@visuarchie yes…not getting any error now…Thanks a lot ![]()

Posts tagged Value Pickr

Microcap momentum portfolio (03-10-2024)

Schneider Electric Infrastructure: A global company with advantage of a industry tailwind: (03-10-2024)

As far as I’m aware, very few of these sophisticated equipments are manufactured in India right now. Schneider EU holds a significant market share and these machines are imported in India.

My Portfolio (Updates and Suggestions) (03-10-2024)

I might not be right but, just 2 cents if i were you, i would keep that much cash in hand in short term fd’s. (atleast 20%) since wedding is an expensive affair. So, your cash part is alright according to me.

The piece of land that you own is all upon you to access as to in how many years will it yeild a good return compared to any stock/mf investment you make.You might have bought it off dirt cheap and it would be great. Just take into consideration of your total capital gains tax that you might need to pay.

The crypto part, no comments,coz even i would have keep 0.2-1% of my wealth there…

Just on the stock/mf investments where i am more concerned for you.

If I were to invest into a nifty50 etf, why will i buy shares of the same holdings directly in my personal portfolio? both the places when i have the same bluechip stocks, dosen’t make sense… apart from keep let’s say 2-3.

Also, i cannot understand your equity investing thoughprocess. Since, i were to plan for a 30 year runway with enough cash, emergency fund & insurance. Good amount of mf investments, i would not invest majority of my wealth into companies with 50k+ cr in mcap…Since, the ability of compound/returns will be less than let’s say a midcap growing at 20-30%.

You might wana look here… And It would be better to cut down on irrelevant stocks unless you can track on all the investements you make. since, you might get busy with work and there personal commitments, will you be able to track all. (but then, here comes the comfort of having bluechip stocks, they are going nowhere ![]() )

)

I am a novice, don’t take anything as an investment advice. I am not SEBI registered.and i myself have made a lot of mistakes and might be wrong here as well.

Anant Raj Limited (03-10-2024)

A few details that can help us understand if the management is building data centers as per the standard-

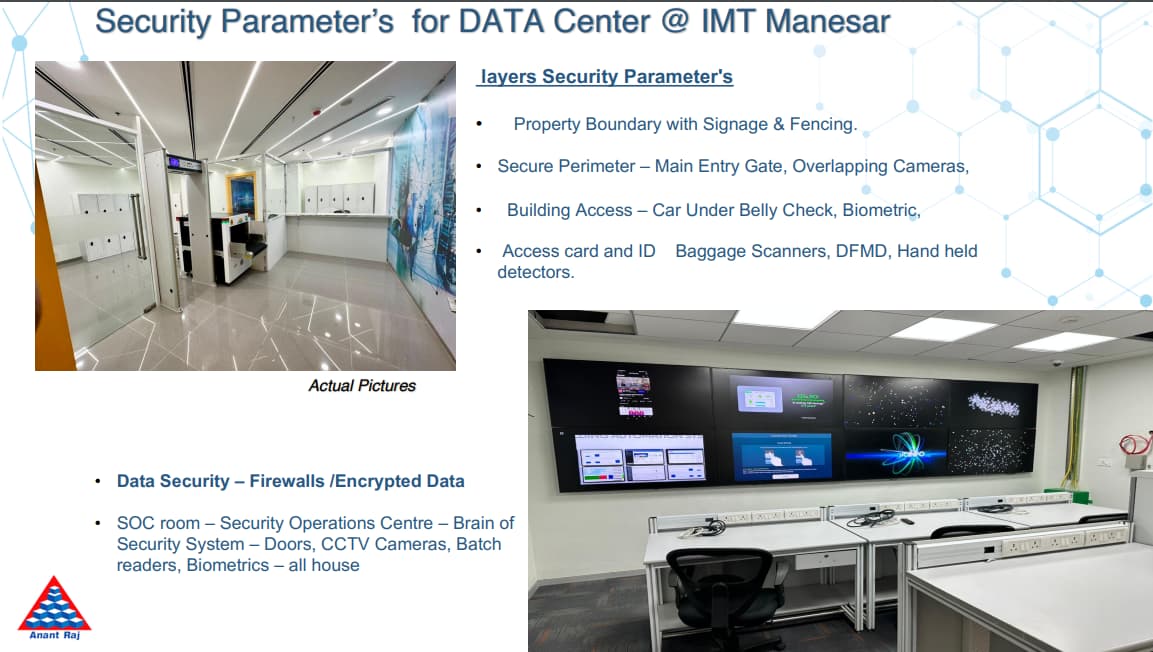

- Strict security levels (vehicle under belly check, face detection cameras, etc)

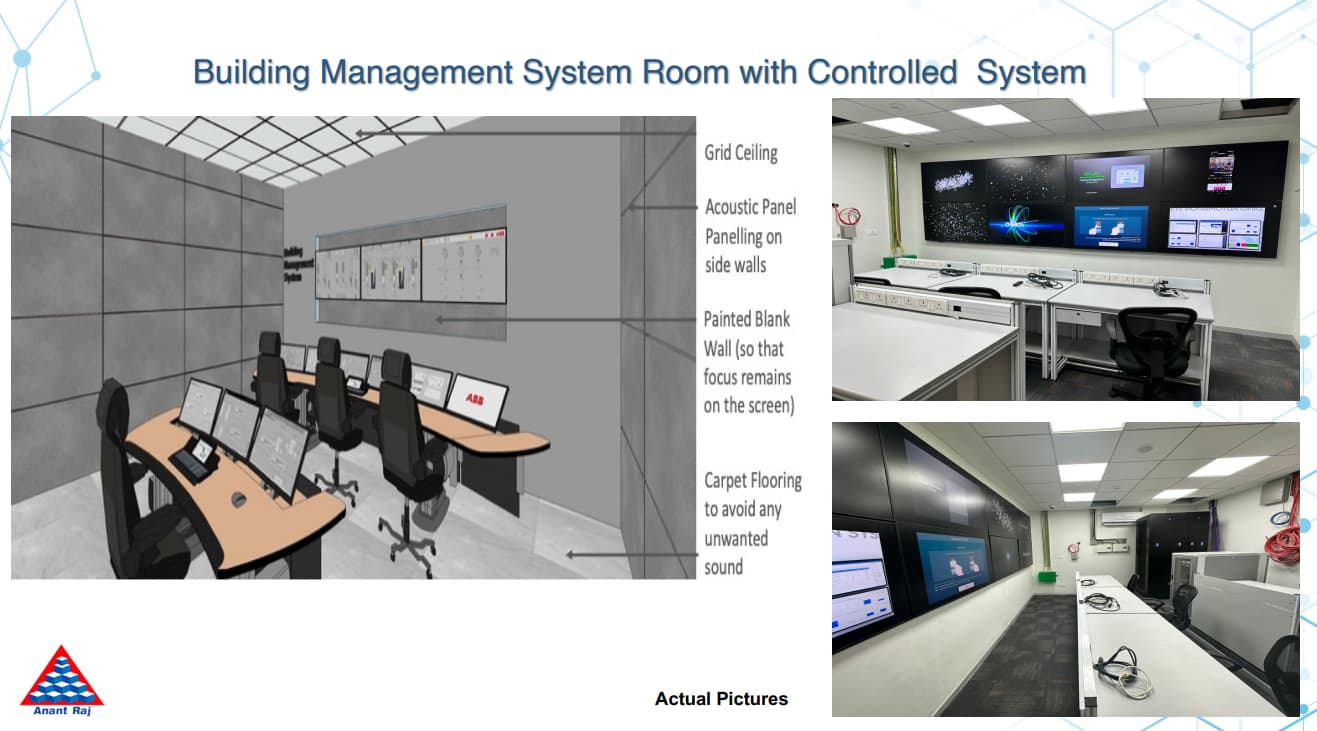

- Building monitoring systems(BMS) room

- Management system room

- Diesel Generators and fuel storage for emergency power backup

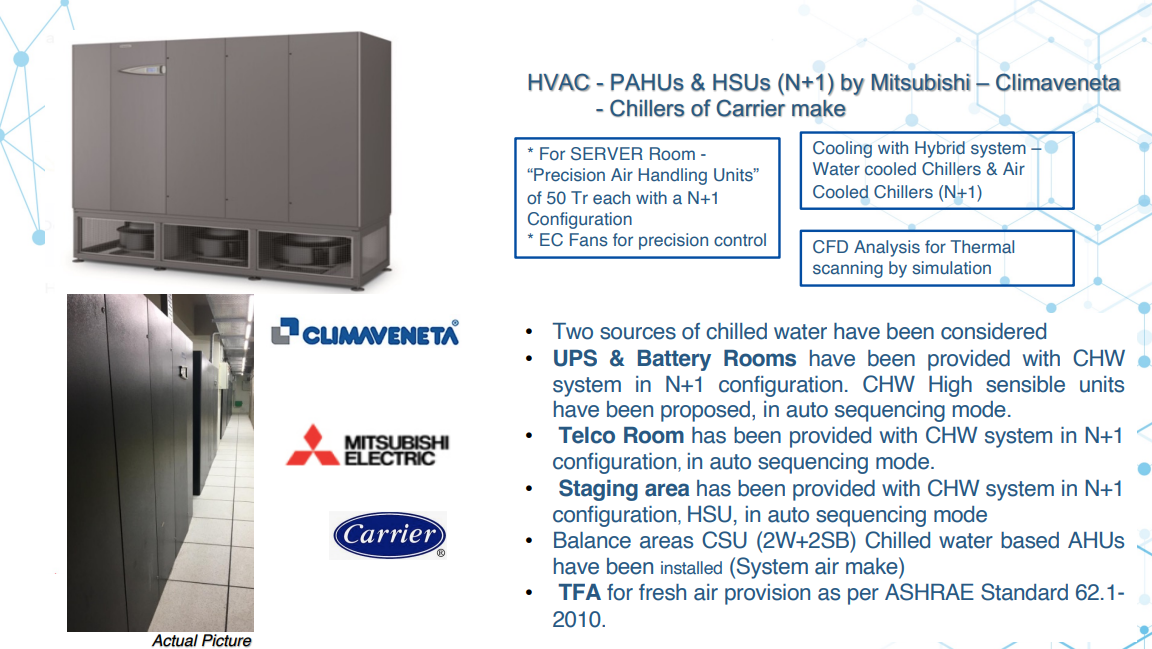

- Multiple sources of HVAC for cooling server halls

- PAHUs must have UPS power backup

- Water distribution system, chillers and thermal tanks

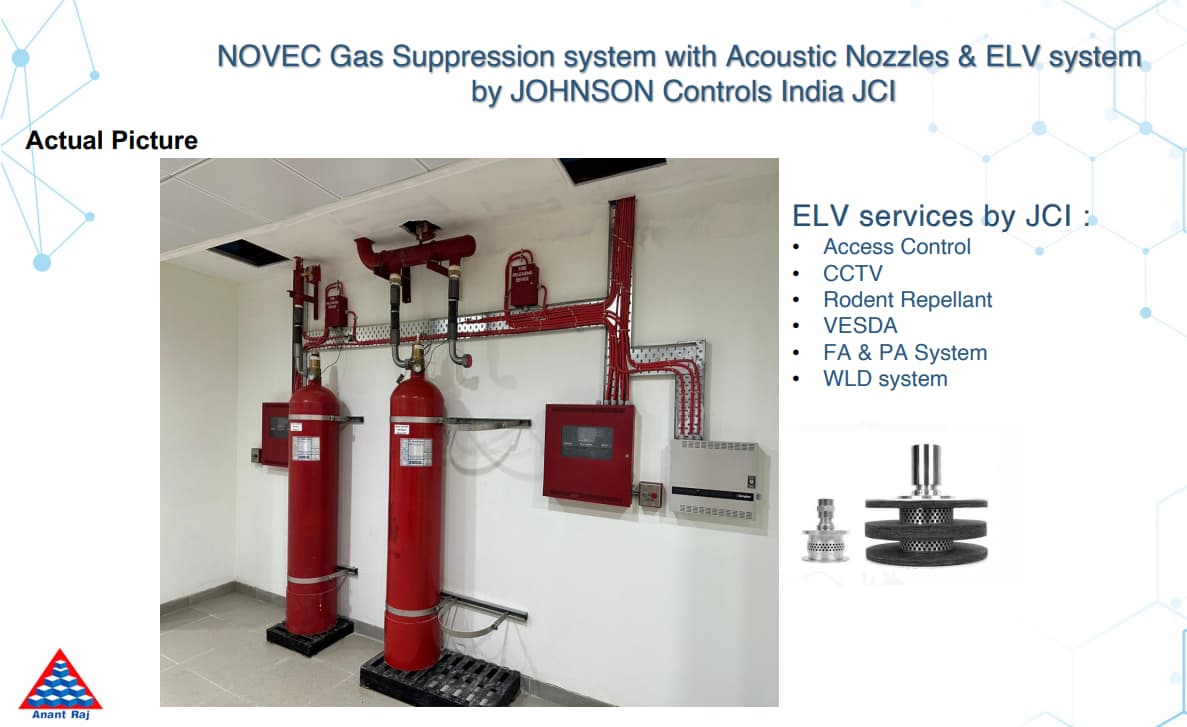

- Gas fire suppression system

- N+N redundancy for power supply and fiber network supply

- Administration building for customers

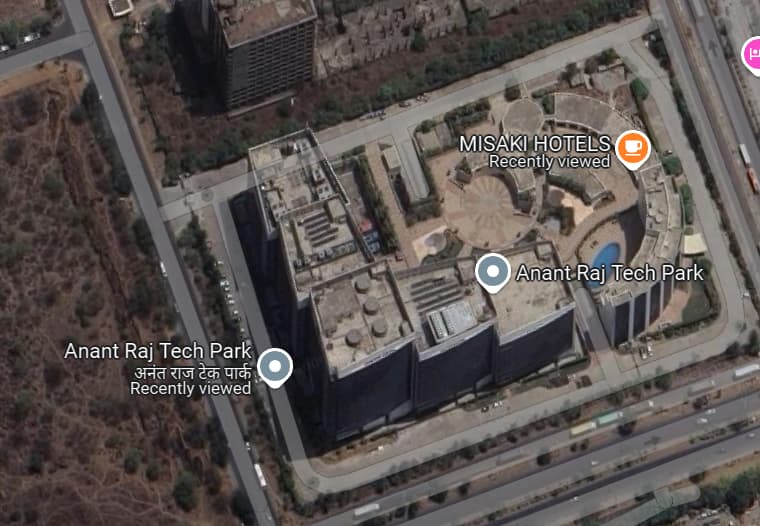

ARL Tech park, Manesar

Located at IMT Manesar industrial estate area, at the center of the manufacturing hub, right next Maruti’s largest manufacturing plant.

1. Security and 2. building monitoring system upto standard as shared by the management

3. Mnangement system room dedicated

4. Diesel generators already built in Tech Park infrastructure

5. Multiple sources of HVAC both air and water cooling systems

6. UPS for power backup

(note – mitsubishi plant is also located in manesar)

7. Water distribution system and thermal tanks no information available

8. Gas Fire suppression system

9. N+N redundancy for power supply and fiber network supply

10. Administration building for customers functioning hotel inside the facility

A few other small details –

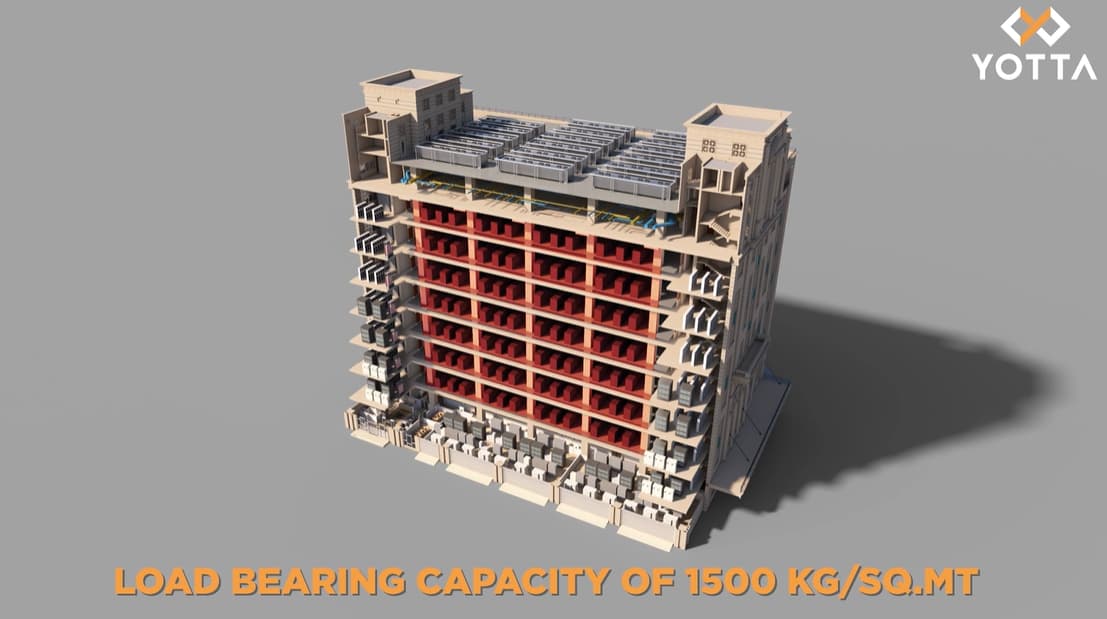

- The infrastructure of the building must be stronger than normal corporate buildings to bear the heavy load of all the equipment.

This process is already completed, and the company needs to just set up the required equipment Q2 FY 2024 concall.

-

Setting up data centers in already established IT buildings with the required equipment.

-

Management expects undercutting in the long run.

- 10-15 year long tenures with clients

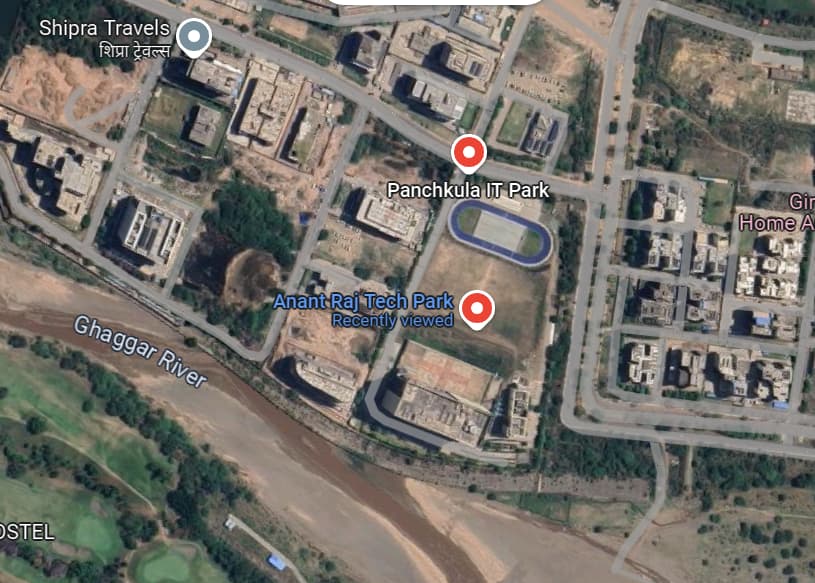

ARL Tech Park, Panchkula –

Existing infrastructure similar to IMT Manesar. No major developments required in this facility as well except for strengthening and equipments.

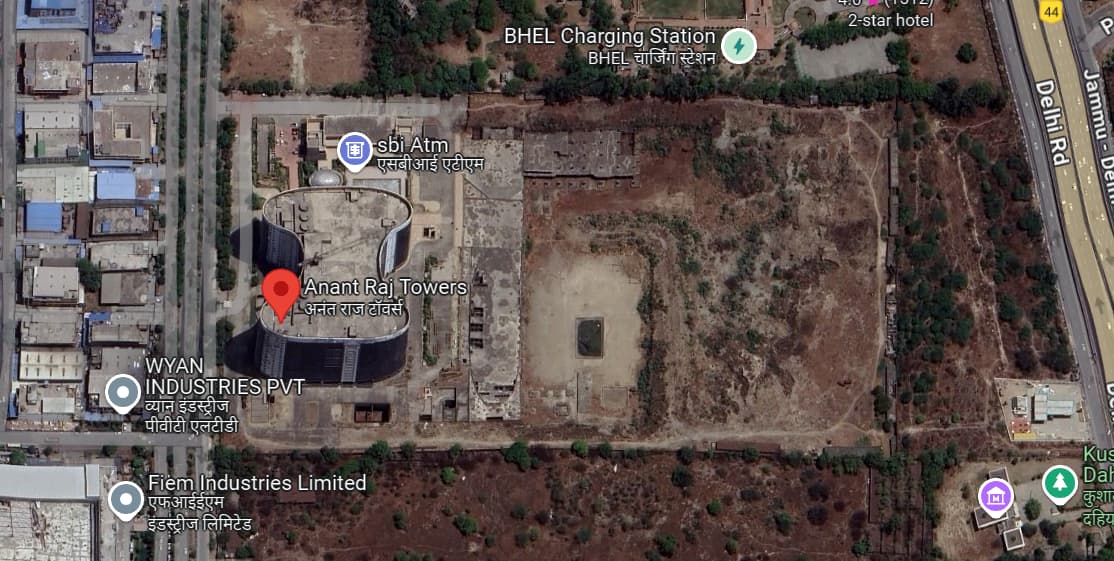

ARL Center, Rai

The largest data center of the company to be. I’m estimating a set up of 50+ (2.2 MW) diesel generators would be required as the yotta facility which was operating @ 100 MW had 32 diesel generators with underground fuel storage for backup power. Along with huge water distribution system and chillers on the roof. This facility seems to be requiring a lot more work than the Manesar and Panchkula facilities simply because of the large 200 MW operational capacity. But they also have a lot of empty land for all the required development.

Source – Presentation by the management.

4cf4ac34-8edb-4a36-991f-d16b6f8811e1_compressed.pdf (1.8 MB)

Disc – invested

Microcap momentum portfolio (03-10-2024)

Please check now. I have updated the sharing.

My Portfolio (Updates and Suggestions) (03-10-2024)

Thanks! Its feels nice discussing.

E2E Networks Ltd – Listed small Cloud computing player (03-10-2024)

A note on micro data centres prepared by people+ai. It covers the categories of Data Centre players in India, the advantages of micro data centre over traditional ones and the players operating in India.

My Portfolio (Updates and Suggestions) (03-10-2024)

As per your plan (regerring to your post above) , if you have a home by age 37 and loan free home by age 40, have a high growth plot of land in a good location and exposure to quality stocks & mutual funds…why do you need a 10% exposure to Gold?

You may need it till time you are exploring what kind of investor you are but once done, you may leave Gold to a maximum of say 1 year expenses in case of extreme exonomic turmoil in country and collapse of other financial channels (hope this never happens. Physical gold will only help then. Paper gold will have no value in such scenario and collapse.

Rest leave to females in family to enjoy as jewellery as per their liking and even some males like it. Enjoy the art for those who like it.

Btw above just personal thoughts and may change with time. Pls take your own decisions based on how your thinking evolves.

Good discussions!

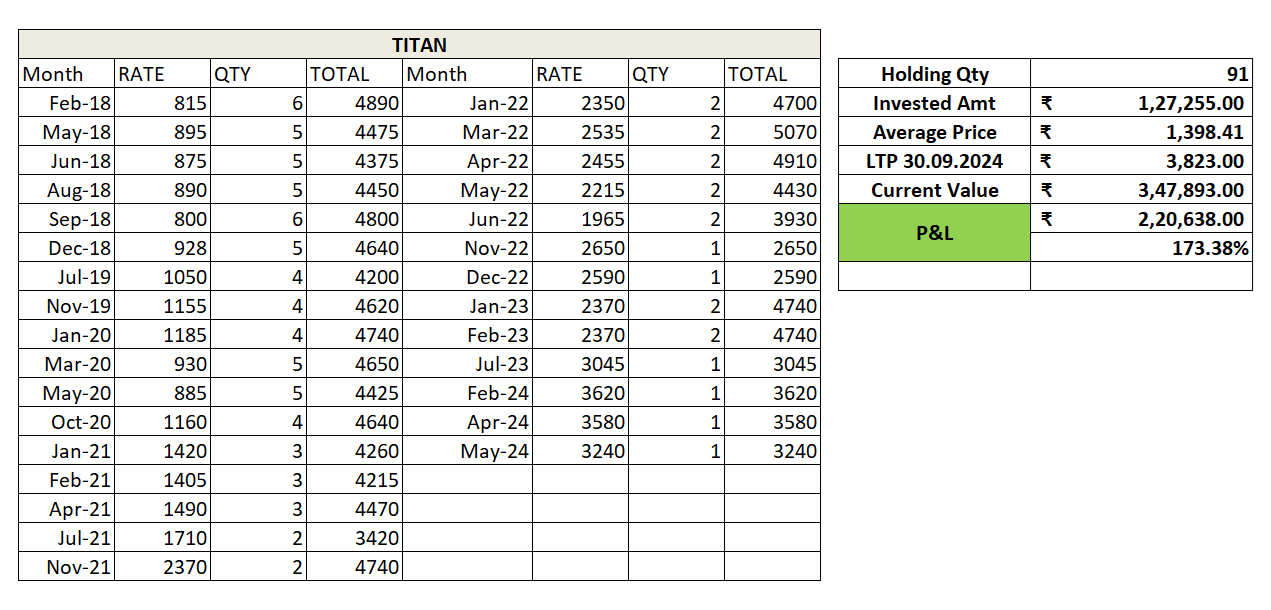

Stock SIP boring yet powerful (03-10-2024)

TITAN back test result

Jan 2018 to Sep.2024

SIP amount : 5000

Disclaimer: invested.

I am not a SEBI registered or a financial advisor. Any of my investment or trades I share on this post are provided for educational purposes only and do not constitute specific financial, trading or investment advice.