They have surplus land along with permission to extend the room count which is very good sign. Also Whitefield is prominent location for IT in Bengaluru.

Posts tagged Value Pickr

Samhi Hotels – Turnaround with Tailwinds (05-10-2024)

The property could be poorly managed and Samhi could bring efficiency and utilise the property efficiently to maximise the revenue.

Samhi Hotels – Turnaround with Tailwinds (05-10-2024)

Is Samhi hotels paying too much given the turnover is only 24cr but they are paying 205 Cr?

Burger King ~ Whopper of an Opportunity (05-10-2024)

Newer assets and contionous new stores opening up is the reason for higher depriciation.

Supreme Industries (05-10-2024)

I recently watched a podcast of a senior analyst from Nuvama where she mentioned about the value chain of Pipes and fitting industries.

Insights I got:

Pipes and fittings is a bulk industry where the bigger player is getting and the smaller player is getting smaller. So the question comes in mind, why is this happening? The major raw material for pvc pipe is PVC resins and the major suppliers of resins are likes of reliance industries, Chemplast; and when big companies such as supreme or astral goes to procure resins from reliance, they have a bargaining power, incremently they can procure it at 2-3% discount. This reminds me of the moat of APL Apollo where they purchase raw material at a marginal discount rate from the Iron n Steel players. And on the other hand, small players lack this bargaining power, at first they can’t directly go to Reliance or Chemplast to procure resins, they have to procure via distributers and in this chain distributer wll have a cut of 3-4%.

Additionally being a bulk material, that needs to be transported from plants to the retailers incurs significant logistics cost. And only big player, Supreme has plants in various parts of the country, they can save on logistics supplying it to the retailers, on the other hand small players lack this scale. This reminds me of Ultratech where the company have various plants all across the country. PVC pipings industry is a commoditised economies of scale business, where the lowest cost and the most efficient manufacturer is poised to well.

Supreme and Astral are clear leaders. This industry has witnessed the significant value migration from unorganised to organised. Supreme is guiding to increase its revenue at 25% CAGR where all other players are downsizing their estimates. The next leg of growth in this sector can come from introduction of OPVC pipes as government wants to replace DI Pipes by OPVC. Additionally, in western countries usage of plastic doors and window panels are common (made up of UPVC) this segment may gather momentum. Additing to this, the pipes used in Fire control systems is also poised to do well.

MSTC Ltd.: Growth through to E-Commerce (05-10-2024)

FSNL Highlights

FSNL has a networth of around 257 crores against which MSTC has realized Rs.320 crores.

Realization was assumed on higher side seeing the growth in last 3-4 quarters.

2. Coal India has started itz own platform as they are aware of their major customers. Major clients of MSTC seems to scrap dealers and PSU which is allowing them to fetch 40% of revenue. To have huge numbers of scrap dealers at various locations in India for online auctions seems to be MOAT for MSTC which i believe.

3. Vehicle Scrappage Policy is taking his own time to get implemented but it will be implemented in next 2-3 years .Till that time if MSTC is able to cater Government vehicles all over India, it should also reasonable topline to MSTC. On monthly basis the numbers are increase of vehicle scrappage.

4. Extract from transcript “So that is the organic growth of, finding more clients or finding more entities, who are into e-commerce of the kind of things that we already are doing. And apart from this, we have also been working at integrating services. So that is a separate line of business, which would be a somewhat inorganic growth, which would build upon what we are doing and are developing more upstream or downstream activities. So that’s two ways that one thinks of growing, which is what MSTC has also been.”

“It should start happening. The revenue stream should start happening from new initiatives in Q3 I mean, things that we are working on at this point of time, So Q3,Q4 onwards, there should be significant.” (extract of Transcript June 24)

“We have also embarked on a very ambitious plan for building and enhancing capacity in terms of domain expertise, both in terms of manpower and in technology. We are quite confident that this approach shall show tangible results, tangible benefits, in Q3, Q4 of FY 25.” (extract of Transcript March 24)

As per the commentary of Management ,Q3 /Q4 should be the period where some new business should materialize and sale of FSNL in Q2 seems to be that direction. It enables to have cash in the books for future opportunities.

New India Assurance Limited seems to selling spree in last many quarters and major sell off in last quarter may be from his end. Shareholding patters for Sept 24 will be key to watch.

Another Selling shareholder is Quant Mutual Fund in Aug 24 month which has been acquired in June 2024.

“I am just Eagerly waiting for Walk the Talk by CMD…”

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (05-10-2024)

As an investor in BCL, it has been a roller coaster ride this year. Below is a summary for anyone who wants to come upto speed with BCL:

Good

Company’s transition from Edible Oil to pure-play Green Energy continues with good momentum. Here is a summary of the declared plans for the next 2 years.

-

As per current disclosures, in around 2 yrs time, company will have 1100 KLPD Ethanol-ENA (current 700 KLPD), 150 KLPD Bio-diesel, 20 MTPD Bio-gas, plus country made liquor business

-

Edible oil business will be shut down in the next couple of quarters, required machinery will be moved to where the Distillery is located and land on which Edible Oil business is, will be sold. Proceeds (40+ crs) from that will help in bringing down debt or help in capex. Shuttering of Edible Oil business will also help in substantial reduction of working capital in addition to the proceeds from land sale.

-

75 KLPD Bio-diesel plant under construction in Bhatinda along with power plant, planned completion by 1st quarter next FY

-

150 KLPD of Ethanol plan under construction in Bhatinda, planned completion by 3rd quarter next FY

-

Another 75 KLPD Bio-diesel plant construction will start at the W.Bengal subsidiary once the first Bio-diesel plant stabilizes

-

Edible oil business has low single digit margins, while the Green energy business will have mid teens margins. Should help the company command better multiples than what it did in the past

Not so good

-

SEBI notice – no idea yet what it is about. Will try to get some info from IR.

-

Margin pressure (discussed above) – I believe it is a short-term phenomenon. Once new maize harvest comes, maize price should cool down. This year more area is under maize cultivation. Rice is rotting in FCI godowns but govt still not releasing it at subsidized rates like they did in past, for Ethanol is disappointing. Allowing companies to participate in e-auctions won’t help much due to high auction price

-

Promoter selling – for me promoter selling 1.6% when they hold ~60% stake is no biggie. Promoters sell for various reasons, buy only for one. When asked the reason for selling during the Arihant Rising stars conference, Mr. Kushal Mittal mentioned that his parents are over 60 yrs now and they needed money for personal/social obligations. He said that promoters have always put in money in the business when required, so recent sales shouldn’t raise too much concerns (not his exact words, but that’s what he implied)

-

Low cash flows – according to Management it is primarily due to Edible oil business constraints e.g. The flip-flopping govt policies related to custom duties, made it very difficult to plan inventory, often resulting in substantial inventory losses. Now, with EO business shuttering over next few quarters and major Distillery capex starting to generate returns at higher margins, cash flow should improve substantially.

Disclosure: Invested. No recommendation.

Burger King ~ Whopper of an Opportunity (05-10-2024)

Hey

Can anyone please help me understand why does burger king has so much of depreciation expense.

I observed they are generating positive operating cash flows but due to depreciation cost they are showing are loss ar bottom line.

They have 2300cr fixed assets and depreciation is around 350cr

Where as jubilant has around 6,000cr fixed assets and their depreciation is almost half than burger king

Can anyone please explain this ?

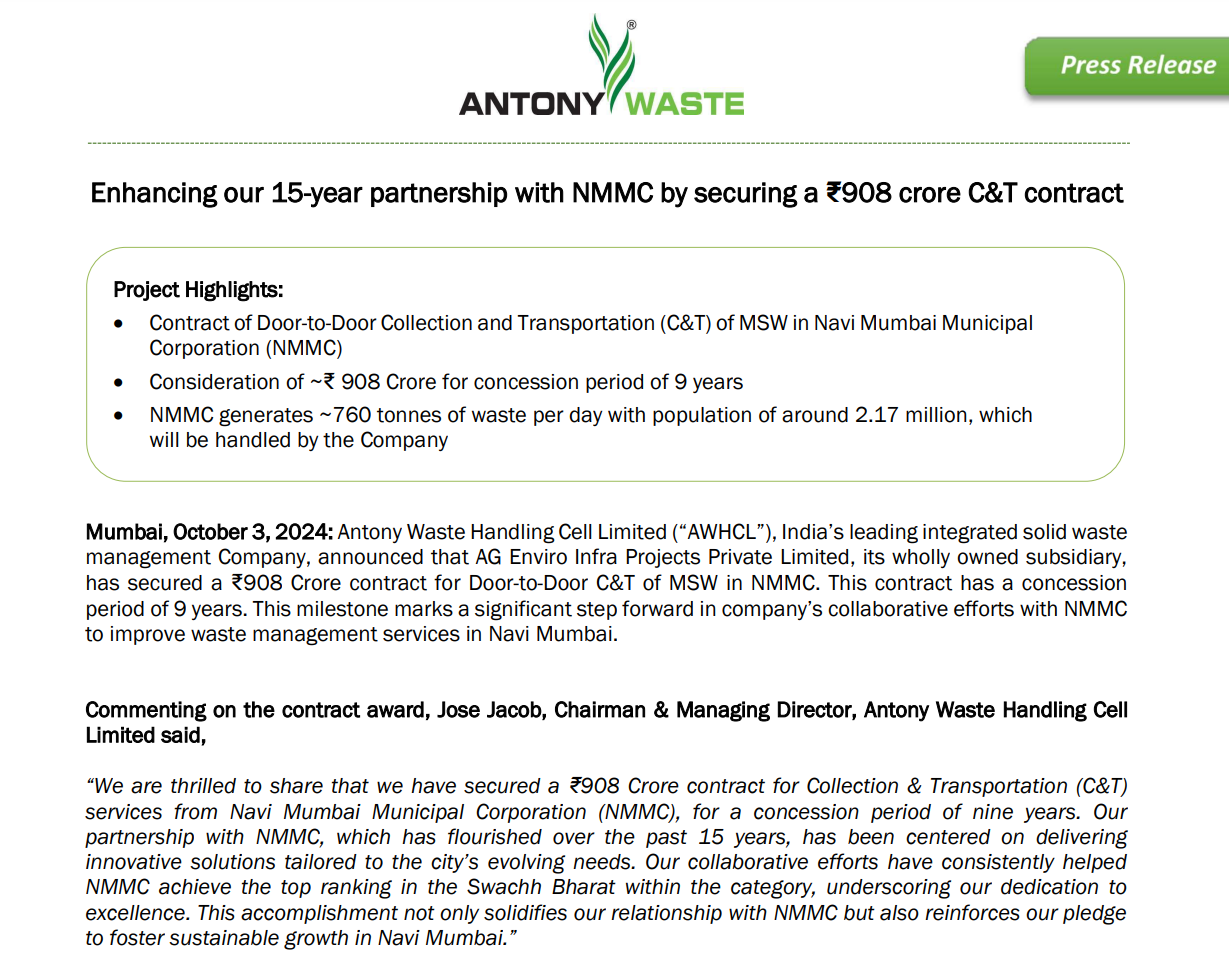

Antony Waste – Long Term (05-10-2024)

AG Enviro Infra Projects Private Limited, a wholly owned subsidiary of AWHCL wins Collection & Transportation project in Navi Mumbai for a period of 9 years. Total estimated contract value is 908 crores over period of 9 years.