Thomas cook tie up with OYO rooms http://m.economictimes.com/magazines/travel/thomas-cook-india-inks-pact-with-budget-aggregator-oyo-rooms-to-offer-budget-stays/articleshow/49800797.cms

Posts tagged Value Pickr

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (17-11-2015)

Hi,

Couple of pointers…

1) Company isn’t using cash flows from kerry (through lactose sale) for setting up Lactulose capacity. Numbers from Capex has just started flowing through and should keep improving sharply over couple of years.

2) Lactulose Capacity has been largely put up through debt (Long Term debt increased from Rs 4.7cr in FY13 to Rs 29cr in FY15.

I had attended the AGM (was among 3-4 shareholders who attended  )..What I could gather from Atul Maheshwari (MD)…Lactulose market is very exciting given application of the same and company has put up capacity after insistence from the clients. You are right sales from Lactulose will be around Rs 60cr. Demand it seems is largely tied up. I have no idea about whether Lactulose will be sold domestically or exported.

)..What I could gather from Atul Maheshwari (MD)…Lactulose market is very exciting given application of the same and company has put up capacity after insistence from the clients. You are right sales from Lactulose will be around Rs 60cr. Demand it seems is largely tied up. I have no idea about whether Lactulose will be sold domestically or exported.

Since company has expanded massively given its size, it would like to stabilize current capex initially. Management had indicated that Kerry has asked them to put up more lactose capacity. To get more idea about Lactulose beyond what capacity has already been put up, one should try meeting the management. What I could gather from secondary sources is Lactulose is niche market.

Hope this helps.

Thanks.

Disc – Invested.

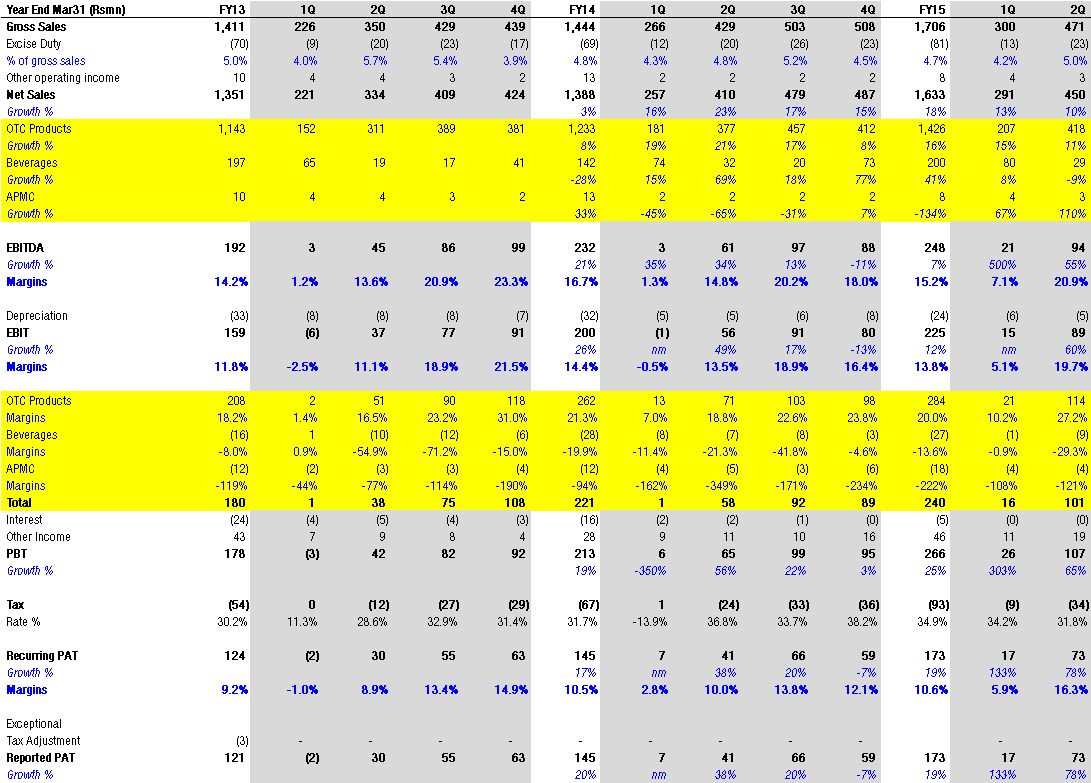

Amrutanjan Healthcare – Finally Waking Up After 100 years? (17-11-2015)

Amrutanjan produces and sells ayurvedic OTC healthcare products. The company’s 100% subsidiary AHCL makes the chemicals for the products. The CMD of the company is Mr. Sambhu Prasad who took over 9 year back. The company is more than 100 yrs old and was set up in 1893. Earlier the company used sell only the yellow pain balm. Everyone in South India knows this company and must have used the pain balm. A few years back the company undertook a re-branding exercise and launched a white pain balm. It also acquired Siva Soft Drink which owns the Fruitnik brand.

From the FY14 Annual Report

We wish to grow the next 3-5 years at a CAGR of 33%. This is bold. But looking at the past, one can argue we are trending in the right direction. 2000-2005: 0% 2005-2009: 5% 2010-2013: 10%

Focus on Head , Body and Congestion areas for our core business and offer/build portfolios in each vertical. We wish to also expand on our smaller portfolio of other products like Sanitary napkins and foot care products(corn caps) that can grow by entering the distribution chain and reaching consumers. Once they individually reach a level of sales that is self sustaining brand investments can happen. We have other unique OTC products that will be entering the market space this year.

The challenges for a company our size is to match the investments in media attempted by our much larger competitors. We have to recognize that our nearest competitor is 10 times our size and two of the smaller brands have sold out to larger competitors in the last 5 years. This was a very dormant category till 2009! Inspite of these head winds we executed to sustain in this business. This industry is driven by investments in the brand and this is a fact. Share of Voice and Share of Market are correlated strongly. We wish to steadily increase our share of voice to a level that will help us build new brands, and sustain existing ones.

Key Investment Arguments

Even if company can sustain 15-20% sales growth (and not 33% like they are targetting) margins will expand meaningfully because of operating leverage which could lead to much faster PAT growth. You can already see the growth pick up in FY15 and 1HFY16 already.

684crs market cap company. Zero debt company and has net cash of Rs38crs. Pays 30-40% of profits out as dividends.

Has plant in Mylapore, Chennai which has been shifted to the outskirts of Chennai. The land available of 2.5 acres is worth upwards of Rs150crs. Dont know when it will be monetized though. In FY09 company sold land for Rs84crs and paid a special dividend and also did a buyback.

Key risks as I see it

Small company with a topline of just Rs171crs. Advertising is critical for sales growth. Dont know if it can spend and compete with the likes of Zandu. Chinese balms like Tiger is another area competition. Subsidiary which makes the chemicals for the balms is loss making. Consolidated profits are Rs2crs lower than standalone profits.

Big investors in the stock already

—-Vijay Kedia of Atul Auto fame

—-Sundaram Mutual Fund.

Company website

https://www.amrutanjan.com/index.html

Disclaimer:

—-Have only done research based on publically available data and not met management.

—- Am invested in the company so my views might be biased.

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (17-11-2015)

This one looks interesting. This is a case of the company expanding the lactose facilities, earning the conversion charges from Kerry and utilising the cash flows to get into the lactulose market.

Given the arrangement with Kerry, the lactose segment would be an asset light model with periodic fixed asset charges for expansion.

The lactulose market looks interesting. From the import figures the rough guesstimate is that India is importing 2200-2400 tonnes per annum of lactulose. This seems to be primarily from Fresinus Kabi plants in Austria and Italy and Danipharm from Denmark. There also seem to be some shipments from the UK.

The question is what is the market size of lactulose in India and if the market can absorb the increased capacity. If the usage doesn’t go up, then it is a case of import substitution. Does anyone have pointers to the global market size and key players? Is it possible for Lactose India to export lactulose given the cost advantage if any.

At around $3.75 landed cost for lactulose, the peak revenue for the company would be around 60 crs before they need to expand again.

I think we need to dig deeper into the lactulose market dynamics before a decision can be taken.

The trading behaviour of this scrip looks very strange with no sellers but a single buy order at UC for a few lakh shares. The usual traded volume was a few thousand shares not very long ago. Better watch out

Disc- Not invested

Lloyd Electric & Engineering Ltd (LEEL) (17-11-2015)

Their main markets are in the South and also Gujarat. Hence mostly they have Southern film stars for promotions. They started off with Tier2 towns as promotion expenses are lesser but now they are gaining traction with their brand and tightening terms with dealers and trying in Tier 1. They even refused Vijay sales as it’s terms were unacceptable. Their margins in ACs are among best in industry as they are backward integrated as they produce own coils. They have a 12% market share in aircon now and are doing better than industry growth. The TV and washing machine business is still in infancy and they just assemble and sell for now to test the waters. If I am not wrong they were once sole supplier to Daikin but I dont think it is so now – some players may have changed suppliers since Lloyd is now also a competitor. They also supply to Bombardier etc. So Quality of product is not an issue – but building a brand is an expensive affair, which is captured in the valuations. Air conditioners are hugely under penetrated in India ( what isn’t) and is still an aspirational product so the runway is very long. The margins in TVs have declined of late and is expected to remain the same because it has become highly competitive with online sellers burning money. I do think their ad campaigns are interesting though and are not targeted at the middle class buyer anymore. Also their website for online sales. What they are trying to push is that they will provide exceptional customer service and make it their differentiator – every customer complaint is provided with a no that the customer needs to give to the technician if he is happy. Else the matter gets escalated and the customer gets a call from the central helplines to resolve the issue. LG, samsung, voltas etc do not have this concept. In Voltas anyway customer is left to fend for themselves. The focus now will be on invertor ACs as next year Aircon star ratings are again going to be revised making them more expensive.

Zenith Fibre (17-11-2015)

Stock has been hitting upper circuits since the publishing of results on Nov 7 which were positive. Not able to buy the shares. Has given more than 25% returns in a week.

Discl:Not Invested at this time

Deepak Fertilizers and Petrochemicals (17-11-2015)

As a topic starter, you are suppose to disclose your holding in the stock. Please do so immediately.

Deepak Fertilizers and Petrochemicals (17-11-2015)

As a topic starter, you are suppose to disclose your holding in the stock. Please do so immediately.

NCL Industries – Resumption of growth? (17-11-2015)

Checking the price online shows this data. One need to track this only biweekly basis to see the trend. Since this is the first time this site is checked lets take the current rate as base rate

http://www.materialtree.com/building-materials/cement/53-grade-cement?dir=asc&mode=grid&order=price

Wockhardt – A story with twist and turn (17-11-2015)

Anyone tracking has idea when is the concall?