The latest version now computes Piotroski score for last 9 FY.

Automated Stock Analysis with the Piotroski Score

Posts tagged Value Pickr

Automated Stock Analyzer (05-11-2015)

MPS Ltd (05-11-2015)

Thanks for the detailed explanation. Definitely it helps me to understand MPS deeper. You and your team is doing a great job.

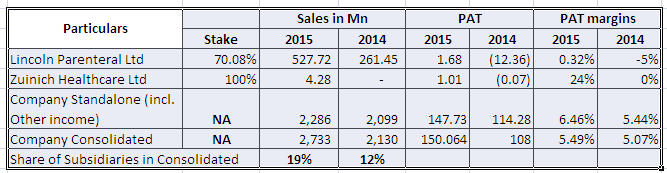

Lincoln Pharma … the next mid-cap pharma in the making …? (05-11-2015)

Company has two subsidiaries – Lincoln Parenteral Limited and Zuinich Healthcare Ltd. .

After analyzing the Financial Statements, I noted the following:-

Almost, 20% of sales has contributed nothing to the PAT margin. So, the subsidiary business is margin dilutive in nature.

Also, its hard to believe that a company generates 16 lacs of PAT on 68 crores of sales (it includes 16 crores to holding). I feel if that’s a way of taking out cash from the business.

Lincoln pharma has given 4 crores as a deposit to Lincoln Parental Limited.

I observed 5 directors out of 7 from the promoter group.

None of them has a degree or mentioned experience in pharma field.

I’ve certain doubts on governance  .

.

Thanks.

Disc : Not invested. Under Radar.

MPS Ltd (05-11-2015)

I think I could not explain properly.

The Moolah lies in servicing the needs of the Academic/Educational STM (Science Technology Medical) Journal & Books Publishers.

I would think catering to Digital Publishing requirements of these customers is profitable – as The Digitally transformed product is only (one of) the Outputs. The main technology service that MPS like providers provides is what is called pre-publishing processes & workflows. From the Time an author submits a manuscript or file to the publisher to proof-read to editing to cross-referencing author reference for scholarly articles referred, to integrating bibliography to design to content rendering/transformation or print. The technology service provider game is to provide quick turnaround from author file to reader consumed final product – to be available for the Publisher’s platform.

Catering to digital publishing requirements of non-STM segment like say an Amazon.com self publishing platform cannot be that profitable or for that matter say fiction or business or fashion books/magazines and the like.

Hope this time I could explain better

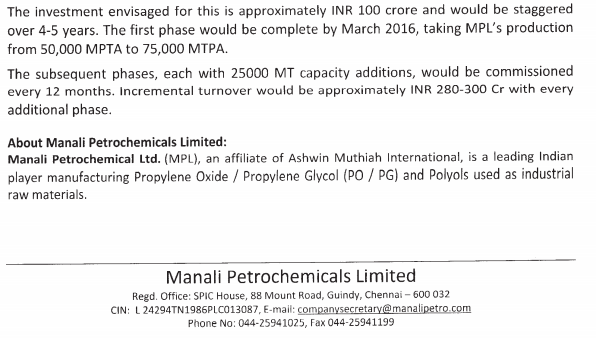

Manali Petro- Capacity Expansion (05-11-2015)

Only thing I will be concerned about it is – “This huge stockpile of cash is utilized properly and for the interest of all shareholder”

Any pointer towards promoter’s background?

Manali Petro- Capacity Expansion (05-11-2015)

I have a query on their announcement dt Aug’15 “Pending receipt of approval of TNPCB for consent to operate at higher capacity, utilization of the plants has been restricted.”

If their current capacity is under question for Pollution board how come a big capacity planned by the company will not face such risk in future?

Second in their May press release they had plan to invest Rs 100cr for capacity expansion

But in Sep they signed MOU of Rs 500cr investment which includes power plant as well

Discl – Exited fully in 2 phases…want to buy again post some clarity on capex

MPS Ltd (05-11-2015)

Got it. thanks a lot for quick reply. I am reading the real moolah lies elsewhere as … Multi B $ opportunity in print publishing outsourcing.

Nitin Spinner – textile yarn story (05-11-2015)

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/2641D161_381D_41EF_8125_8A00AF9F3C09_134315.pdf

results just came out

Not as stellar as last qtr but still decent

MPS Ltd (05-11-2015)

Manoj,

You are right about that – we did not focus on digital publishing. Because that is not a segment that matters. Refer to the Segment info on BQ Sheet1.

Where is the FOCUS then – only one thing – if the business has done well in the past, why will it be sustainable in the future; Just why can’t somebody dislodge it from its perch in its own niche – that’s the one answer we want to find out – either way. Focus on where 80% of the business comes from.

Digital Publishing is an important segment no doubt in the overall publishing industry, and set to grow faster bigger in the years to come – the way content consumption needs are changing – multiple devices, multiple formats.

However competency – one would reckon is open to anyone and everyone, lots of players, not a protected market for them unlike the Academic/Educational Books & Journals segment; though they will continue to offer these services – more to complete service portfolio where existing customers – Academic/Educational customer need digital publishing/content transformation solutions, or newer customers like Apple say; volumes will be small, margin profile should be poorer. They might have some Marquee customers in this segment too, one can reckon. But the real moolah lies elsewhere