Equitymaster has a graph that does this for the last three years at least.

My two cents – those graphs don’t mean much to find whether it is worth investing. Discounting all future cash flows to today and comparing with price – that’s the real value identifier.

Posts tagged Value Pickr

Historical P/E ratios (20-11-2015)

Duke Offshore – Hidden Gem? (20-11-2015)

I am not sure about monsoon story. Monsoon was week this year. So, why this affected more this year. As soon as qtr ended, they got the job in Oct!

How, do you feel about 6 cr reserve? Is that enough for new vessal! How much debt it need to take if not?

Thanks.

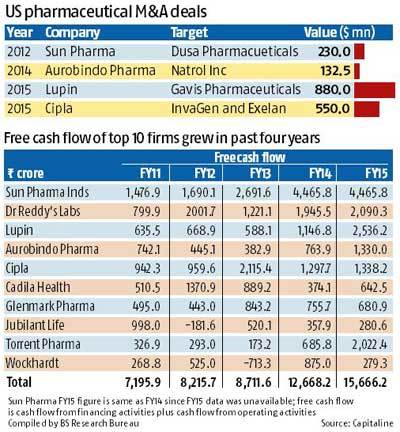

Torrent Pharma Ltd (20-11-2015)

Thanks Hitesh bhai.

I think the key trigger market is waiting for is some US based acquisition from Torrent. Given that they did not repatriate any cash from bumper US sales, and maintaining standalone debt indicates that management is keen on acquisitions.

Also, any inorganic growth would fill up the void from one off abilify sales in FY16. After Cipla and Lupin, Torrent might be next in line.

Historical P/E ratios (20-11-2015)

I am also interested to know this

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (20-11-2015)

According to Assocham study sugar prices in india is likely to firm up from summer of 2016.

Assocham press release about sugar study. Also as per recent concall of EID Parry, bounce in sugar prices from recent low of around 11 cent / lb to 15 cent / lb is technical in nature as most global projections estimates deficit of around 2-3 million tonne for consumption of around 182 million tonne for year 2016. However projection for 2017 is more supportive of global sugar prices. Also US FAO project that sugar prices can touch 18-19 cent / lb based on fundamental factor by 2017 which can be fair value of sugar considering expected demand supply scenarios. However from 2018 again some surplus is possible. All bounce back in commodity prices start with bit skepticism but gain ground based on future events playing out. However with severe deficit of monsoon in 2015 usually shock in sugar cane supply mostly surprises in downside and expectation of sugar prices touching 40-45 range sometimes in next 2 years in indian market cannot be rules out as agricultural product prices in india moves up very sharply in short duration. Also logically it does not make sense that in a country where hardly any vegetables or food staples available below Rs 40 only sugar is available below Rs 30 which is more difficult to produce and consumes more time , money and efforts in producing 1 kg of sugar than any other crop based food items.

Forensics and the art of triangulation (20-11-2015)

Have been on and off on value pickr. Find attached a report by ambit – which I think is quite good on forensic accounting.

I will also share a report by ACFE in the next post as the file size is too big to be posted in one post.

Avanti Feeds (20-11-2015)

Will these series of cyclones on the east coast impact production ? @hitesh2710 – if you could ask your contact on it pls and about general trends in shrimp pricing and volumes.

Thomas Cook India-Will it move like Warren Buffet Stock (20-11-2015)

Dont agree – things are always fluid – I am sure things that were thought of when the deal between TC and quess was signed have changed now. The issue is not changing terms but if they can they are favourable to minority shareholders. Remember that’s its the species that adapts itself to circumstances that survives in the long run.

At this point of time, given prem watsa’s record and ajit isaac’s record, I am willing to give tthem the benefit of doubt

MPS Ltd (20-11-2015)

thanks @Donald – will share my notes. I have spoken to a few guys in the industry and the gist of it was

a. mps mgmt is very good and they know what they are doing

b. they are focussed on margins and would never sacrifice it for growth

c.their sales team doees not have as much mojo as others – partly because they were never used to selling as a macmillan subsidiary – they were a cost centre and had captive business

d. SPI global and Newgen are ahead in terms of growth and profitability. Spi has scale while newgen has a lot of niche IP

I do not know SPS and TNQ. will share financials of newgen and others by this weekend. Also, will check if any of my contacts is willing to talk specifics on these.

Thanks

Gulshan Polyols(GPL) – Business by FMCG and Valuation by Commodity (20-11-2015)

CK Jain latest interview in CNBC

Key Points:

- Key projects (grain processing, desi liquor )completion by Q1 2016. Starch processing, Sorbitol capacity expansion to completed by 2017 March and company plans to deploy 150 crore for the same.

- Grain processing plant in UP started contribution to sales from Q2.

- Ability to pass on raw material price hike to customers in next quarter (HUL,Dabur,Coalgate etc.)

- Sorbitol domestic consumption estimated growth is 10% where as less margins for exports.

plans to increase the sorbitol capacity expansion 20% by 2017. - Paper plants has to adopt onsite ppc plant for reducing the cost and ease of maintenance, either today or 2 years down in the line. GPL is the only company to do so in India.

- Aim to reach 800+ crore sales by 2018 March, considering immense market potential in PCC, Sorbitol, Liquor and other business.