so indirectly ashirwad price will affect manappuram price

Posts tagged Value Pickr

Manappuram Finance (05-10-2023)

This is not a demerger. Ashirvad is a subsidiary of Manappuram. Currently manappuram holds 98%. Now Ashirvad is going to raise fresh equity from open market worth of 1500 crores. This will be issued to new investors. So as a manappuram shareholder, you will not get ashirvad shares

Manappuram Finance (05-10-2023)

Yeah I have the same question

Edelweiss Financial Services (05-10-2023)

I needed more clarity on their business financials. Usually companies dress up their financials prior to an IPO, I wanted to get a full year data prior to taking a stance on its return metrics and valuation.

As well I took a calculated gamble of there being some selling pressure initially in Nuvama because of the quantum of investors who had invested in parent co Edelweiss just to unlock value from Nuvama.

Nuvama has a lot of equity capital invested in itself and so far hasn’t delivered proportionate returns as compared to some of its peers. Hence, I felt for now, till there’s clarity on its financials and return ratios, it does not deserve to trade at these valuations.

However, having said that, Edelweiss Wealth is a very old player in the industry, has some of the best talent working for them and now has an international parent with deep pockets with resources to support its growth. Hence, once there’s clarity and the selling pressure is absorbed, I’ll look to buy again

Suryoday small finance bank (05-10-2023)

2QFY24 Provisional numbers show sustained improvement across all parameters. Management commentary indicates disbursements growth on back of Vikas and Retail Loans.

CoF increased further by 40bps.

Disclaimer: Invested and Biased.

52 week highs and all time highs strategy (05-10-2023)

Supreme Petro

Technicals : at all time high.

Funda: 1.have 60 % market share in HIPS after shutdown of LG in 2020

2. almost 100% market for XPS and EPS

3. Entering ABS resin space which has 40% imports currently and balance supplied by Bhansali and old worn out bayer plant currently run by styrenix.

4. proven partnership management of taparia and raheja, wherein taparia increased stack by 4%

5. professionally run company.

6. stable demand for AC/washing machine/home appliance over next three to four years will keep resin demand going

Negative:- 1.available at 25 PE compare to historical avg of 12.

2, international over supply can spoil the show, commodity product.

Question:- can those three (one big and two small qualify as cup and handle and can this be a case to be considered as all time high candidate worth investing?

reply and comments highly appreciated

discl: invested

Edelweiss Financial Services (05-10-2023)

At 380 cr PAT- it is available at 20 PE, which seems ok. Any specific reason why you sold Nuvama after demerger?

Listed Microcap- Frog Cellsat- Opportunity (05-10-2023)

Notes from Frog Cellsat Limited from the Annual Report 2022-23

-

Frog has ventured into defense projects

-

Its new manufacturing facility in Noida marks an increase in capex, enabling full-fledged operations by Q1 FY2024

-

Certified by the Department of Science and Industrial Research (DSIR) Government of India.

-

New CEO appointed – Mr. Pankaj Gandhi as the CEO of Frog Cellsat Ltd., effective May 2023. ( Professional Management – a positive)

Capex:

-

Phase 1 construction of the new manufacturing facility in Noida, covering 100,000 sq. ft., signals increased capex.

-

Full-fledged operations begin in Q1 FY2024.

-

Phase 2 construction (60,000 sq. ft.) is ongoing and expected to complete by Q3 FY2024.

-

Increased hiring expenses as they see growth in the next few years

-

No Revenue Growth but 100% debt free company

In FY2023, Frog clocked revenues at 1,33 Cr, which is relatively at the same level of 132.9 Cr million in FY22

- FY24 Guidance –

Revenue is expected to grow in the range of 45% to 50% in FY2024,

EBITDA margins are expected to be in the space of 16% to 18% for FY2024 vs 16.48% in FY23

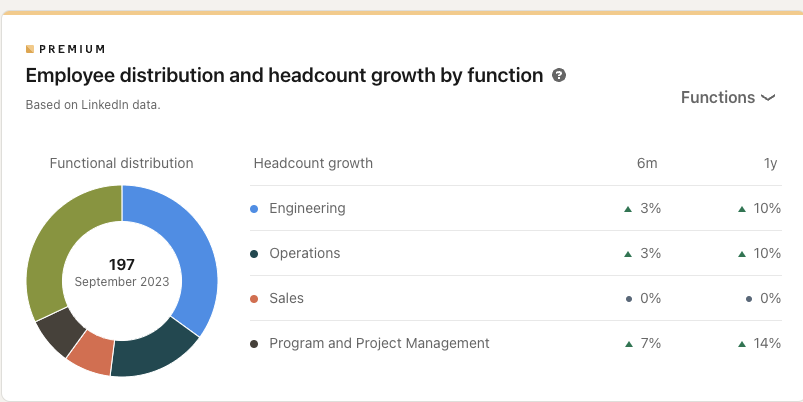

- Employee benefits: ( 151 employees as of March 2023 / 197 as perLinkedIn 5th Oct 2023)

The Company extends assistance for education of children of the employees. Shiksha Sahyog Policy

Median employee tenure ‧ 6.2 years (LinkedIn)

Red Flags:

-

Promoters has issued shares to themselves for almost free before the IPO: 225 (Two Hundred and Twenty-Five) new equity share for every 1 (One)

-

Production Linked Incentives are recognized as income when on the basis of the judgment of the management

-

There are several litigations pending for the inventory filed by the Company

-

TDS default for previous years amounting to Rs 5.99 lacs

-

They are getting into defense/government projects so the payment cycle will increase

Things to monitor:

-

Revenue Growth guidance that management has given can be achieved , very aggressive

-

Track related party transactions as they do have a few

-

They are eligible for and get PLI incentives from the government in the next FY

-

Progress and deliverables from the new Noida plant from Q1 FY2024 onwards

PPFAS Financial Opportunities Forum (05-10-2023)

95% is too high an allocation. I will suggest at least 35% should be moved to large and flexi cap,20% to mid cap and remaining 40% in small cap. It will ensure 20% annual return, as you will have 60% in pure mid and small cap, in addition to it some flexi cap funds may have good exposure in small and mid caps.It will minimise the risk as well.Of course, a lot depends on the individual’s specific circumstances.If someone doesn’t need money for next five years at all, then even the present allocation is fine. I have shared my allocation and approach (funds and stocks) as per my situation, as I am full into funds and stocks so I need to care of all sorts of financial requirements through this market. As mentioned in the last post, in last 20 years approx. I did not face any major problem, at the same time the growth has been satisfactory.

Aarti Drugs (05-10-2023)

(post deleted by author)