In the SEBI regulations.

Posts tagged Value Pickr

Kilpest India Ltd (18-08-2022)

Good development on the export front.

Disc.: invested

Pix Transmission – low profile smallcap company (18-08-2022)

Good points and definitely something to think about. High compensation might not necessarily be a red flag. But other points mentioned related to audits and audit fees is definitely something that needs to be thought about.

I have limited understanding of how other smallcap companies do it but taking high salary and then lending to the company at high interest rate might not reflect well on the managements image.

Maybe someone needs to ask these questions in AGM etc.

Funny thing about red flags is that they only they get importance in hindsight, when something goes wrong.

Divi’s Laboratories (18-08-2022)

Instead of swindling money or appropriating money by unfair means, its always better to take it in a legitimate way. Running a high performing business, which their parents have started from scratch…they definitely deserve high salaries. I would be in a favour of giving a promoter a salary of 20 crore, instead of him duping the company through unfair means by 100 crores…Why we should make him do that by insisting on lowest salaries…Let them also enjoy the fruits of their parents’ hardwork…

Time technoplast (18-08-2022)

You need to refer to last 5 years presentations as to where the capex had been spent

This company was into multiple product lines and so many geographies , that it had too many mouths to feed …

Refer to this old 2020 presentation you will understand complexity

Now for first time they are prioritising … Hope they might to better job in allocating capital

Pix Transmission – low profile smallcap company (18-08-2022)

Concerns expressed imho are not relevant to how investing works in smallcap in india. As long as co can deliver profitable growth, paying directors more is something market is willing to digest.

Rico Auto Industries Ltd – ROCE to grow + Auto Cycle revival? (18-08-2022)

Some additional points from last concall

-

Contribution from PV (48%) + CV (11%) + Exports (7%) and rest 2W

-

15% of sales in 2W is towards electric - so growth visibility there. New plant for Suzuki also expected to contribute with electric for PV

-

Management mentioned that current capacity can do revenues up to 3000 Cr

Discl : Invested

Rico Auto Industries Ltd – ROCE to grow + Auto Cycle revival? (18-08-2022)

Had posted this today itself in the 52W high thread and post was up for approval - good to see thread started and putting in my points here now.

Rico Auto - close to 52 week high

- Rico is a manufacturer of Aluminium and Ferrous castings for Auto OEMs with clients such as Maruti, Kia, Tata, Honda, Bajaj

- It serves the CV, PV and 2W industry, with ~77% revenues coming from India

- Fundamentals look good in my opinion as there could be scope for sales growth + margin expansion + valuation expansion if the auto cycle plays out

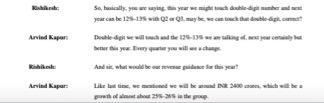

**Sales growth and Margin expansion guidance from latest con-call **

- Management guiding in latest concall for 25-26% sales growth with FY 23 revenue at 2400 Cr (1860 Cr revenue in FY 22)

- Management guiding for margin expansion to 11-12% by FY 24, and at least double digit margins in coming quarters. OPM for FY 22 was 8%

Potential valuation upside in case guidance is met?

Market Cap to sales currently is still at range lows of 0.3x.

This is still below 10 year median (0.4x sales) and far below peak of last auto cycle (1.3x sales)

Disclosure : I am invested and biased

KPI Green- Turning Sunshine Into Cashflows (18-08-2022)

In CPP they charge one time for setting up the plant and then there will only be operating and maintenance charges which they will charge to customers. The CPP segment will only have recurring revenue from O&M.

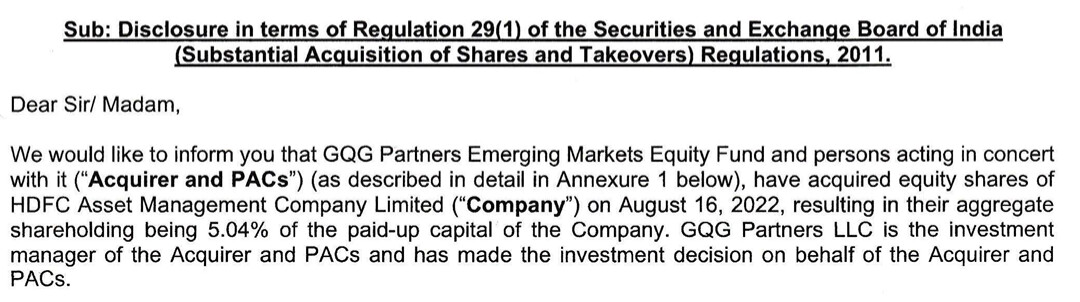

HDFC Asset Management Company (18-08-2022)

A foreign AMC has bought the stake from ABRDN. Doesn’t look like a strategic investor