That I understood, but how they will fulfil 15% allotment requirement to small investors?

Posts tagged Value Pickr

Companies With First ever concalls OR Investor Presentations (01-09-2024)

Suratwwala Business Group, first presentation:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d7bfbd91-ee7a-456c-abfb-612b94ce23a5.pdf

Ola Electric – Full Stack EV play? (01-09-2024)

I find very hard to predict stock price even 6 months down the line so it’s impressive to such confident forecast of 540 (an interestingly precise reference) for 10 years down the line.

I have seen too much faith being put in DCF but methodology has been mostly rejected by highly seasoned investors including Mr Buffett.

Considering that investing in equity market is far from exact science and one has no clue about the future, all one can do is to find a fairy good company run by capable management and hope for the best. That’s how Mr Jhunjhunwala found Titan when no amount of DCF would have justified his bold call on the company.

Hero Motor – Leader in two wheeler (01-09-2024)

I won’t be very sure about that. Bhavesh Agarwal is up against the best, of the 2-wheeler industry, who have bootstrapped themselves to become among the best in the world. They have the kind of management quality, deeper cashflows, and R&D firepower which Ola doesn’t have yet, relying purely on debt and a very benevolent capital market to fund their expansion. God forbid if there happens to be a price war in 2-wheeler EV space, I won’t count on Ola to survive that.

Whether Ola has got a secret sauce in the product, the answer is NO. So far based on the channel checks and having heard feedback from different sources there is really not much to choose between different EV bikes of Ola, Hero, TVS etc. So it’s not as if Ola is making a superior product.

Below is a recent interview from Rajiv Bajaj with his trademark candor and insightful commentary. At some point he makes a note that Ola is losing its market share which to me is not surprising.

Overall I don’t think Ola has any advantage over the ICE 2-wheeler incumbents and they will have to try really hard to succeed in this space.

Bajaj Auto To Soon Hit The 1,00,000 EV Sales Milestone | Rajiv Bajaj Exclusive | CNBC TV18

MOLD TEK PACKAGING—dividend plus growth (01-09-2024)

Basically pkging industry itself is a pure play commodity business, now many other sector co’s are adding machines to make these stuffs but not QR coded one, in commodity space it’s very hard to push specialized product, like paint where every co is joining the band wagon like Astral, JSW etc & more will follow where costing to end user matters, so adopting a pkging which will increase cost is a matter of question, also co claiming to be mkt is accepting specialized product that too is a matter of speculation at this moment, costing minimization is the agenda of customers that may hurt Moldtk’s speculation,

It’s absolutely personal view, may differ with others

Advanced Enzyme Technologies Ltd – The Enzyme company (01-09-2024)

Advanced Enzymes –

Q1 FY 25 concall and results highlights –

Revenues – 155 vs 147 cr, up 5 pc

EBITDA – 51 vs 44 cr, up 16 pc ( margins @ 33 vs 30 pc )

PAT – 35 vs 29 cr, up 19 pc

Segment wise sales breakup –

Human nutrition – 101 vs 99 cr, up 2 pc ( 65 pc of sales )

Animal nutrition – 17 vs 16 cr, up 7 pc ( 11 pc of sales )

Industrial bio processing – 25 vs 22 cr, up 12 pc ( 16 pc of sales )

Specialised manufacturing – 11 vs 10 cr, up 10 pc ( 7 pc of sales )

Geographical breakup of sales –

India – 74 vs 74 cr, flat

Americas – 59 vs 47 cr, up 27 pc

Europe – 7.5 vs 6.5 cr, up 13 pc

Asia – 11 vs 12 cr, down 7 pc

RoW – 3 vs 8 cr, down 60 pc YoY

Manufacturing facilities –

08 in India, 01 in US

05 R&D units in India, 01 each in US and Germany

Company is a leading manufacturer of Probiotics and Enzymes. Company makes over 400 products derived to of 68 indigenous enzymes. These are substitutes of chemicals and find applications in diversified industries like – healthcare, agrochemicals, animal and human food etc

Enzymes – are proteinaceous molecules which serve as bio-catalysts. They not only replace traditional chemical agents but also bolster efficiency and efficacy of a wide array of products. Find wide applications in – baking, food processing, dairy processing, leather processing, biofuels, biomass processing, biocatalysis etc

Probiotics – are living microorganisms that confer significant health benefits to both humans and animals. They also find application in treating disease in areas like – inflammatory bowel disease, urogenital infections etc

Company stared its manufacturing operations in 1994 with just 07 enzymes. Today, it makes 68 different enzymes

Biggest entry barrier to this industry is real time R&D with requirements of continuous technical upgrades and efficiency improvements – both are long gestation traits

Company is expecting robust growth trajectory for all its products in H2 this yr

Company’s largest product – an anti-inflammatory enzyme ( serrapeptidase ) recorded a sales of 28 cr vs 35 cr YoY, a de-growth of 20 pc

R&D spends @ 7.6 vs 6.2 cr YoY

Company was working on some sugar management and weight loss products. The same has been launched in the US on a trial basis

Guiding for 33-34 pc kind of EBITDA margins for full FY 25. Also expecting a 12-14 pc kind of topline growth for full FY 25. Most of the growth should be back ended – ie – in H2

Capex requirement for current and next FY should be light @ 25-30 cr each

Company does have a lot of products ( around 50 of them ) under development ( at various stages ). As these products get their requisite approvals, go commercial – they should drive company’s growth

Company has also started their B2C business under the WELLFA brand – so make and sell wellness products. Currently in nascent stages – likely to clock 2-3 cr of annual sales

As a medium term vision – company aspires to keep growing at 10-12 pc kind of rates for next 4-5 yrs and breach the 1000 cr topline number

LY, company had a one off legal expense of 18 cr for settlement with a US based competitor. Don’t see any such exceptional expense this FY

Company’s current capacity utilisation @ around 60- 65 pc

According to the management, as the capacity utilisation improves, every 1 pc increment in revenue should lead to a 2 pc kind of growth in EBITDA and bottomline

Disc : holding, biased, not SEBI registered, not a buy/sell recommendation

Ranvir’s Portfolio (01-09-2024)

Advanced Enzymes –

Q1 FY 25 concall and results highlights –

Revenues – 155 vs 147 cr, up 5 pc

EBITDA – 51 vs 44 cr, up 16 pc ( margins @ 33 vs 30 pc )

PAT – 35 vs 29 cr, up 19 pc

Segment wise sales breakup –

Human nutrition – 101 vs 99 cr, up 2 pc ( 65 pc of sales )

Animal nutrition – 17 vs 16 cr, up 7 pc ( 11 pc of sales )

Industrial bio processing – 25 vs 22 cr, up 12 pc ( 16 pc of sales )

Specialised manufacturing – 11 vs 10 cr, up 10 pc ( 7 pc of sales )

Geographical breakup of sales –

India – 74 vs 74 cr, flat

Americas – 59 vs 47 cr, up 27 pc

Europe – 7.5 vs 6.5 cr, up 13 pc

Asia – 11 vs 12 cr, down 7 pc

RoW – 3 vs 8 cr, down 60 pc YoY

Manufacturing facilities –

08 in India, 01 in US

05 R&D units in India, 01 each in US and Germany

Company is a leading manufacturer of Probiotics and Enzymes. Company makes over 400 products derived to of 68 indigenous enzymes. These are substitutes of chemicals and find applications in diversified industries like – healthcare, agrochemicals, animal and human food etc

Enzymes – are proteinaceous molecules which serve as bio-catalysts. They not only replace traditional chemical agents but also bolster efficiency and efficacy of a wide array of products. Find wide applications in – baking, food processing, dairy processing, leather processing, biofuels, biomass processing, biocatalysis etc

Probiotics – are living microorganisms that confer significant health benefits to both humans and animals. They also find application in treating disease in areas like – inflammatory bowel disease, urogenital infections etc

Company stared its manufacturing operations in 1994 with just 07 enzymes. Today, it makes 68 different enzymes

Biggest entry barrier to this industry is real time R&D with requirements of continuous technical upgrades and efficiency improvements – both are long gestation traits

Company is expecting robust growth trajectory for all its products in H2 this yr

Company’s largest product – an anti-inflammatory enzyme ( serrapeptidase ) recorded a sales of 28 cr vs 35 cr YoY, a de-growth of 20 pc

R&D spends @ 7.6 vs 6.2 cr YoY

Company was working on some sugar management and weight loss products. The same has been launched in the US on a trial basis

Guiding for 33-34 pc kind of EBITDA margins for full FY 25. Also expecting a 12-14 pc kind of topline growth for full FY 25. Most of the growth should be back ended – ie – in H2

Capex requirement for current and next FY should be light @ 25-30 cr each

Company does have a lot of products ( around 50 of them ) under development ( at various stages ). As these products get their requisite approvals, go commercial – they should drive company’s growth

Company has also started their B2C business under the WELLFA brand – so make and sell wellness products. Currently in nascent stages – likely to clock 2-3 cr of annual sales

As a medium term vision – company aspires to keep growing at 10-12 pc kind of rates for next 4-5 yrs and breach the 1000 cr topline number

LY, company had a one off legal expense of 18 cr for settlement with a US based competitor. Don’t see any such exceptional expense this FY

Company’s current capacity utilisation @ around 60- 65 pc

According to the management, as the capacity utilisation improves, every 1 pc increment in revenue should lead to a 2 pc kind of growth in EBITDA and bottomline

Disc : holding, biased, not SEBI registered, not a buy/sell recommendation

Smallcap momentum portfolio (01-09-2024)

As per my knowledge

1 year : 2023-09-01

6 months : 2024-03-01

GODFRYPHLP , ERIS , DOMS , WHIRLPOOL , QUESS → IN into List

HSCL , JAIBALAJI , MOTILALOFS, BLUESTARCO, BLUESTARCO → Out from the List

Hero Motor – Leader in two wheeler (01-09-2024)

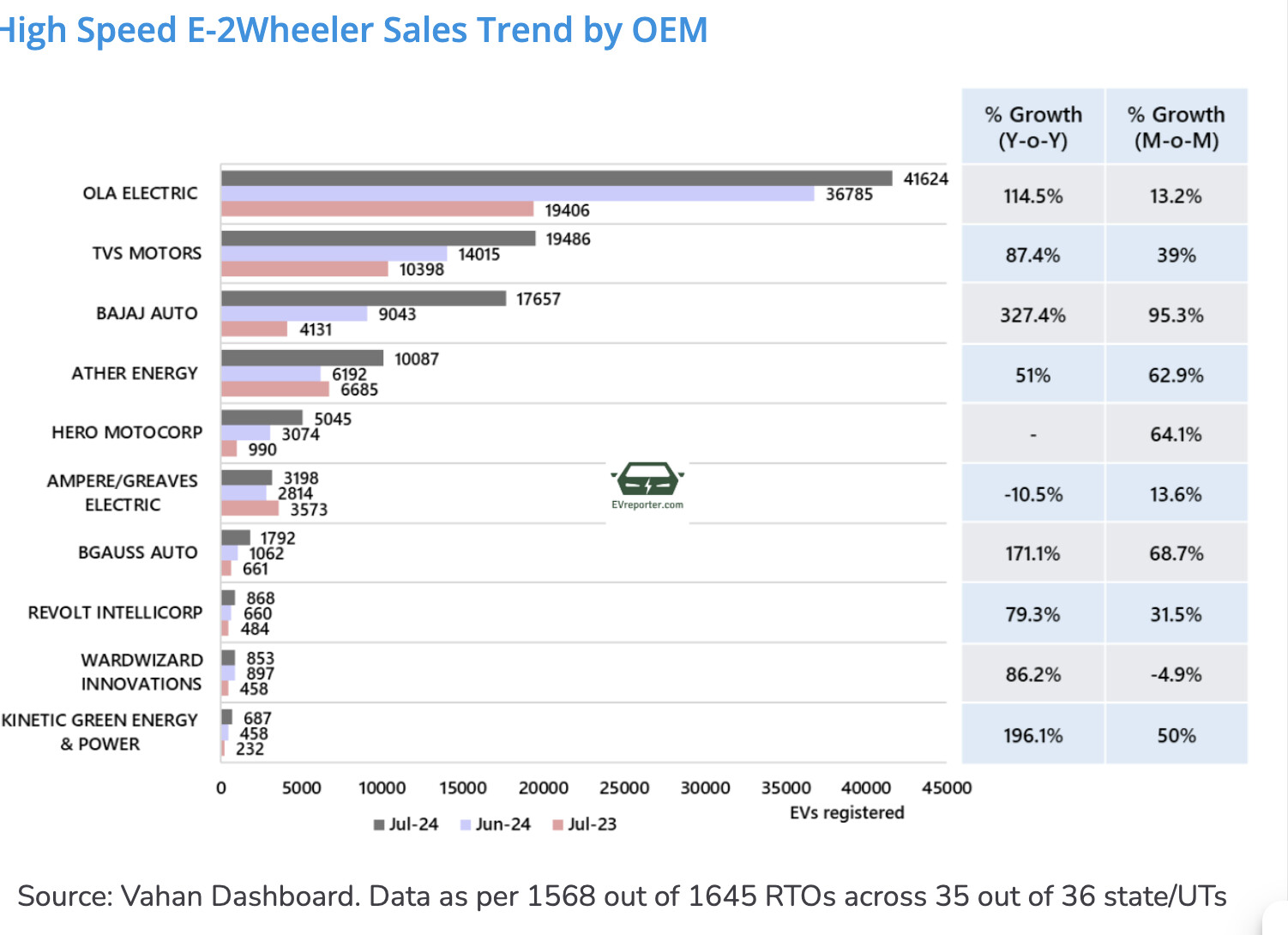

Based on the latest data for July 24 TVS Motors and Bajaj Auto are doing good growth.

Burger King ~ Whopper of an Opportunity (01-09-2024)

That’s due to IND AS 116, where lease liabilities are now considered a part of debt.

Remove that and debt to equity is around 1.