@ Angad and Aditya…..yes u r right….their growth track record has been ordinary…..inspite of ample opportunities like-

-

Being No1 tea brand in India and still not launching an instant coffee brand in India that too after knowing fully well that coffee is a far faster growing seagment.

-

Not taking its Mineral Water brands like Himalyan, Tata Gluco(inspite of having a JV with Pepsi in gluco plus) and Tata Water Plus Pan India.

-

Going slow on acquisitions in India and abroad.

But off late the management has turned far more agressive. As is evident from their actions….Acquisition of MAP coffee(Australian company), Launch of Tata Grand…its Instant coffee offering to take on the Bru-Nescafe Duoopoly in India, Efforts to take Himalyan mineral water pan India, its JV with Starbucks, management commentary on being on the look out for acqiusitions and Cyrus Mistry’s clear intent on transforming Tata brand a lot more consumer facing.

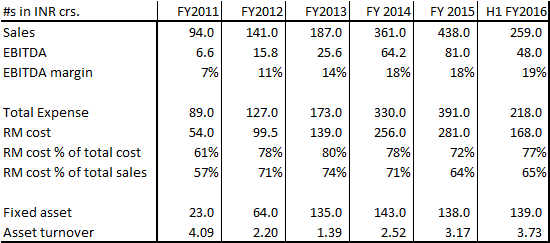

However these thing take time. May be I am too early into buying TGBL. I think I was tempted by yearly price correction and aggressive management commentary. Hoping for a descent uptick in its performance.