company is becoming a supplier to big international manufacturers. adversity in the form of sluggish domestic markets forced the management to look abroad. now the payoffs will come from both India and abroad.

Posts tagged Value Pickr

Associated alcholols & breweries ltd (29-11-2015)

Now with some states trying liquor ban AABL type of companies will be an added advantage because these type of companies are present in all value chain of liquor industry since they are into bottling supplying grain spirit to major brands thy will be able to sustain better than pure IMIL companies targeting a specific state

But if senior boarders has a view on this please do share it will be helpful

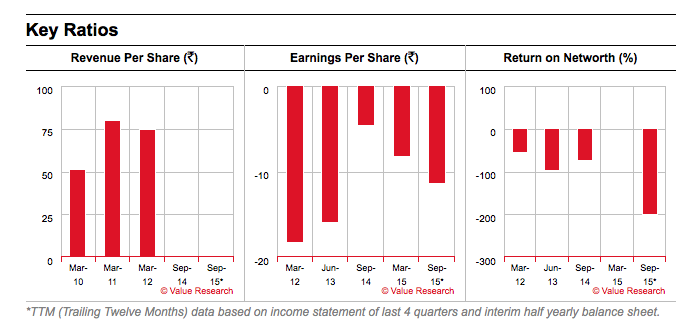

Tree house education and accessories ltd. – Potential candidate for improvement in RoE (29-11-2015)

Gaurav seem to have updated his blog with more details.

Refer to the section under “Significant Update on Saturday Afternoon,November 28,2015”

Top 5 picks for 10 year horizon (29-11-2015)

All I am saying is that given your overwhelming preference for pharma ( and I can see why ) you have not much choice but to allocate to other sectors marginally.

In this scenario beefing up housing finance at the cost of auto makes a lot more sense since structurally that is a segment in a secular uptrend. ( mortgages / GDP is 8 per cent in India compared to numbers almost six to seven times higher in other markets)

But I like your conviction and good luck!

Sarla Performance Fibres – Another Interesting Textile Story in Making? (29-11-2015)

@ ateek and abhishek, thank you for your kind words.

On big order at USA plant – Company has dispatched sample quantity to clients and waiting for their revert (reference concall). My understanding is it takes ~2 quarters for test samples to crystallize into final orders. So they might flow in Q1 FY2017

Yes, it’s a fair assumption that if crude stays at same level then margins will at least stay at same levels! Numbers support this hypothesis and I had asked this question on Q2 concall also specifically.

On shifting of orders to USA plant, not sure if this is happening. However, in that case actually margins will bump up as in USA for commodity products also RM/sales ratio is 30% i.e. gross margin of 70%!

I share the concern on flat sales. But only solace is that management candidly admits (and financial numbers also stand by it) that they are focused on profitable franchise rather than sizeable franchisee.

Is there any rule for max gain weekly, monthly and yearly basis? (24-11-2015)

Fellow Investors,

I feel that BSE is trying to reduce the losses to investors, caused by the selling spree that happens during times of crisis. Even though this safeguard is encouraging the short term (1Yr) trading.

We are seeing the upside a stock can go to 400%, but we all know, just a Random Walk phenomenon can make stock to touch -400%. The Exchange is reducing our Risk and in turn the returns are also reduced.

Say if a stock is 400 INR at year starting, and it climbs to 1600 INR by the year end. Then 1600 INR becomes the base line. So the next 400% jump can take it to 6400 INR in the year 2. It is only that, in Yr 1 the stock cannot reach 6400 INR. How this policy will be abused is yet to be seen.

May be we have to run some simulations and see. Views are welcome.

What makes declining stocks still be part of index? (23-11-2015)

What is the reason large cap declining stocks gets traded in high volume such that they are in index in-spite of performing so poorly?

Foe example stocks like coal india, reliance industries, cairn india have been struggling for years still they are in index. Are the stocks to form index entirely ruled by day trading volume ?

Krebs Biochemicals & Industries – can it be a one of next pharma multibagger? (23-11-2015)

I found it surprising to not to find a thread on this company. It has already been a 10 burger in last two years.So with whatever little information I could gather I am starting a thread.

Krebs Biochemicals & Industries is a 155 Cr company established in 1991, KBIL is headquartered in Hyderabad, India with two manufacturing plants in Nellore and Vizag, India.

Highlights are:

– Undertakes both contract manufacturing for large pharmaceutical and multinational companies as well as product development by KBIL for sale in global markets

– Employs over 600 employees across 3 locations

– Certifications include: USFDA, ISO 9001, Indian GMP Approved, EDQM and EUGMP Approved

– Ipca Laboratories took 18.92% stake in Krebs Biochemicals in Feb 2015

– Primary products in market are pain killers, anti-asthmatic(Ephedrine), anti-HIV drugs and Anti Cholesterols(Simvastatin, Lovastatin)

– Products in pipeline:

– Adenine – Anti Cholesterols

– Atorvastatin – Anti Cholesterols

– Phenylephrine – Anti asthmatic

– Orlistat – Anti obesity

Some open questions which I could not gather much data points.

- Which are the markets KBRL sells?

- What is the split of revenue among its products?

- How is the prospect/demand of anti-asthmatic and anti-HIV drugs in coming years(assuming these are main sources of revenue)

- Who are its competitor in these products ?

- EPS and ROE are negative, so what makes investors to be so bullish on it ?

Disclosure: Not invested yet

Torrent Pharma Ltd (23-11-2015)

Q2 investor update:

http://www.torrentpharma.com/pdf/Torrent-Investor-Update-Q2-2015.pdf

Virat Crane Industries Limited (VCIL) – sure shot multibagger (23-11-2015)

Hi Abhishek, I see Kamadhenu ghee also besides Durga but the shelf space is limited and also the packaging is not as attractive as Durga ghee.

- The packaging is white in color

- Cow ghee is used for pujas at home, temples etc. so I believe it’s not as much consumer product as Durga is

- I do not know what %ge of sales are split between Durga and Kamadhenu but I surmise lion’s share is taken by Durga ghee itself.

- Since this is for pujas, not sure how brand conscious would people be, they would most likely buy ‘any’ cow ghee except for may be someone who wants a particular brand.

- Since Durga ghee is made to use sweets, mix with baby food, people want best ghee (for kids), tasty ghee etc.

These are just observational thoughts on cow ghee and not much research/enquiry has been done.