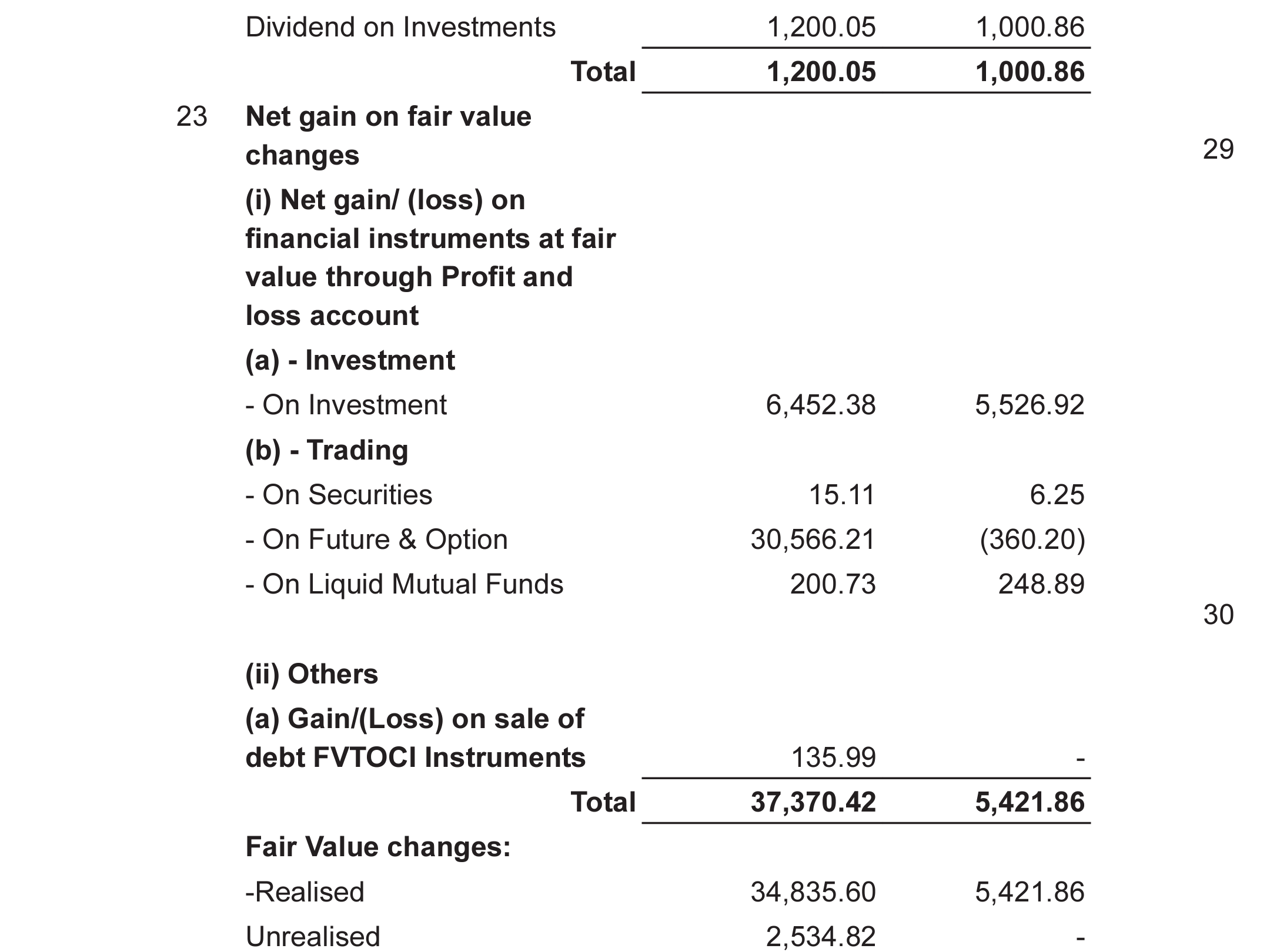

In the Annual report I can see in net gain on fair value change for trading On Future & Option is 30,566.21

So, the company made around 305 crore from f&o?

In the Annual report I can see in net gain on fair value change for trading On Future & Option is 30,566.21

So, the company made around 305 crore from f&o?

Just one confusion. Has the 5 MMTPA terminal already been completed? Sources keep say it will be completed. In that case what explains the outperformance of the energy sector? Thanks

Following my points on this video –

(1) I could not digest the statement on potato as he was in final year of B Sc. Agriculture and he was not knowing where potato grows underground or aboveground!!. I can believe if he is not graduated in Agriculture science – integrity of the promoter !

(2) One man army can work for small level business but not if he want to grow company to mid/large cap. His approach looks like “Jugad” do it at lowest cost. Most of people are from his association. To grow company, professional talent has values and promoters should give respect to talent in respective area

(3) Promoters mentality / thinking is good to grow company from micro to small cap but such approach can not work for further growth of the company

(4) I shall remain cautious and keep track on equity dilution, related party transactions and quality of growth and quality of clients they get for office occupancy!

Tata Motors DVR shares will be swapped for ordinary shares on September 1, 2024, and the shares will be credited to accounts on September 18, 2024.

The cash entitlements will be remitted on September 21, 2024

I would love to hear thoughts & reasoning on the selling between December to next year April/May. How did you arrive to this specific time period?

Thanks

Though the revenues are increasing, the story that the management paints and the reality aren’t matching. Management wanted the exports revenue share to go to 50% and reach 75% eventually. But the reality is, the domestic revenue share is 86% and exports is 14%.

Supporting this claim, the management says that they have presence in 100+ countries and that they have been getting inquires from multiple countries across the world, North America, Australia, Middle East, Nepal, etc. This is to create a narrative that they are diversified now and hence the revenues should be more predictable.

Let’s look at their order inflows in the past few quarters starting from Q2’23 till date: 461 → 2863 → 410 → 1215 → 1529 → 402 → 1141 crores

Of these, the biggest order was from BSNL (domestic telecom), second biggest order seems to be from PGCIL. They secured 9 contracts from PGCIL in the last 12-15 months.

From the recent concalls, the management confirms that the revenues from EPC, railways, North America are pretty less and that the railway revenues may decrease this year. However, they seem to have got a good order from Australia, not sure of the size though.

Putting all these into perspective, Skipper is a domestic player, largely dependent on PGCIL and the telecom tailwinds (revival packages to BSNL from Govt).

For Skipper to grow 20%, they should get order inflows of around ~ 1200 crores, every quarter, or pretty huge orders (once or twice every year) from the existing clientele. Unless there are tailwinds in domestic sectors that Skipper operates in, I am not sure how that is possible. If any, due to the economic conditions, the orders from PGCIL may dry up or slow down (as has happened in 2019).

If it helps, FIIs have reduced their stake from 9% in June 2023 to 3.6% in June 2024, promoters have reduced their stake from 71% to 66% in the last couple of quarters.

Needed a rejig/shake like that to tread cautiously ![]()

Thanks for this bro! Got to learn a lot and still much more to learn… THANKS A LOT ![]()

PB fintech is expected to make 500 crore to 600 crore in FY2025 and 900 crore to 1000 Crore in FY2026, company is expected to have an ROE above of 70% to 80%… Now you can calculate what multiple it should get… I have made a video on it, its pinned in my x account you can watch it.

X- @amitsinghpal

It is always good to listen promoters. However, we need to be cautious and we should know what we are paying for buying a SME / Micro / small / mid cap company on words of the promoters.

It is not good to compare EFC (I) Promoters with Manapasand Beverages Ltd. However, to refresh everyone’s memory on how promoters of this company was selling stories and all well-known analysts / magazines were promoting his vision ! We all know how many retail investors lost their wealth by investing in this company. Following are few links –

(1) Listen (@ 10 minutes) Manpasand Beverages Ltd promoters – https://www.youtube.com/watch?v=BuJXPzvul88

(2) Forbes article – Dhirendra Singh Makes A Fortune Selling Juice To Indian Small Towns And Villages

(3) Motilal Oswal report – https://www.motilaloswal.com/site/rreports/636223141693228805.pdf

In 2017 – Manpasand Beverages Ltd was selling at higher PE than Varun Beverages ! People who loved stories of promoters and entered Manpasand Beverages lost wealth and people who trusted professional promoters, having profession brands, created wealth- irony is Varun beverages was cheaper than Manpasand in 2017!

In bull market, no one has doubt on any dream sold by the promoters and buying without thinking what they are paying !! Such people sometimes earn money but most of times learn it hardaway !