Posts tagged Value Pickr

Valuepickr Rajkot (02-09-2024)

I am from baroda

native from Saurashtra

have some visits to rajkot & jamnagar.

do notify any meeting in rajkot

Valuepickr Rajkot (02-09-2024)

Kindly message me your mobile number. I will float a whatsapp group. Also don’t post your personal details in this thread.

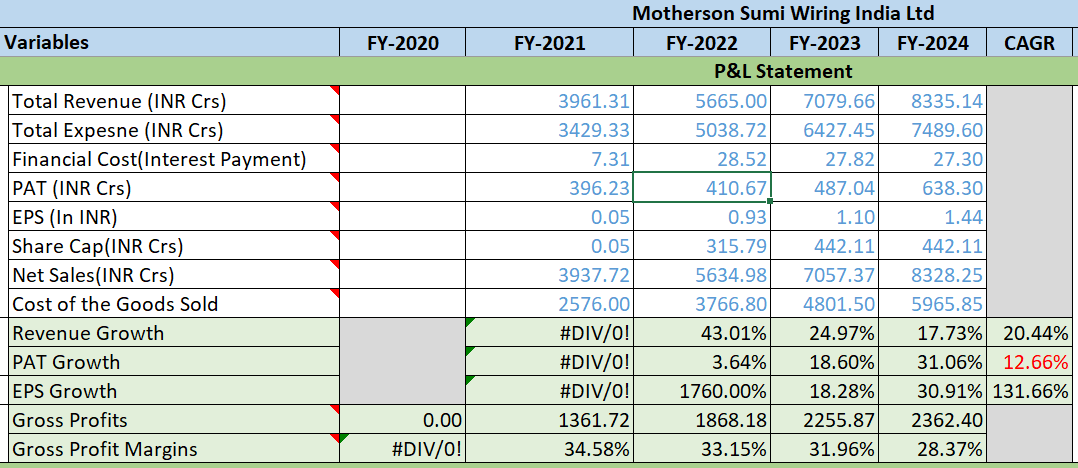

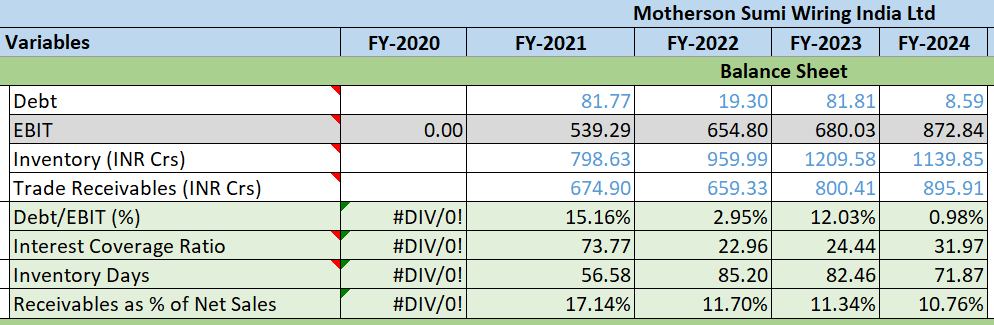

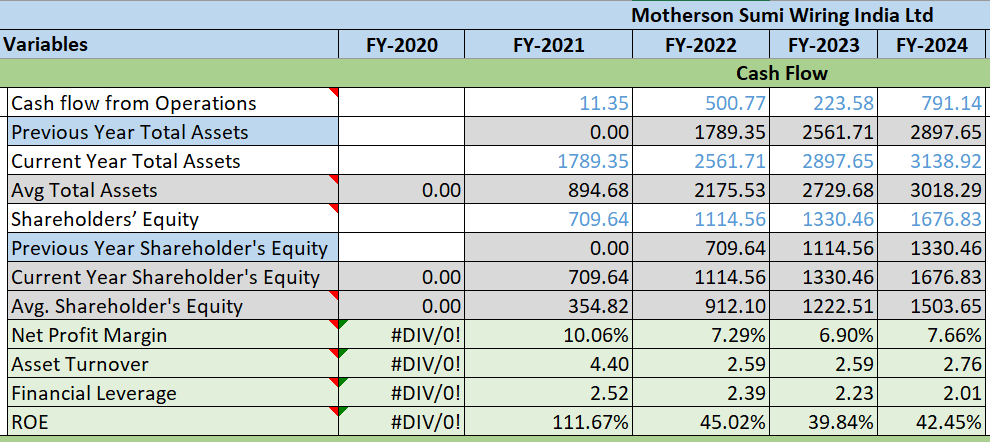

Motherson Sumi Wiring India Ltd (MSWIL) – Wired for growth (02-09-2024)

Hello Community,

I’d like to share some quantitative insights from my analysis, which complement the qualitative highlights that @Chandragupta Sir has thoughtfully provided. His review gives a thorough understanding of the business, and now let’s dive into the numbers since listed:

Profit & Loss Statement:

- Revenue CAGR: 20%

- PAT CAGR: 12%, with consistent year-over-year improvement

- EPS CAGR: 131%, also improving year over year

- Gross Profit Margins: Steadily hitting 30% YoY

Balance Sheet:

- Debt to EBIT Ratio: Reduced over the past 5 years

- Interest Coverage Ratio: Consistently improved over the last 3 years, reflecting sound financial management

- Inventory Days: Declining, while PAT is increasing from last 3 years, signaling positive growth

- Receivables as % of Net Sales: Showing a downward trend, which is encouraging

Cash Flow Statement:

- Net Profit Margin: Consistently around 7%; further improvement would be beneficial

- Asset Turnover Ratio: Stable at about 2.5x

- Financial Leverage: Decreasing

- ROE: Exceeding 40%, which is phenomenal

ROCE & Business Focus:

- The company’s ROCE is driven more by higher sales relative to capital employed rather than margin improvement, suggesting a supplier-side moat. This aligns with the management’s commentary, indicating a strategic focus on ROCE over margins. Maintaining and enhancing this supplier-side moat will be crucial for future performance.

Conclusion:

This is a simple business with a strong supplier-side moat, benefiting from positive industry tailwinds and robust parentage from SAMIL and Sumitomo Wiring Systems, Ltd. (SWS). If they expand their supply reach into other industries like healthcare, aerospace, and logistic solutions, etc., it could lead to margin expansion, improved ROCE, enhanced profitability, and ultimately, higher earnings.

Disclaimer: I am invested, so I may be biased.

Pritika Auto industries Limited (02-09-2024)

They have further expansion plan upto 1 lac MT production by 2027… as per concall they are fully booked and currently delivering 70 % Capacity utilisation of 75k MT production and sales 63% of Capacity utilisation. After demerger the copany is targeting higher margin which can be seen in last quarter results…

Blue Star ~ Leading player in RAC & Commercial Refrigeration (Market Leader) (02-09-2024)

Any internal news in the market? Even with good results, stock is struggling to go up.

IPO Review – Discussion until listing (02-09-2024)

Interview with the Chairman and MD of Namo eWaste Management – Mr. Akshay Jain

Exclusive Interview with the Chairman and MD of Namo eWaste Management – Mr. Akshay Jain | SMEmitra

Hitesh portfolio (02-09-2024)

Thank you so much sir for the reply and complement on name (Actually it was given to me by my Mom)!

Yes , you did mention it as IPOs in a bear market, but I somehow remembered it as IPOs in an ignored sector.

Maybe it’s time to revisit that interview again, I really enjoyed it and appreciate your ability to identify companies at early stage (so many company forums were started by you in VP when they were really small)

if someone wants go through the interview, here is the link : https://www.youtube.com/watch?v=-3BpExbdZ8A

KRBL- The King of Basmati rice (02-09-2024)

I have also exited after being really hopeful for a few years. My worry is that they are sitting on huge inventory but always complain of margins being under pressure due to high cost of purchases. It doesn’t make sense. If prices of paddy go up, they should be making better margins , not lower – as the spreads on earlier inventory should increase. Something is fishy in their inventory numbers and that might be the reason they didn’t hold the concall ( other than the Saudi business not returning for good)

KRBL- The King of Basmati rice (02-09-2024)

I have also exited after being really hopeful for a few years. My worry is that they are sitting on huge inventory but always complain of margins being under pressure due to high cost of purchases. It doesn’t make sense. If prices of paddy go up, they should be making better margins , not lower – as the spreads on earlier inventory should increase. Something is fishy in their inventory numbers and that might be the reason they didn’t hold the concall ( other than the Saudi business not returning for good)