Obviously, it has to merge and shareholders will get Strides shares in ratio announced.

Posts tagged Value Pickr

Duke Offshore – Hidden Gem? (22-09-2015)

In small cos generally we bet on Jockey driving the co.

Who and how good is the Jockey Avik in Duke? does he has the growth mindset?Whats been the track record,his educational qualifications?

Is the growth mindset there? Whats the moat for the co?

Heard for first time that AGM got adjourned due to lack of quorum ie atleast 15 SH shud be present.V strange.Do u know any body who attended the AGM?

Duke Offshore – Hidden Gem? (22-09-2015)

Adding to the findings. Generally oil firms hire patrol vessels for their offshore assets on long term lease. Also couldn’t find any competitor who offers patrol services instead of leasing boats. So market opportunity is good.

Strides_Arcolab (22-09-2015)

Will shasun delist once the merger completes or will it continue to trade on the stock exchange ?

Skipper Ltd., distributing Power and Water, Is it a moat in making? (22-09-2015)

Hi Sodhi,

Thanks for sharing this new story. I have been tracking this Company from past one week. Don’t know much about the Company but read its latest annual report.

Some of the important extracts from the Annual Report are the following:

Following are some of the important links:

http://www.skipperlimited.com/pdf/Skipper%20Concall%20Q1’FY%2016.pdf

http://www.careratings.com/upload/CompanyFiles/PR/SKIPPER%20LIMITED-09-02-2015.pdf

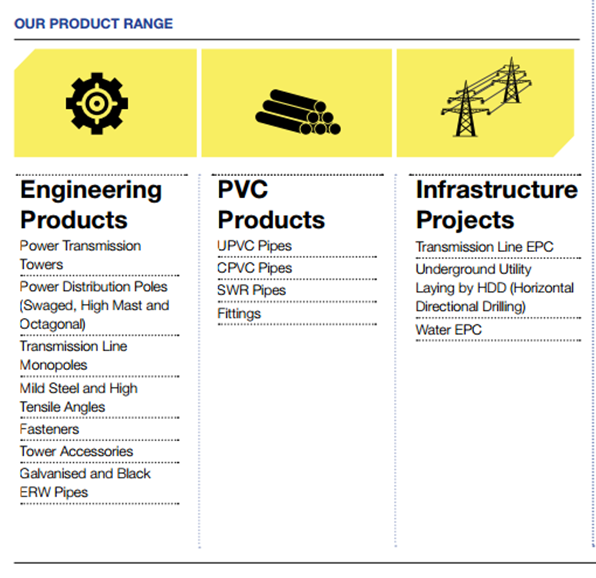

The Company has become the manufacturing partner of Sekisui a Japanese Company which is one of the world’s leading manufacturers of CPVC compound, for manufacturing premium quality CPVC pipes.

Secondly the Company has entered into tie up with WAVIN, a Netherland based Company, which is one of the world’s most renowned plumbing technology companies, for launching in India, the most advanced plumbing systems in the world. With these the Company is hopeful of becoming a Pan India brand in the PVC piping space in the near future.

The Annual Report seems to be of Standard Quality and carries the following vision statement:

“To be a billion dollar company by 2020 that is focused on producing industrialised, market oriented and finished products and services, with an increasing affinity to customer-centricity.”

Important Points Noticed:

1) 1600+ Employees as on date and growing;

2) Largest player in eastern India with unrivalled leadership for all T&D projects announced by the Government of India for east and northeast India.

3) 30 years+ Domain knowledge across towers and pipes industry.

4) OUR MANUFACTURING FACILITIES We have three state-of-the-art manufacturing facilities – two at NH-6, Jalan Complex, Jangalpur, Howrah and a major one at NH-6, Uluberia, Howrah.

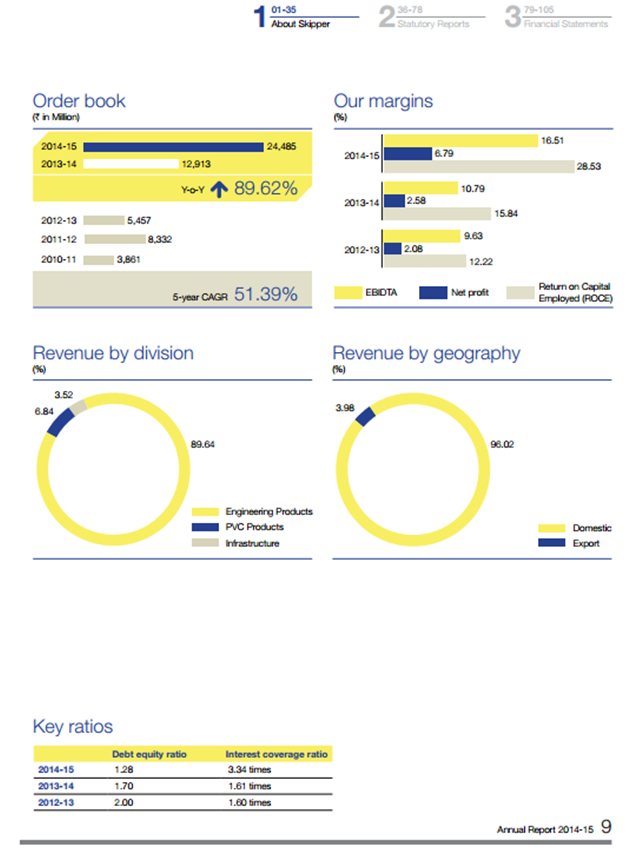

5) 51.39% 5-year CAGR

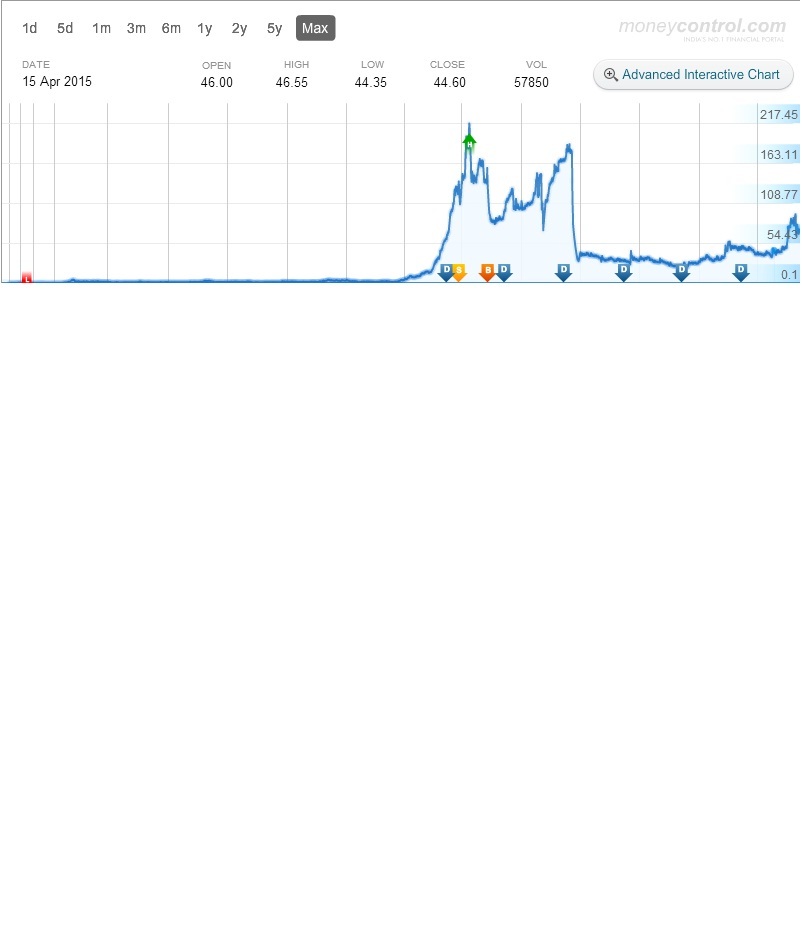

6) Trading and Deliverable Data indicates that day in and day out the deliverable of total shares are > 75% coupled with rise of share price is really noticeable for such small cap Company (Please verify with the link and search- http://www.bseindia.com/markets/equity/EQReports/StockPrcHistori.aspx?flag=0&expandable=7)

Positives (Views)

1) Numbers and Margins are improving year after year;

2) Huge deficit in India for Power and opportunity to tap with New Government (The per capita consumption of power in India is around 90 kVA per person, compared to the global per capita consumption of 313 kVA per person and China’s 447 kVA per person);

Negatives (Views)

1) Power Sector is highly regulated in India and it is not very often that we see multibagger in this sector;

2) High Debt sitting in Balance Sheet.

Questions:

1) In the Annual Report “asset-light approach” is mentioned . Unable to get to know about the dynamics and model.

2) Does anybody have any idea about the promoters? Basically want to know about integrity and shareholder friendliness of the promoters?

Lets discuss this Company in detail, this might be a great story in the making which will truly unfold as time progresses.

Disc: Not invested yet but tempted.

Regards,

Gaurav

Skipper Ltd., distributing Power and Water, Is it a moat in making? (22-09-2015)

Hi Sodhi,

Thanks for sharing this new story. I have been tracking this Company from past one week. Don’t know much about the Company but read its latest annual report.

Some of the important extracts from the Annual Report are the following:

Following are some of the important links:

http://www.skipperlimited.com/pdf/Skipper%20Concall%20Q1’FY%2016.pdf

http://www.careratings.com/upload/CompanyFiles/PR/SKIPPER%20LIMITED-09-02-2015.pdf

The Company has become the manufacturing partner of Sekisui a Japanese Company which is one of the world’s leading manufacturers of CPVC compound, for manufacturing premium quality CPVC pipes.

Secondly the Company has entered into tie up with WAVIN, a Netherland based Company, which is one of the world’s most renowned plumbing technology companies, for launching in India, the most advanced plumbing systems in the world. With these the Company is hopeful of becoming a Pan India brand in the PVC piping space in the near future.

The Annual Report seems to be of Standard Quality and carries the following vision statement:

“To be a billion dollar company by 2020 that is focused on producing industrialised, market oriented and finished products and services, with an increasing affinity to customer-centricity.”

Important Points Noticed:

1) 1600+ Employees as on date and growing;

2) Largest player in eastern India with unrivalled leadership for all T&D projects announced by the Government of India for east and northeast India.

3) 30 years+ Domain knowledge across towers and pipes industry.

4) OUR MANUFACTURING FACILITIES We have three state-of-the-art manufacturing facilities – two at NH-6, Jalan Complex, Jangalpur, Howrah and a major one at NH-6, Uluberia, Howrah.

5) 51.39% 5-year CAGR

6) Trading and Deliverable Data indicates that day in and day out the deliverable of total shares are > 75% coupled with rise of share price is really noticeable for such small cap Company (Please verify with the link and search- http://www.bseindia.com/markets/equity/EQReports/StockPrcHistori.aspx?flag=0&expandable=7)

Positives (Views)

1) Numbers and Margins are improving year after year;

2) Huge deficit in India for Power and opportunity to tap with New Government (The per capita consumption of power in India is around 90 kVA per person, compared to the global per capita consumption of 313 kVA per person and China’s 447 kVA per person);

Negatives (Views)

1) Power Sector is highly regulated in India and it is not very often that we see multibagger in this sector;

2) High Debt sitting in Balance Sheet.

Questions:

1) In the Annual Report “asset-light approach” is mentioned . Unable to get to know about the dynamics and model.

2) Does anybody have any idea about the promoters? Basically want to know about integrity and shareholder friendliness of the promoters?

Lets discuss this Company in detail, this might be a great story in the making which will truly unfold as time progresses.

Disc: Not invested yet but tempted.

Regards,

Gaurav

Motherson sumi : Recent opportunity to buy (22-09-2015)

Mr Sehgal,chairman of MS gave interview on the VW and Maruti.

Motherson sumi : Recent opportunity to buy (22-09-2015)

Its a great company facing difficult times; it can be worth buying when news are bad for a good quality stock. But even at current price the stock is not cheap. Its still a expensive stock above 30 PE & with negative news of Maruti and VW there there growth will surely be impacted.

Yes but a good company to keep under watch after the recent correction.

Motherson sumi : Recent opportunity to buy (22-09-2015)

Shares of Motherson Sumi extended losses for second consecutive day,

falling over 8 percent intraday on Tuesday. The stock was at 52-week

low of Rs 239.65 per share and down 14 percent year-to-date due to

concerns around one of its biggest clients Volkswagen.

The German carmaker has been accused of cheating on diesel emission

tests in the USA and may face penalties of up to USD 18 billion.

CLSA maintains an underperform rating on the stock and warns of

adverse impact if Volkswagen’s regulatory issues spill over to Europe.

Currently, Motherson has a limited exposure to Volkswagen in the USA.

Volkswagen is a key customer for Motherson in Europe and sales to its

group contributed 44 percent of its consolidated revenue in FY15.

According to CLSA estimates, if Motherson’s revenue from Volkswagen

group declines by 10 percent, it could result in 6 percent downside to

FY17 consolidated earnings per share (EPS).

“We continue to remain cautious on Motherson shares given the slow

pace of Indian auto demand recovery and slower-than-expected margin

improvement.

We believe that these regulatory issues for VW Group will be an

additional overhang on the stock in the near term until more clarity

emerges,” CLSA says in a note.In a response to CNBC-TV18, management

of Motherson Sumi has said that the company has only two big plants in

USA and are not affected by VW issue in any manner.

However, trouble for the German car maker has spread to South Korea as

the country’s environment ministry will conduct an investigation into

emissions of Volkswagen AG and Audi diesel cars after the firm

admitted rigging emissions tests on diesel-powered vehicles in the

United States.Meanwhile, Credit Suisse has already raised an alarm of

Motherson Sumi’s slowdown in domestic business.

“Motherson’s near dominance with Maruti is reducing as the

four-wheeler manufacturer is decreasing its single vendor

concentration. Maruti is in process of enforcing its single vendor not

having more than 70 percent share. Hence, Motherson which enjoys 85

percent share in Maruti component parts will suffer,” Credit Suisse

said.