Hi @nav_1996 Pediasure was launched way back in the year 2000. Are there any new products that they’re launching, which I am not aware of?

Disclosure: Recent tracking position

Hi @nav_1996 Pediasure was launched way back in the year 2000. Are there any new products that they’re launching, which I am not aware of?

Disclosure: Recent tracking position

Rajat Monga, Senior Group President, Financial Markets & CFO addressed the call:Highlights by Capital Mkt

Bank has continued to post strong loan growth of 29% at end September 2015. Bank expects loan growth to be at 25% for FY2016.Bank has exhibited strong CASA growth momentum driven by surge in saving account deposits, while current account deposits growth was steady as bank has shed some unprofitable current accounts.

The healthy new account addition has mainly boosted the saving account deposits growth. Bank has stepped up saving account additions to 1]1.2 lakh customers every quarter compared to 80-90 thousand addition in the corresponding quarter last year. Bank has added 1.25 lakh accounts in Q2FY2016.

Average savings account cost stood at 6.9%. Bank has take further pricing adjustment measures. Bank has reduced the peak interest rate on saving account deposits to 6% from 7% earlier, which is expected to further reduce the cost of saving account deposits.

Bank has improved NIMs to 3.3%, while bank expects further improvement in NIMs with higher rising CASA and retail assets acquisition.

Bank has already been calculating its base rate on marginal cost of funding based methodology, so donft expect any impact of banking system shifting to marginal cost of funds base rate calculation.

Bank has board approval for capital raising of US$ 1 billion and plans to raise capital next year.

Fresh slippages of advances stood at Rs 130 crore in Q2FY2016. Meanwhile, bank has not sold any asset to asset reconstruction companies in Q2FY2016. Bank has also not undertaken any refinancing under the 5:25 scheme.

Key highlights of Conf Call by Capital Mkt

The net sales increased by 33% to Rs 97.05 crore while net profit inclined by 98% to Rs 4.74 crore. Top-line growth was fully volume drive.

Investment in innovative marketing helped sales to grow. However, innovative gift impacted the gross margin.Employee cost was high due to recruitment at top level and in south market.

Marketing expenses for Q2 was lower on innovative consumer promotion.

Crax and Natkhat both recorded healthy growth.Natkhat has shown good growth in Rs 5 pack.The company has seen healthy growth across all zones.The company is increasing production capacity at existing Noida location at cpaex of Rs 25 crore which will be done through 75% external debt and 25% internal accrual. Rs 100 crore additional revneu is expected from this capex.

The mgmt said that it is working on new products.The company’ term loan is Rs 35- 36 crore at present. After capex, term loan will go up Rs 52 crore. The cost of loan will be 11%.The company’s direct reach is at 2 lakh outlets,Q1 is lean quarter as schools are closed. Q2 is strong quarter. At end of Q3, sales drop due to winter. Q3 and Q4 are good.The last time price hike taken by the company was in April 2014.2-2.5% ad spends to sales in Q2

Sunil Pahilajani MD & CEO & Narayan Narasia CFO addr callHighlights by Capital Mkt

In September 2015 quarter, sales fell 4%to Rs 424.73 crore. Engines Division sales fell 4% to Rs 408.20 crore.While the revenue growth is still a concern on account of weak market conditions, various operational excellence initiatives have started yielding results and has been reflected in the EBITDA margins improvement.OPM jumped 510 basis points from 12.7% to 17.9% taking OP up 35% to Rs 75.97 crore.PBT grew 55% to Rs 75.42 crore. EO loss stood at Rs 1.85 crore against Rs 14.80 crore. PBT after EO soared 117% to Rs 73.57 crore. After providing for tax (up 195% to Rs 19.31 crore), PAT jumped 99% to Rs 54.26 crore.

For the six months ended September 2015, sales fell 7%to Rs 805.39 crore. For the six months, Engines Division sales fell 5% to Rs 778.34 crore.OPM jumped 520 basis points from 11.9% to 17.1% taking OP up 34% to Rs 138.11 crore.PBT grew 51% to Rs 133.71 crore. EO gains stood at Rs 5.54 crore against a loss of Rs 15.43 crore. Thus PBT after EO soared 90% to Rs 139.25 crore. After providing for tax (up 140% to Rs 41.65 crore), PAT jumped 74% to Rs 97.60 crore.

The company has show caused its modern 105 HP three cylinder, BS IV complaint, ‘ leap Engine’ for automotive applications at recent Society of Automotive Engineers – China Congress & Exhibition at Shanghai, China which offers attractive value proposition to its OEMs. This thrust on farm Equipment sector continues with launch of indigenized Mini Power Tiller and Paddy Weeder. The company can provide more such engines of different variants.These farmer friendly products are value for money and suitable for local soil condition.

The launch of Greaves Mini Power Tiller and Greaves Paddy Weeder is a testimony to its continuous efforts in innovation and product development.Its Farm Equipment Business is focused on transforming the lives of small & marginal farmers by enabling them to mechanize various farming practices backed with strong service network & easily availability of Spare Parts in rural markets at affordable prices. These machines are certified by Government of India as per the latest standards andare backed by Greaves cotton’s nationwide authorized dealer networks.The company has focused on few things. These include focus on genset business, farm equipment business, cost minimization and working capital improvement.Value engineering and other cost initiatives has helped the company in getting better margins. Benefit of lower commodity prices also has helped in improving the OPM.Going forward, commodity benefit will have to be passed on.Volumes for 3 wheeler was 80000 in September 2015 quarter (against 90000 y-o-y) and 4 wheeler was 10000 (10000) respectively.Pump business volume was 22000 in September 2015 quarter (against 25000 y-o-y) tiller was 1000 (against 2000).

Second half should be better than fist half in auto business.The company’s market share in 4 wheeler segment is around 85%. The company is in Small Commercial Vehicle (SCV) segment which is sub 1 ton vehicle. The company can offer solutions for 3.5 tons also.Auto business accounts for 55% of its sales.After Markets sales accounts of 18-19 of sales.In tax the company enjoys benefits for R&D spends so it is 26-27%.The company has Rs 100 crore capex.Utilisation is 75% in Auto Engines.Around 55% of sales come from Auto OEMs, 18-19% comes from After Market and rest comes from agri power generation.3 wheeler and 4 wheelers segments will get better for the OEM’s. This is what the company is hearing from the OEMs.Exports is 4% of sales and the company is hoping it to enhance it to 10% of sales in next 3 years.Price negotiations with the OEMs happen around twice a year.Volume wise second half is expected to be better than the first half.

Results out. Completely flat results, marginally higher revenue eaten up by higher finance cost. 9687FF94_B396_40B5_A983_17AD0720B7E1_172916.pdf (42.1 KB)

Most of the good product lines like Pediasure is getting launched thru unlisted subsidiaries.

Did you apply in HNI category ?

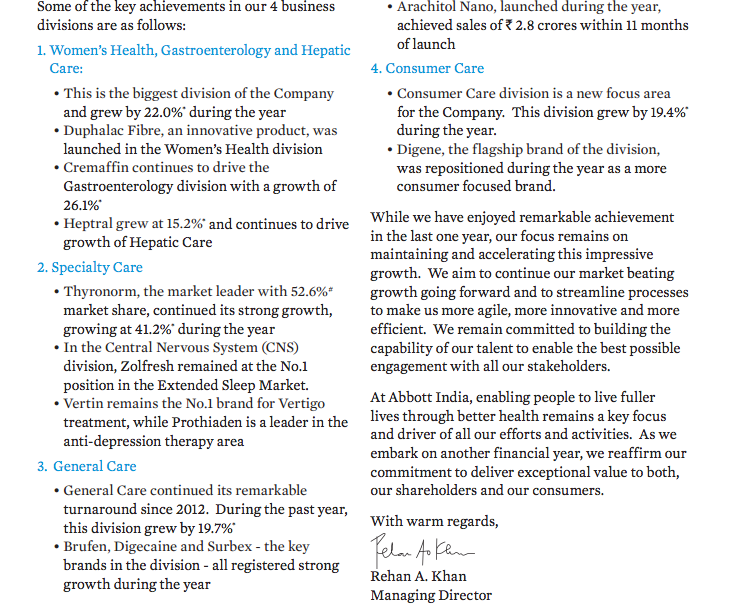

Abbott India is a Multinational pharma company.

The key revenue drivers in India as of now are the following segments:

-Women’s health(biggest division)

-Specialty care(key product: Thyronorm)

-General care

-Consumer care(expected to be future growth driver)

Their parent company in the US, Abbott Nutrition private ltd sells popular products such as Pediasure (Note that these revenues don’t reflect in the Indian company as it is a 100% subsidiary of Abbott USA)

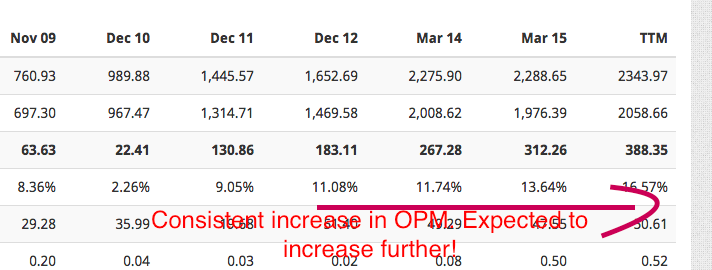

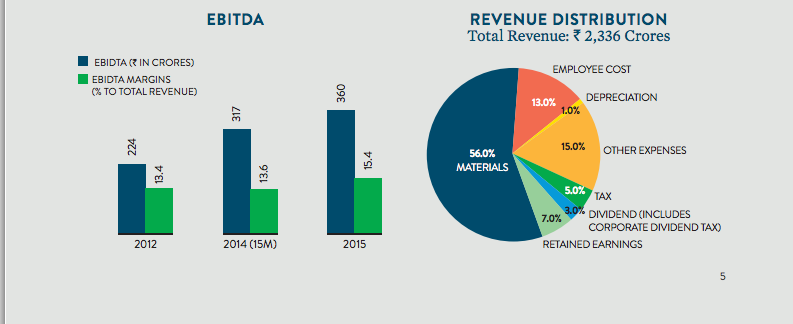

The operating profit margins show a rising trend indicating their focus on increased profitability. They are investing in assets such as real estate currently to develop the future growth drivers through branding and marketing products to consumers with high spending power. The focus seems to be in creating the brand Abbott as is reflected in the big logo which they paste on their products.

Overall, this seems to be a futuristic MNC pharma company with high growth potential. Attaching some images from the recent annual report of the company.

Key risks in my opinion include the decreasing spending power of the Indian consumer, profitability decrease for current products due to governmental norms etc.

Views & criticism from senior members & others are invited as I may be biased due to recent tracking position in my portfolio and family’s portfolio.

Disclosure : Recent tracking position

Highlights of the call by Capital Mkt

For the quarter ended Sept 2015, the consolidated operating revenue increased by 19% to Rs 519.51 crore, Advertisement revenue increased 27% to Rs 388.96 crore. Circulation revenue was up by 3.5% to Rs 99.83 crore. The net profit increased by 61% to Rs 91.28 crore.On standalone basis, the company reported 7% growth in revenue to Rs 437.26 crore. Advertising revenues grew 9% to Rs 312.74 crore, Circulation revenue was up by 3% to Rs 93.87 crore. The net profit grew 4% at Rs 58.31 crore.The company has discontinued publication of Cityplus in Q2.

Dainik Jagran’s ad growth was driven by mix of yield improvement (50%) and volumes (50%) while growth for other editions primarily driven by volume increase. October-2015 has seen better than expected ad growth, mgmt expects at least 10% growth till Diwali. UP has started to get its due share with improving national advertisement.

Madhya Pradesh market is going very slow. The mgmt said that local market is low while national one is not impacted. Bihar, U.P. doing well.City plus had 0.7% impact on the ad growth.

The sector which has contributed to advertisement revenue growth are automobile, white goods and online shopping companies. Auto did excellently. Online shopping also did well but the company has not carried every company ads to protect rates. Retail on local side is picking up.

Radio operating revenue grew 8% to Rs 55.5 crore, driven by yield improvement. EBITDA stood at Rs 16 crore registering decline of 2% with EBITDA margin of 29% vs 32.1% in Q2 FY15. EBITDA was impacted by higher provision for license of Rs 3.5 crore. The net profit was Rs 12 crore. In H1, core market has grown by 10-12%. Utilization has not grown. Both large and small markets have grown, large markets grown on rate hike and small market on volume. Consumer durable. Government and e-commerce companies have helped ad revenue growth for H1. The company will take rate hike in radio business. 8% growth is sustainable.

There was improvement per copy realization especially in Midday.65% digital ad revenue growth for Q2. Rs 5 crore run-rate per quarter in digital biz.

I next – increased share in core market after its re-launch. Circulation improved 55%.Newsprint consumption for H1 was 80000 tonnes. The mgmt said that newsprint price will remain stable.

Land parcel – always looking for disposal of it, at right price.The capex for Jagran Prakashan is Rs 60 – 70 crore for FY16.Net Debt stands at Rs 104 crore for the group as on 30th September 2015.Tax rate for FY17 will be 27-28%.

I feel there is a difference in the point of view of FIIs and DIIs towards Indigo and aviation sector in general. The folks in the west are closer to the happenings on crude front (disruption owing to fracking, US becoming energy sufficient from crude importer sometime back etc.) and I feel they are seeing crude at low levels for good amount of time. Besides, they are seeing how Airlines in the US are making money owing to low crude. Most of the marquee investors in Indigo also own LCCs in the west, as per the article above.

On the other hand, the crude impact is yet to be fully play out and hence appreciated by the Indian firms, hence the DIIs have probably not bought into this yet. Also, Indian aviation industry has had a terrible track record in the last decade.

Overall, I feel once Indigo starts throwing dividends, indian investors will start flocking to it.

Vijay