It’s Potluri Venkateswara Rao, he is been offloading since 2020, still holds more than 2,00,000 shares, which is 0.15% of the company, he offloaded around 27000 shares

Posts tagged Value Pickr

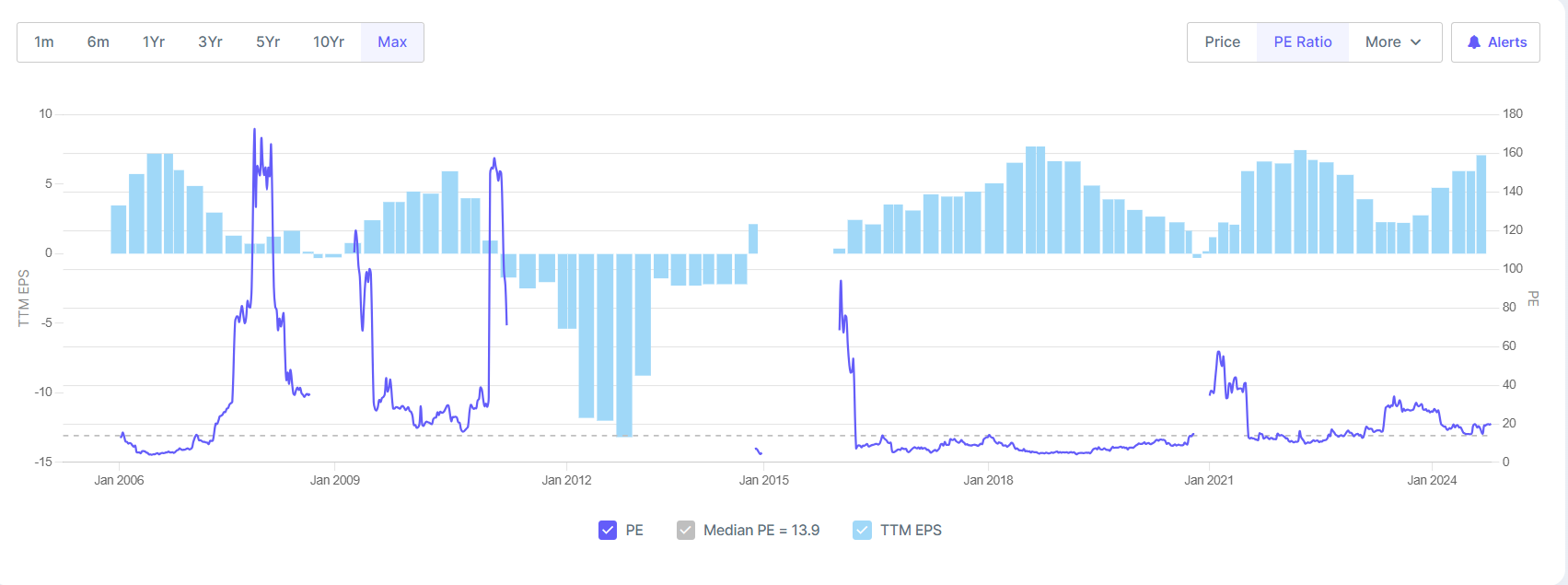

NPST – Technology Provider for UPI Tech (23-09-2024)

On point number 2, looking at past data, the number for Aug doesn’t seem to be the anomaly, but Jun and July are. Seems odd, this should be clarified in the next con call maybe.

On point number 3, the press note says policy upgrades for Evok 2, not version upgrade from 2 to 3 , would cause the blip. Since they’ve explicitly said a blip is expected, we should clarify this as well.

Hope they know what they’re doing and won’t try to disrupt the momentum ![]()

Apeejay Surendra Park Hotels – Potential Value Unlocking (23-09-2024)

Apeejay Surrendra Park Hotels Limited (ASPHL)

Apeejay Surrendra Park Hotels Limited (ASPHL) is a prominent player in India’s hospitality sector, with over five decades of experience in luxury boutique and midscale hotels. Known for its flagship brand, The Park Hotels, ASPHL has established itself as a leader in creating unique, design-driven properties in key urban locations across the country. The company’s portfolio includes 33 operational hotels, spanning luxury, upper midscale, and economy segments. Additionally, ASPHL’s iconic F&B brand, Flurys, contributes significantly to its diverse business model. The company’s commitment to innovation and service excellence ensures its strong position in India’s growing hospitality market.

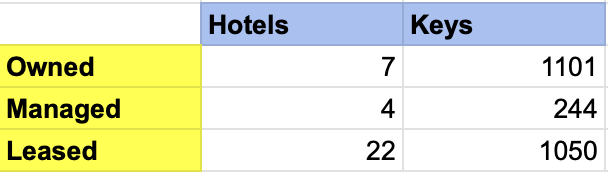

Hotels Bifurcation-

Operates 4 segments of Hotels-

- The Park Hotel– Luxury Hotels in metros

- The Park Collection– Luxury Resorts/Hotels in select tourist destinations (have less rooms)

- Zone & Zone Connect- Upper Midscale segment

- Stop by Zone– Motels (economy)

Hotels in place-

Total Keys- 2395 over 33 Hotels

Key Differentiation-

Operating at- 92% occupancy (100% in kolkata hotel, 93% in Mumbai and Chennai Hotel)

ARR- 6699

RevPAR- 6170

*They have the highest occupancy rates in the industry. Even during the covid maintained 62% occupancy rates.

Guidance-

Occupancy will be maintained at 92%, moreover can increase it to 93-94%.

Revenue Bifurcation-

Room rent- 58%

F&B- 32%

Flurys Coffee Shop- 10%

(ASPHL) boasts a vibrant portfolio of 88 restaurants, nightclubs, and bars, renowned for their exceptional ambiance and energetic nightlife. The nightlife at The Park Hotels has earned a stellar reputation, with its bars and nightclubs being popular destinations among patrons for offering dynamic, immersive environments. Additionally, strong presence in nightclubs and bars compensates for the downturn if ever happens in the industry,

FLURYS- The Coffee Shop / Tea Room

The bakery is quite famous and well known and is one of the most iconic confectionary brand in the country.

It currently operates 82 Flurys bakeries, with plans to expand aggressively by adding 30-40 new outlets annually. The brand has received a strong response from customers, particularly in Mumbai, where its recent introduction has been met with overwhelming success. The outlet near the Gateway of India has consistently exceeded expectations, and a new location in Colaba is set to open soon. Additionally, two kiosks have been launched at Mumbai Airport. Management remains highly confident in Flurys’ growth potential and believes it will continue to surpass expectations.

The bakery is on 3 formats-

- Kiosk- 150 sq ft (capex- 20 Lakh)

- Cafe- 400-600 sq ft (capex- 40-60 Lakh)

- Restaurant- 1000 sq ft (capex- 1cr)

Also, Cafe business is little seasonal-

H1- 40% sales

H2- 60% sales

Flury is earning 13% EBITDA margin. Will increase to the north of 20% in coming quarters and will be maintained there.

Hotel biz EBITDA margin- 36%

Won’t Flurys be a drag on consolidated EBITDA margins?

No, opening of luxury property- The palace hotels will earn significantly higher EBITDA margins and will compensate for the same.

35% EBITDA margin is stable on a consolidated basis. Has 2-3% headroom to grow if operating leverage kicks further.

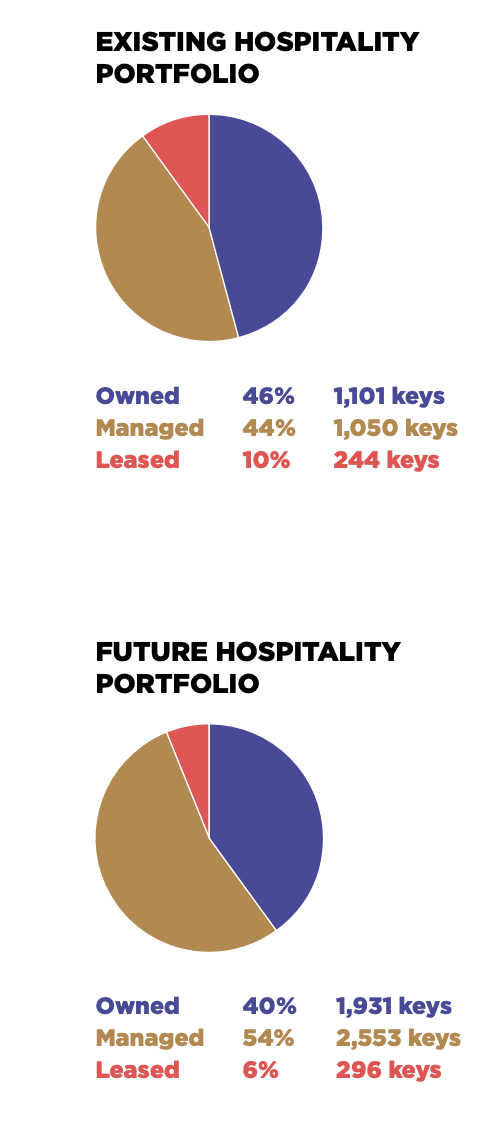

Future Plans-

Many projects are under development for future expansion-

23 Hotels & 2385 keys- planning to be opened. This is almost a 100% increase from the present keys in place.

Q2 FY25-

Opening of 2 flagship Palace Hotels-

- The Chettinad Palace (15 rooms)

- The Ran Baas Palace, Patiala (37 rooms)

ARR for these 2 properties will be 13000. Occupancy will increase substantially. Getting a good response for these 2 hotels. Room bookings are already taking place.

Future Openings-

- FY27: 200 rooms in Pune- at capital outlay of 200 crs

- FY28: 100 rooms in Vizag- at capital outlay of 100 crs

- Fy 29- 200 rooms in EM Bypass + 100 apartments (JV with Ambuja Nautica)

At a capital outlay of 900 crs. The proceeds from the sale of apartments will be used for the construction of the hotels.

- FY 29- 80 rooms in Navi Mumbai

Plus the opening of 30-40 outlets of Flurys coffee house every year.

Total Capital Outlay will be around 1000 crores by FY29, fully funded by internal accruals. Can take a little debt to speed up the construction process. 1000 crores is net after accounting for the sale of apartments,

Future expansions are being driven by an asset-light model. The company’s owned hotels are situated on proprietary land banks, and further owned hotel developments will be constructed on these owned land assets.

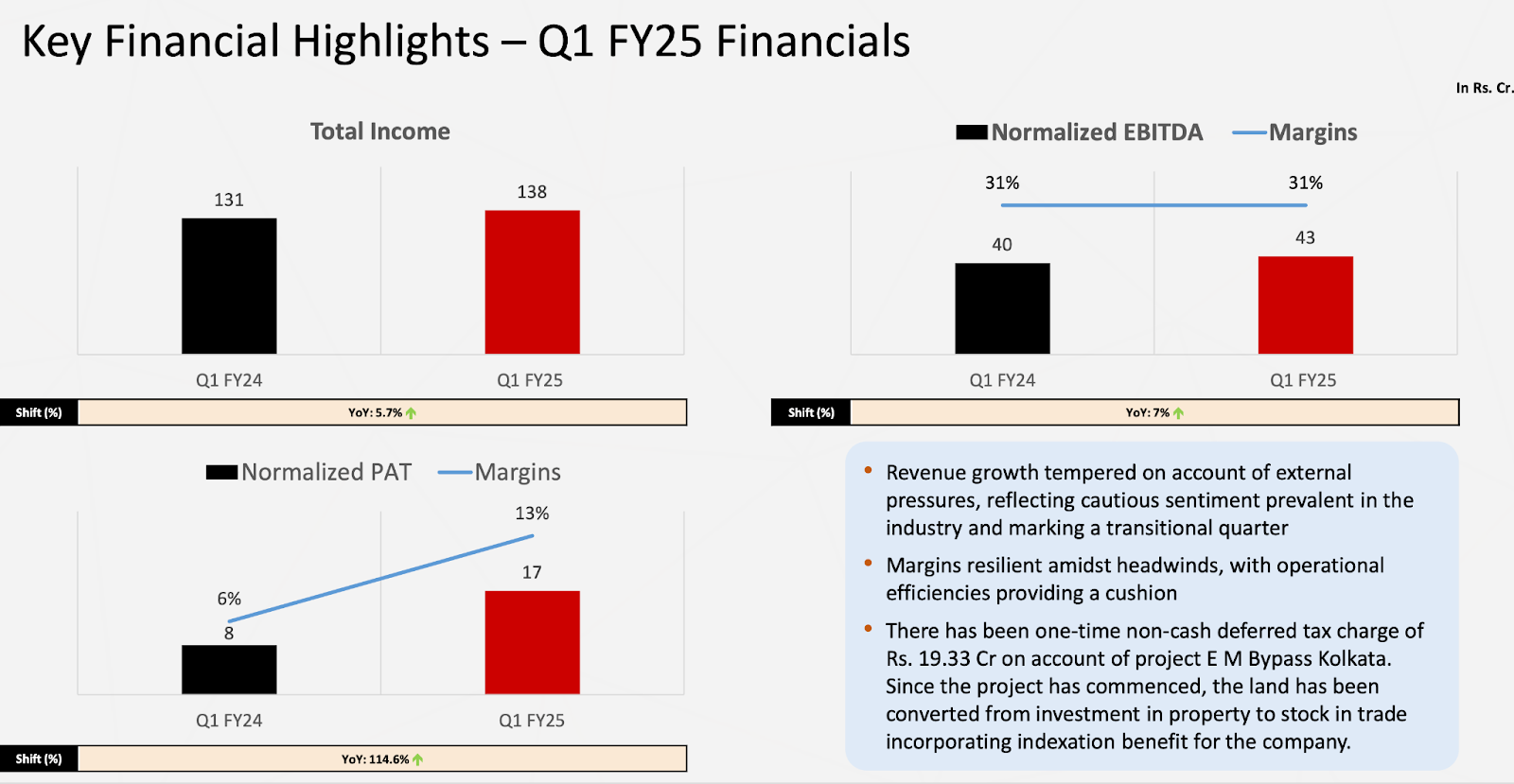

Q1 FY25

Why did PAT increase significantly?

Because from the IPO proceeds, the Company paid off the debt of 550 crores, Huge savings on interest cost happening.

Only 100 crores of debt remains in the balance sheet as of now.

12 Crores of interest payment will be happening p.a. reducing from 66 crores p.a.

Additionally, in this quarter they took 19 crores one off hit. (details mentioned in the slide)

Also, management mentioned Q1 was soft due to elections and heat waves.

And seasonality is there in business: Q4>Q3>Q2>Q1.

The company consistently undertakes renovations to enhance customer experiences, with 10% of its inventory typically under renovation at any given time. Currently, upgrades are underway for several hotel rooms and nightclubs. These ongoing renovations allow the company to maintain and elevate the immersive experience it is known for.

Park Hotels enjoys a high percentage of repeat customers, thanks to the company’s effective use of AI and ML to track user data and maintain ongoing engagement with guests. Additionally, the well-structured loyalty program ensures a strong, loyal customer base, further enhancing customer retention.

The markets they are operating in has seen a robust demand growth of 9.3% outpacing the supply growth of 5%. And this phenomenon will continue further leading to double digit ARR growth.

Flurys saw 17% YoY growth and will continue to surprise further.

Only 100 crores of debt remains in the balance sheet as of now.

12 Crores of interest payment will be happening p.a. reducing from 66 crores p.a.

Management expects 10-15% revenue growth YoY.

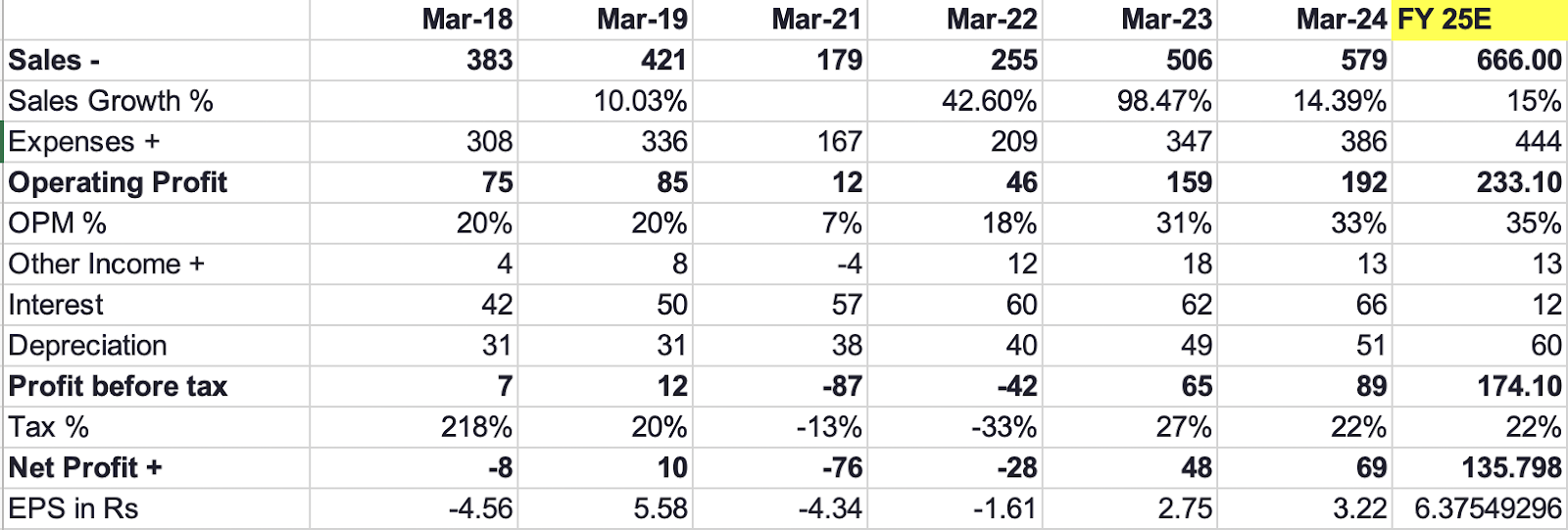

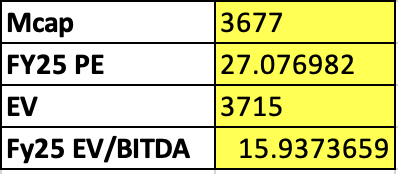

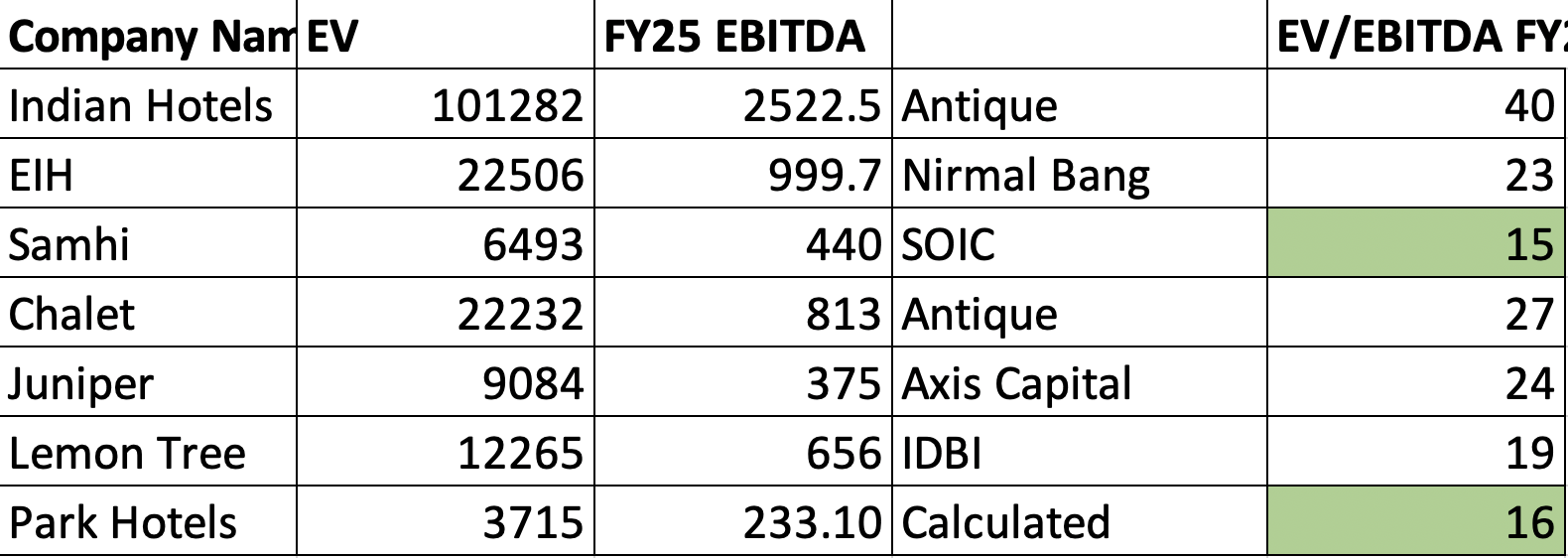

FY25 estimates:

P2P comparison:

Technically in a downtrend.

Srestha Finvest Ltd: A Strategic Shift Towards Green Finance and Sustainable financing (23-09-2024)

Well drafted and I echo the sentiment… Disc : Invested

Naidu’s portfolio (23-09-2024)

I have been studying both arman financials and one of my favorite companies in NBFC’s – Cholamandalam finance. About Chola finance- first of all it is from one of the most reputed conglomerates known for its corporate governance – the Murugappa group. Other group companies have also been in news and market favorites like tube investments recently, but chola has been known for a long time. It has occupied a niche that provides vehicle finance mostly to transport vehicles like trucks, etc and to people who want to run small to medium logistics businesses, small packers and movers etc. Though its forte is in south India but is not restricted to the said location. I was thinking as Highways and infrastructure is being built on such a large scale for almost a decade now and no signs of slowing down, logistics businesses will boom as a result. Now I don’t know which players might succeed, or multiple players may succeed but the company financing many of these players especially small to medium ones, I think it has a runway for growth. But the problem is valuation. Price to book is an expensive 6.5-7.5 range most of the time. The only growth will be the earnings growth and not valuation and no margin of safety otherwise the company itself by my evaluation is an excellent one, the cost of funds is lesser than thier peers like sundaram, aptus etc. Closely looking to invest if valuations come down, unlikely scenario, hope it happens because somehow at such valuations I am not able to convince myself to make it 10% of my portfolio.

IRB INVIT TRUST- new game in the town! (23-09-2024)

PGInvit has disadvantage of being owned by PSU which itself has execution and delivery issues, They have to take clearance from ministries before selling assets to Invit hence lower valuation than Indigrid. PGInvit isn’t comparable with IRB.

Bharat Highways price is appreciating for simple reason of demand and supply, it has just been listed, float is limited moreover their entire portfolio is made up of HAMs which are more attractive in high rate environment. hence demand is higher. we have to see how invit performs in rate cuts.

that being said I think the thing going for Bharat highways is that promoter is aggressive in acquiring assets. If they grow assets base without diluting equity I think it would be worth looking.

IRB INVIT TRUST- new game in the town! (23-09-2024)

how do you estimate INVIT should give 12% or any other certain number? it’s an quasi equity instrument, yield depends on price and many other factors.

For reference only AMT( American tower ) in US which behaves like an invit has dividend yield of 2.5% although price has ran up a lot. Hence don’t take it for granted that invit are obliged to pay a certain percentage.

Wonderla Holidays (23-09-2024)

Why is going to a theme park waste? Also wonderla doesn’t buy land it rents from government…

NPST – Technology Provider for UPI Tech (23-09-2024)

My thoughts

- There is a long term story and then there is a medium term one. In long run, the other products might be more relevant. In the medium term however, we have to take note that, 80% of the current revenue (last Q) came from evok and this contribution grew from around 66% in Q2’24. All said and done market is giving such fantastic trailing multiples as it’s discounting the evok;s growth trend of last few qtrs to continue.

- If there is a question mark raised on the evok business segment’s growth then we have to sit up and take note. The reduction in govt. incentive was the first dent. then this revelation of Cosmos Payee PSP Nos for Aug.

- Can the shift from evok 2.0 to 3,0 have caused this reduction in volume for Cosmos? I doubt it, because NPST is bound by agreement for 99% uptime (Page 194 Rhp) . New version of software are typically not deployed by such disruptions in a industry as critical as dealing with payment systems.

- NPST’s share in the fees earned for providing the evok services to cosmos is 75% of what cosmos earns from merchant. So it’s very much like disrupting your own services not just a service to a customer.

- I am not able to figure if there is a seasonality aspect to the evok nos. or some other aspect that we are missing.

Sky Industries Ltd – Footwear,Automobile manufacturer Major customers (23-09-2024)

All I see are green flags in this company. Although hook and loop seems to be a low barrier entry industry, consolidation can happen and these guys have good certifications and higher margin products. The only issue is in their earnings and seems to be very cyclic in nature. I can see 4 cycles already and it seems the fifth one has started. This is a big concern unless there is a valid reason why this cyclic nature should stop or at least be dampened.