Hi Prashant,

Will go through the concall again and get back. May be I missed it earlier.

Hi Prashant,

Will go through the concall again and get back. May be I missed it earlier.

Hi,

Havent looked at Satin Credit and thus dont have any view.

Few more questions :

I think the metrics to track in Take, like in MPS are

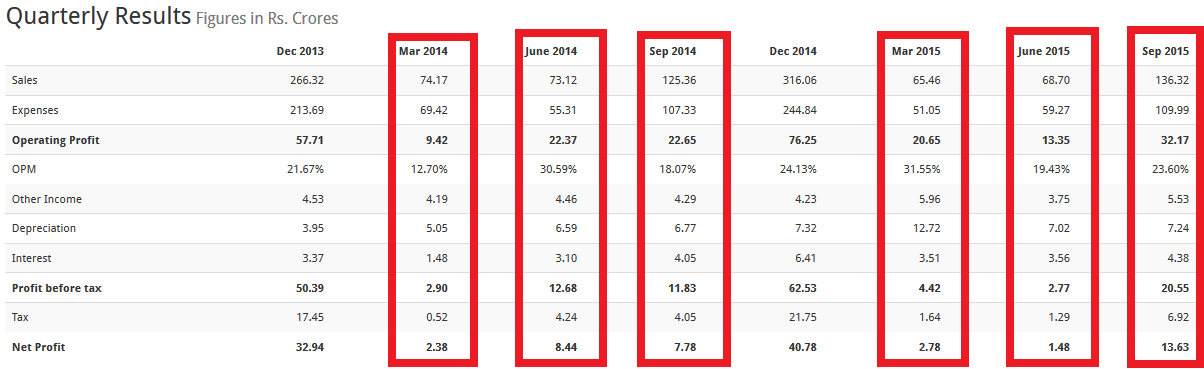

You are correct that 50% of sales are now from the cotton segment. I do not know the margin in this segment as segment-wise analysis is not available in the AR. It is likely that margins are decent. This is evident from the fact that in non-winter quarters the net profit is lower than Q3 but margins are intact(but they seem to vary a lot). Screenshot (there was an adjustment of inventory from June 2015 to Sep 2015):

I would say increase in debt is due to increased store openings. The stores have increased 10% over the last year. Also, the management has indicated in the investor presentation that the company is investing into marketing and advertisement. However, inputs welcome.

I am not very knowledgeable on the institutional arrangements. I know of a few people that buy MC without any institutional tie up. There is a positive spin to an institutional arrangement though – guaranteed sales visibility without marketing and store costs?

Have just started spending some time on this company. Few questions that I am looking out for answers are below:

Ankit, I again I went through the call and they mentioned about venturing into the HFC(in the audio b/w 32.35–33.40) and they have some industry veteran on board who was a head of nationalized bank but nothing materialize yet in this front they said.

Dear friends ! a little information from my side also. Financial parameters are impressive but business outlook may not be so good for comming few quarters. Reason is that some of the products from this company might be in recession. As some chemicals like Bentonite is mainly used in drilling of Oil wells.

Drilling industry prospects look grim so this may dent the profits of this company also. So please do your homework throughly.

Disclaimer: Not invested, tracking

Rajendra Badoni

Hi @ankitgupta Did you get a chance to look at Satin Credit? This looks like an MFI with very good fundamentals and promoter and a bit undiscovered and so low valuations compared to its peer SKS. Can you offer your opinion on this please?

I full appreciate your point. US and UK subsidiary of company account for 72% of Renaissance sales. I have earlier mentioned about companies products being listed on amazon.com. Also both the subsidiary are subjected to local US and UK laws. Financial details about UK Subsidiary is available on privco.com/ (some need to pay for access  )

)

Can you point me to some bankers, who would be ready to talk about the company?

Thanks a lot for clarification Ankit. I thought, i heard HFC