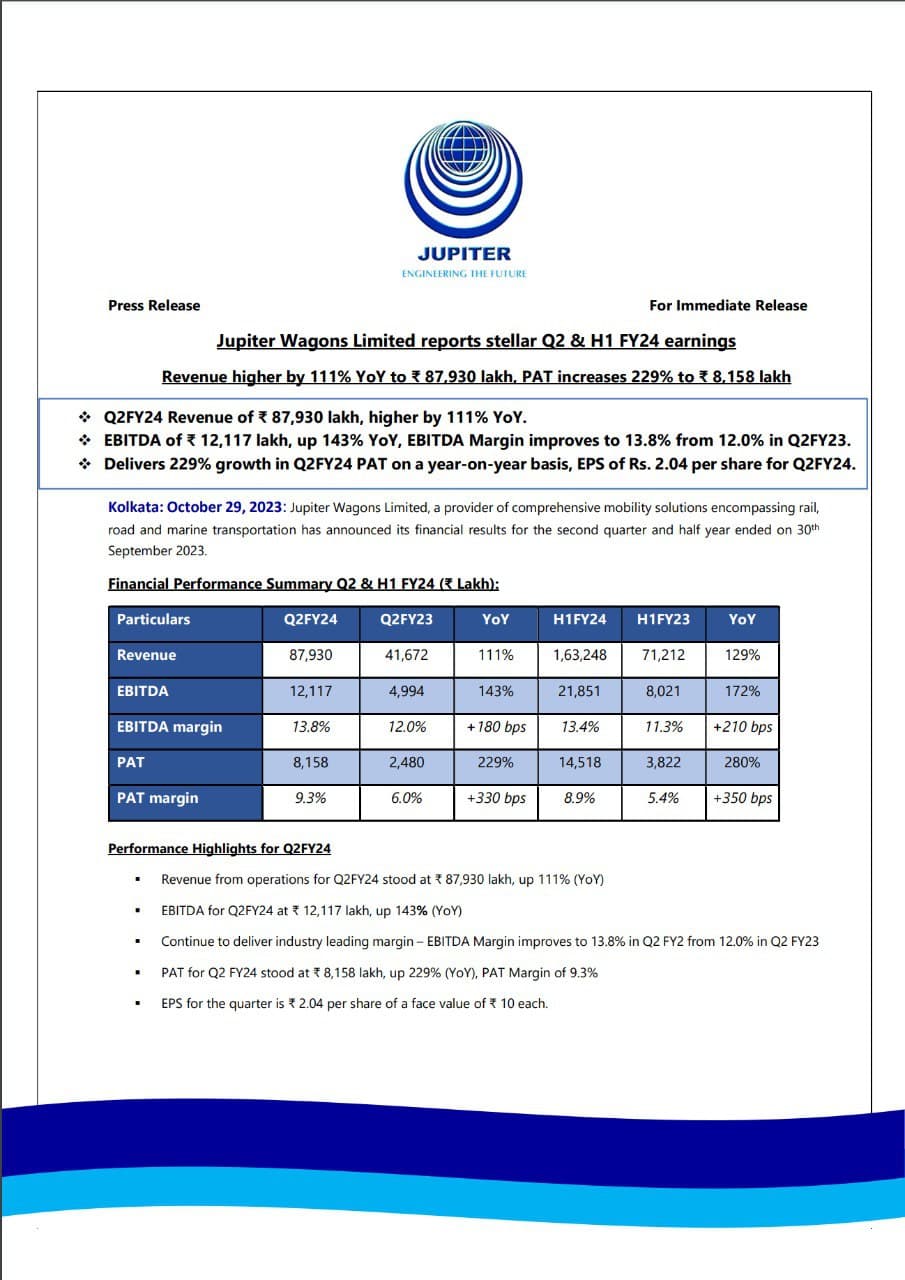

Jupiter Wagons Ltd (previously CEBBCO) (30-10-2023)

Jupiter Wagons Limited has released its financial results for the second quarter (Q2) and half-year (H1) of the fiscal year 2023-24.

Financial Performance (Q2 & H1 FY24):

- Revenue for Q2FY24 increased by 111% year-on-year (YoY) to ₹87,930 lakh.

- Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) for Q2FY24 increased by 143% YoY to ₹12,117 lakh, with an EBITDA margin of 13.8%.

- Profit After Tax (PAT) for Q2FY24 increased by 229% YoY to ₹8,158 lakh, with a PAT margin of 9.3%.

- Earnings Per Share (EPS) for Q2FY24 was ₹2.04 per share.

Performance Highlights for H1FY24:

- Revenue for H1FY24 increased by 129.2% YoY to ₹1,63,248 lakh.

- EBITDA for H1FY24 increased by 172% YoY to ₹21,851 lakh, with an EBITDA margin of 13.4%.

- PAT for H1FY24 increased by 280% YoY to ₹14,518 lakh, with a PAT margin of 8.9%.

- EPS for H1FY24 was ₹3.66 per share.

Outlook and Key Developments:

- The company continues to experience strong demand in the production of wagons for both public and private customers.

- Capacity expansion is planned for the foundry in Kolkata and a new foundry in Jabalpur, which is expected to yield cost savings in freight expenses.

- The Indian Railway tender for 20,000 wagons has been issued, and production capacity is set to increase.

- Stone India is expected to initiate operational activities in Q4FY24.

- Electric Mobility vehicle testing is scheduled for November, with commercial launch planned for the fourth quarter of the fiscal year.

Jupiter Wagons Ltd (previously CEBBCO) (30-10-2023)

Jupiter Wagons Limited has released its financial results for the second quarter (Q2) and half-year (H1) of the fiscal year 2023-24.

Financial Performance (Q2 & H1 FY24):

- Revenue for Q2FY24 increased by 111% year-on-year (YoY) to ₹87,930 lakh.

- Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) for Q2FY24 increased by 143% YoY to ₹12,117 lakh, with an EBITDA margin of 13.8%.

- Profit After Tax (PAT) for Q2FY24 increased by 229% YoY to ₹8,158 lakh, with a PAT margin of 9.3%.

- Earnings Per Share (EPS) for Q2FY24 was ₹2.04 per share.

Performance Highlights for H1FY24:

- Revenue for H1FY24 increased by 129.2% YoY to ₹1,63,248 lakh.

- EBITDA for H1FY24 increased by 172% YoY to ₹21,851 lakh, with an EBITDA margin of 13.4%.

- PAT for H1FY24 increased by 280% YoY to ₹14,518 lakh, with a PAT margin of 8.9%.

- EPS for H1FY24 was ₹3.66 per share.

Outlook and Key Developments:

- The company continues to experience strong demand in the production of wagons for both public and private customers.

- Capacity expansion is planned for the foundry in Kolkata and a new foundry in Jabalpur, which is expected to yield cost savings in freight expenses.

- The Indian Railway tender for 20,000 wagons has been issued, and production capacity is set to increase.

- Stone India is expected to initiate operational activities in Q4FY24.

- Electric Mobility vehicle testing is scheduled for November, with commercial launch planned for the fourth quarter of the fiscal year.