Margin expansion is huge which can lead to re-rating, it has had lumpy margins , are this one time margin? Remains to be seen. But great nos

Posts tagged Value Pickr

Avantel (09-10-2023)

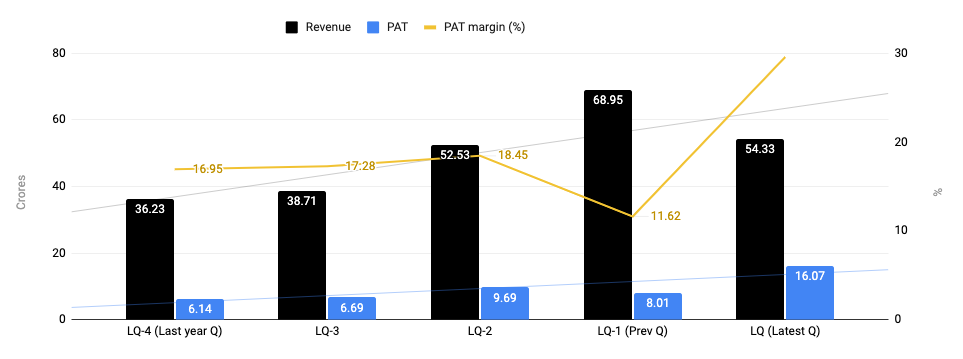

Apart from what @aceinvestor_75 already shared, here are other noteworthy things from consolidated Q2 FY24 results:

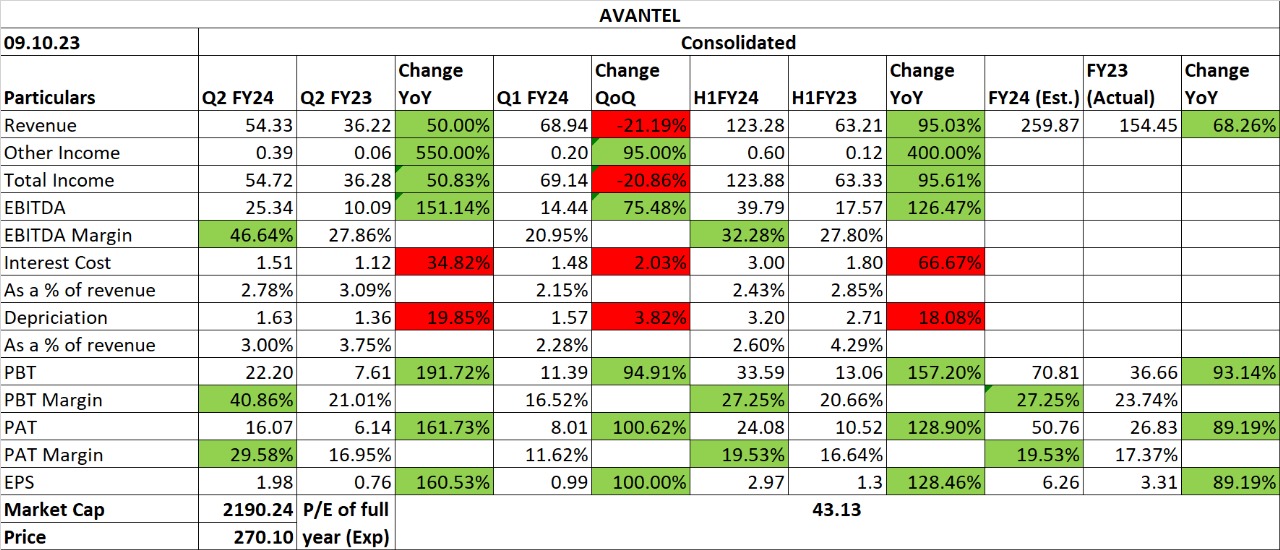

- Cost of materials consumed was significantly down from 41% to 26% YoY

- Overall expenses down from 83% to 60% YoY

- Revenue up 50% YoY and down 21% QoQ

- PAT up 161% YoY and 100% QoQ

- PAT margin at 29.6% vs 27% YoY and 11.6% QoQ

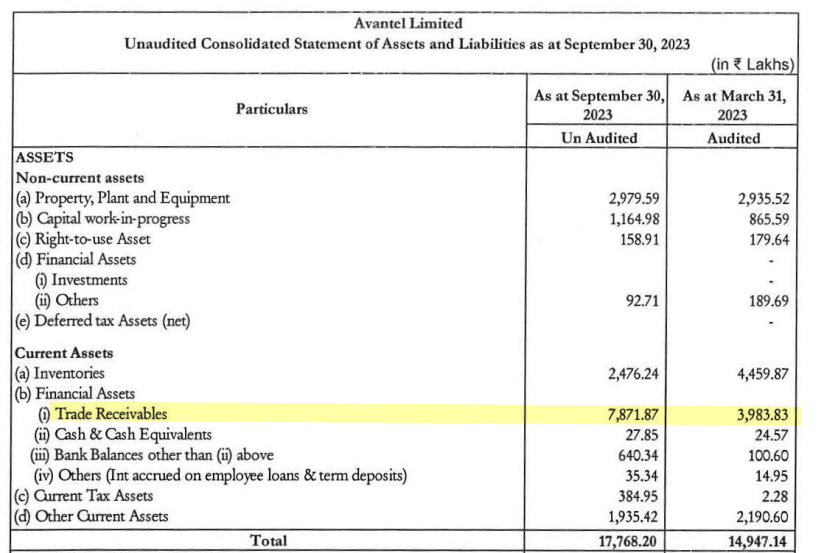

- Current assets show Trade Recievables of 78.72Cr (44% more than this Q2 sales) which should hopefully materialize in the upcoming quarters for this FY.

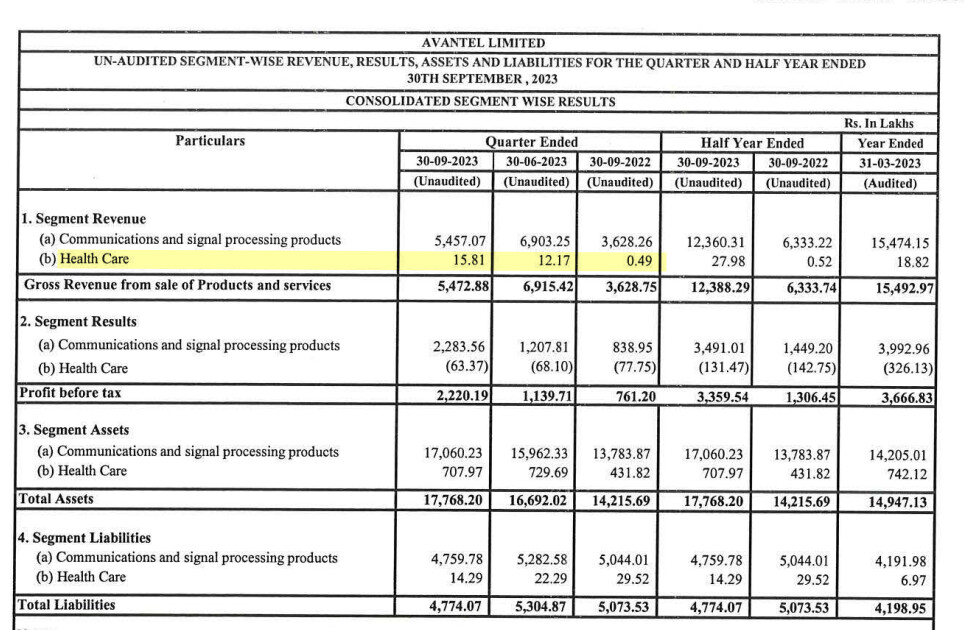

- Revenue from Imeds Global was miniscule (~16 Lakhs).

My takeaways

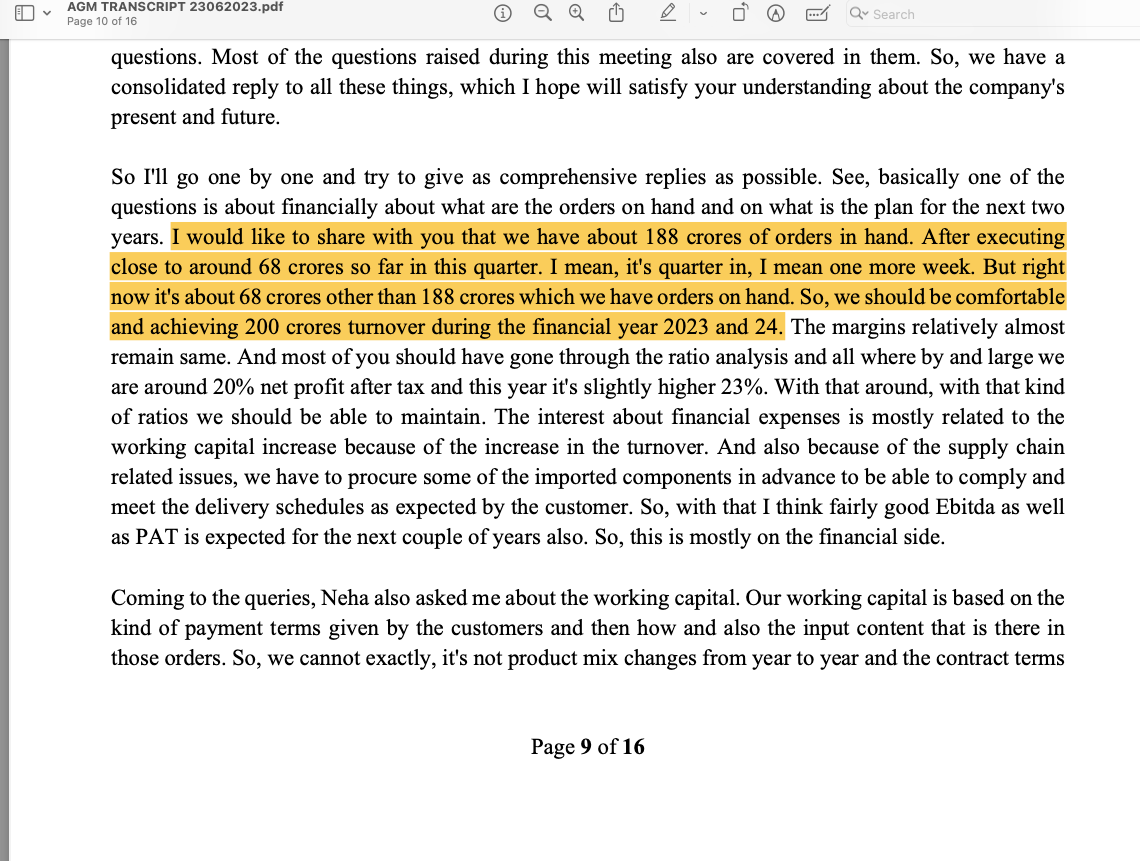

- The TTM revenue for FY24 seems on the path to achieve the guidance of 200Cr (+). Here’s what management had said in AGM held in June 2023.

- On the Imeds Global front, since it is still in a nascent stage and they’re working on getting necessary approvals, certifications, etc. think that biz would hopefully start contributing in a meaningful manner only from the next financial year as per management’s commentary in June 2023 AGM.

Va Tech Wabag (09-10-2023)

on the 3rd page of digital magazine, details are given for subs and everything, just go through that. Actually I am fixed to Magzter Gold subs, which is one of the best source for many magazines, so I read digitally on iPads, hope it helps

Niyogin Fintech Limited – Real problem solver of small business (09-10-2023)

Niyogin Fintech Limited

BSE 538772

CMP 61.70/- on 31.07.2023

CMP 67.70/- on 03.10.2023

Sanskrit word for “empowerment” niyogin was incorporated with a deep understanding of real daily problems of small businesses!!!

Shareholding

Peomoters 39.60%

Institutions 13.19%

Public 47.20%

Financials

FY23’vs Q1 FY24

Revenue in Cr 117.20 vs 45.50

EBITDA in Cr ( Loss) 21.20 vs 4.3

% -18.10% vs -9.01%

EPS in Rs -1.90 vs -0.50

23.08.2023

The company has issued share warrants 175,36,011 @ 45.62 to marquees investors

1st tranch of ₹ 20 Cr and balance within 18 months

Q1 FY 24 presentation and concall

FY 25 Guidance

~ Revenue Rs 500 Cr

~ EBITDA 10-12%

~ BaaS 1.5 to 2 Mn

~ Target outstanding loan Rs 250;Cr ( Current Rs 117 Cr)

~ GTV 100000 Cr

~As on date Gross take rate 36bps and Net take rate 9bps

~GTV of the Quarter 9893 Cr and expected at Q2 11500 Cr

~IservU partners 796

~ Avg transaction size Rs 2943/-

Q2 and H1 business update: 03.10.2023

H1 and Q2: Rs.21455.7 Cr and Rs 11562.7Cr✓

Number of transactions: 4.2 Cr

Gross Loan book: Rs 135.3 Cr

Paushak Ltd. – Alembic’s agrochemical business (09-10-2023)

If any update related to this stock then please let me know

Genus Power – Smart Metering (09-10-2023)

Genus Power Infrastructures wins order worth Rs 3,115.01 cr (net of taxes)

Total order book now stands at over Rs. 14,000 crore (net of taxes)

Indian Energy Exchange (IEX) (09-10-2023)

Indian Energy Exchange to acquire 10% in Enviro Enablers India Pvt Ltd (EEIPL)

Under this agreement, IEX will acquire a 10 per cent stake in EEIPL through Compulsory Convertible Preference Shares (CCPS). This strategic move aligns with IEX’s commitment to sustainability and decarbonisation, in accordance with India’s net-zero commitments and to promote a circular economy, the company stated in a press release.

What does Enviro Enablers India Pvt Ltd (EEIPL) do?

EEIPL incorporated incorporated on 21st October 2021 is engaged in the business of waste management by collection, segregation, processing and transportation of dry waste, plastic waste, and all categories of waste including but not limited to organic waste, expired FMCG waste, electronic waste, construction and demolition waste, hazardous waste, agro waste, tyre waste, solar PV module waste and end of life vehicles waste, and proposes to develop and operate a digital Material Waste Platform which would connect industry participants in the waste management process.

Comments from IEX Management: Mr. SN Goel, Chairman and Managing Director of IEX

IEX is proud to associate with Enviro Enablers and to partner in this circular economy platform. This partnership reaffirms our steadfast commitment to sustainability and decarbonisation, aligning seamlessly with India’s net-zero goals. The platform will catalyse solutions for compliant waste management, including segregation, processing, recycling, tracking, tracing, and valorisation of waste fractions, all while uplifting informal waste pickers.”

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/dd7394c8-d3ba-43cd-8dc8-d02d4d351c63.pdf

Avantel (09-10-2023)

Avantel Blockbuster Q2FY24

Rev gr yoy 50%

Opm yoy 41% v/s 21%, qoq 17%

Eps 1.98 v/s 0.76 yoy, qoq 0.99

Ocf 33.6 cr for H1FY24, 36.7 cr for FY23

Significant inventory reduction

Bonus 2 shares for every 1 share held

Cosmo Films – Diffentiated player in commodity business (09-10-2023)

Hello Jiten, have been reading some of your comments and additions of cyclical commodities since a few days now , I have recently joined in and just learning as much as possible.

Coming to my question at hand how is your holding in cosmo films currently, and knowing you are working in the flexible laminates space do you still stand by your views from 2016 about cosmo films.

I am trying to learn this company more and more and learning about its capex growth in the last few years and seeing how the company is of a cyclical nature , current levels seem very attractive to capture the upcycle move, similarly the charts also show a good cup formation, ideally seeing the sector it had its peaks in 2016-17 then 20-21 and looks like it might pick up again , profit margins of the company and how they have been moving for competitors (nahar poly, jindal poly , polyplex, uflex) seem to be responding in tandem with the cyclical nature hence hinting an upward soon.

Could you please share your views on this?