@djinnis – Thanks for sharing the information. Additionally as per Money control data it seems almost 41% of promoters holding is pledged. Can somebody please explain the rational behind this?

Posts in category Value Pickr

Narayana Hrudayalaya Ltd (11-08-2024)

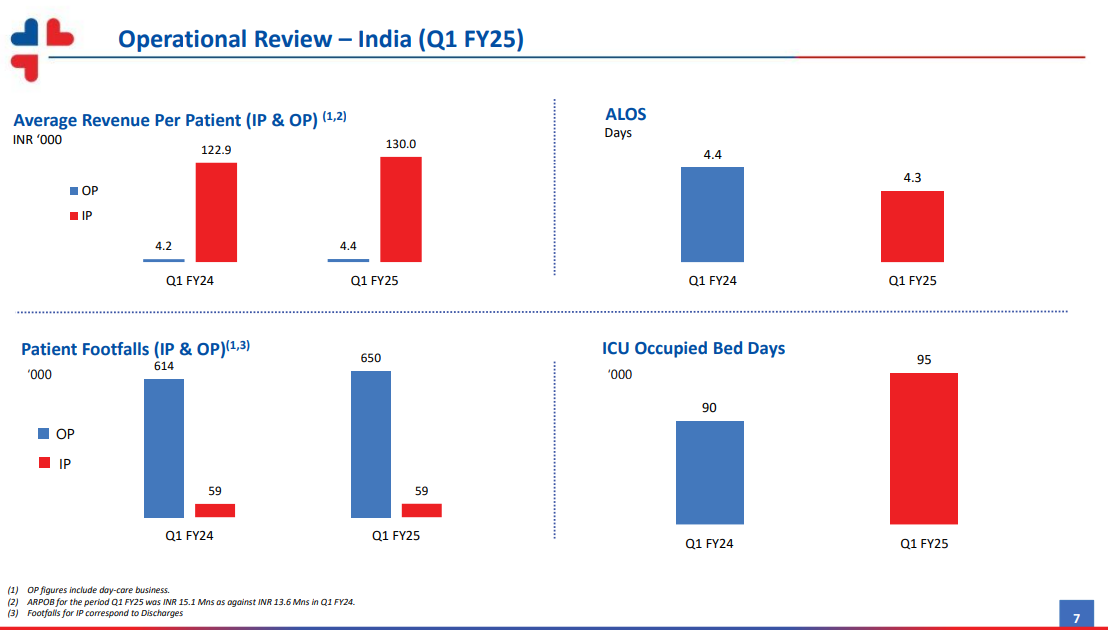

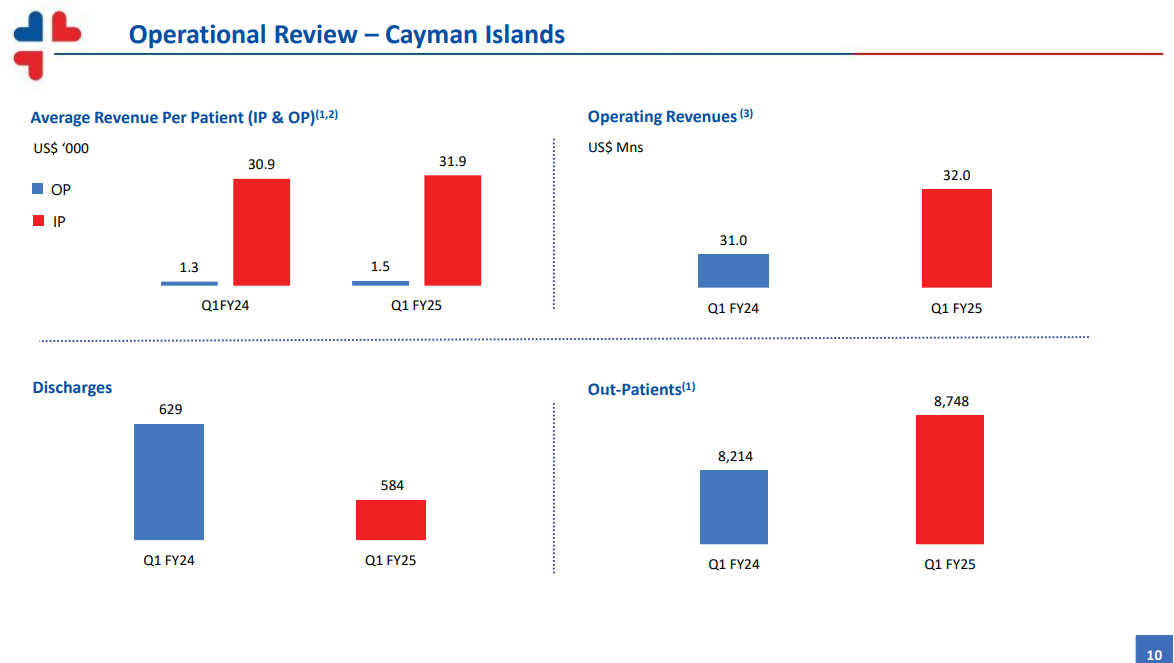

Q1 FY25 Concall Highlights

-

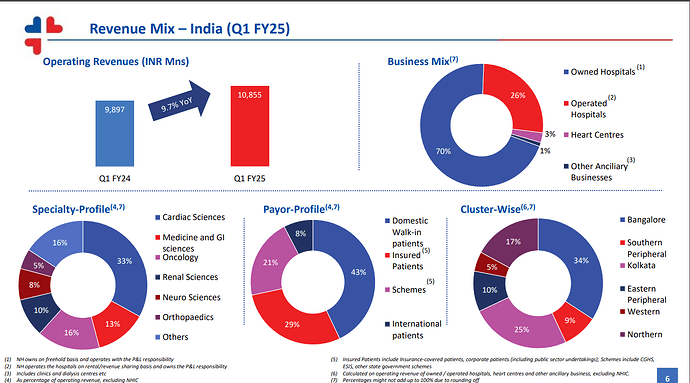

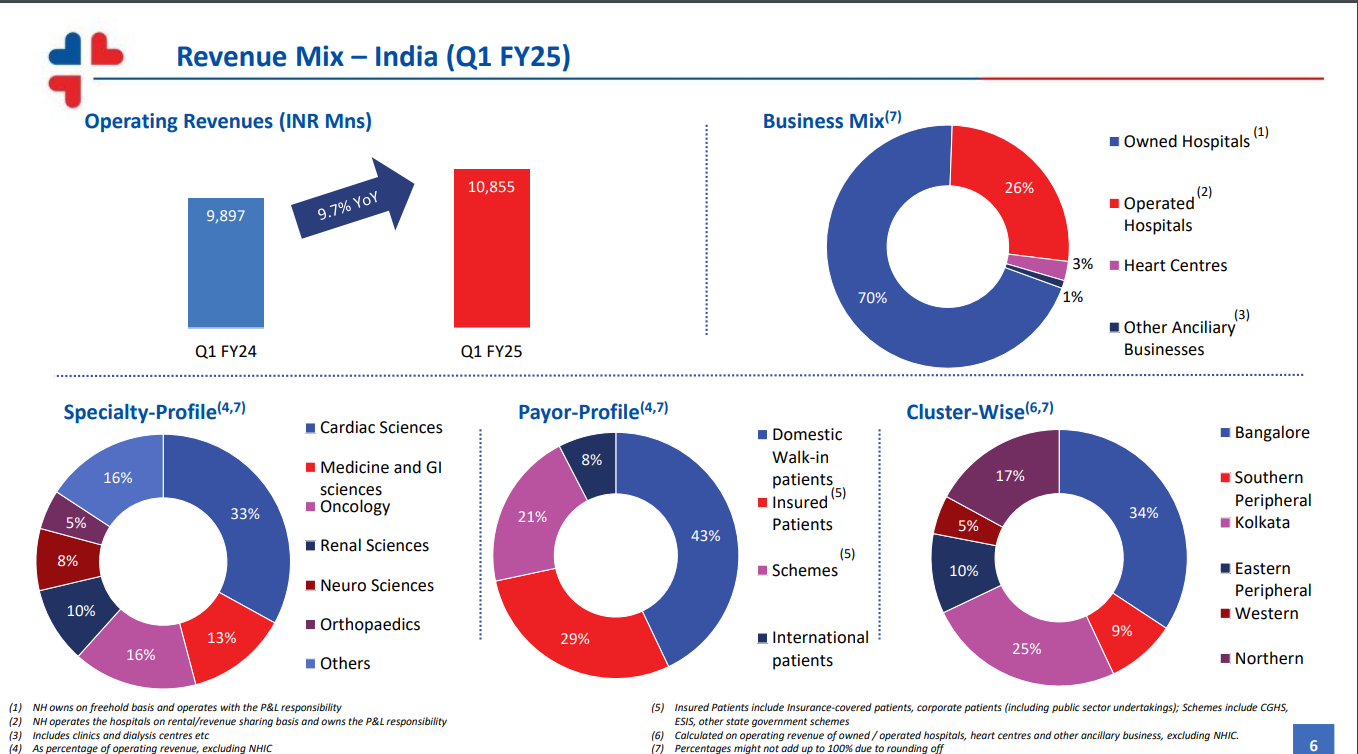

Consolidated operating revenues of INR 13,410 mn in Q1 FY25, an increase of 8.7% YoY and 4.8% QoQ.

-

Consolidated EBITDA of INR 3,274 mn in Q1 FY25 at margin of 24.4%, and consolidated PAT of INR 2,015 mn for Q1 FY25 at a margin of 15.0%.

-

Consolidated Total Borrowings less Cash & Bank Balance and Investments of INR 1,549 mn as on 30th June 2024**, i.e. net debt to equity ratio of 0.05** (Out of which, debt worth US$ 75.0 mn is foreign currency denominated).

-

-

-

-

Revenue from NHIC and NHIL stood at INR 80 mn and EBITDA stood at -INR 120.8 mn for Q1 FY25.

-

Kolkata Greenfield capex- The estimated capex would be INR 1000 cr and in the first phase, 350 beds will be built

-

Bangalore greenfield capex- Estimated capex to be INR 500 cr, bed capacity yet to be finalized

-

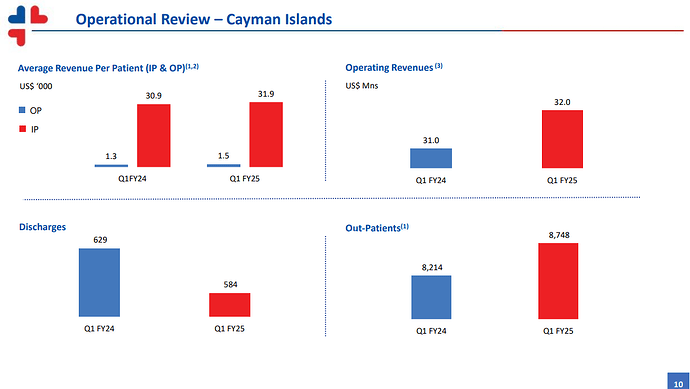

Cayman facility- NH will see margin dilution for some time due to the upcoming Cayman facility capex due to high fixed costs. The new facility will fill the gaps on NH’s existing offerings in Cayman. The existing Cayman facility is also seeing a saturation point, so the management feels it as a good time to go for a new facility

-

The insurance facility is currently limited to Narayana hospitals across India. In future, the management sees that the insurance facility will not be provided all the major hospitals like we see in normal insurances today and will operate in a narrow network.

-

Debtor days- Comparing YoY, we are at similar levels. But comparing QoQ, we have deteriorated by about 8-10 days as in Q4 most of the collections happen. The management expects the debtor days to improve in the next quarter.

-

Company is focusing more on domestic patients and less on international patients. Management is OK if the international patient’s revenue goes down to 0% in next 5 years. As per the mgmt., they never differentiated on the prices for international patients and domestic patients (Superb management quality according to me, I know investors might not like it)

-

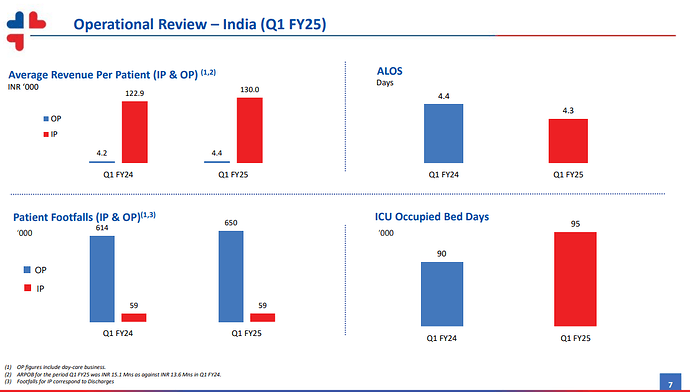

Occupancy levels in Q1 was around 60%

360 One WAM Ltd (Erstwhile IIFL Wealth) (11-08-2024)

I saw that on the exchange, thanks. Let’s see what is the reaction of the market participants tomorrow.

Smallcap momentum portfolio (11-08-2024)

I don’t think any caution is necessary regarding 360ONE; have not planned any.

Looks like a bunch of apprehensions without any proof. 360ONE has responded to the exchanges also.

Let us wait and see.

Oriana Power – SME play on Renewable Energy (11-08-2024)

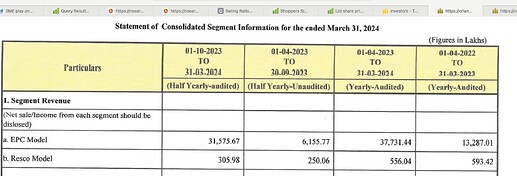

I looked at the financial statements filed by the company so far and its IPO RHP, and was not convinced about the quality of reporting. Highlighting some of the issues I found:

- As per the RHP, the company reported a standalone revenue of Rs. 133 Cr in FY2023, out of which, Rs. 50.6 Cr came from EPC work carried out for subsidiary SPV companies. The consolidated revenue for the same year was reported to be Rs. 136 Cr. This would imply that the subsidiaries earned revenue of 136 – (133 – 50.6) = 53.6 Cr during the year. However, if you aggregate the individual revenue figures of subsidiary companies (mentioned in RHP), you arrive at subsidiary sales of Rs. 5-6 Cr. This is also corroborated by the segmental break up of revenue reported as part of FY2024 financial report.

For me, this raises a lot of questions on the overall reliability of the financials being reported by the company.

- The other part is the RESCO business itself. It has hardly been generating any revenue. I understand that many of the projects are still under construction. But, if one goes by the fixed asset schedule in the consolidated balance sheet over the last two years, it is clear that a significant value of capex has been commissioned and therefore included in PPE and not CWIP.

Assuming most of the fixed assets belong to the RESCO business (which is a reasonable assumption, since there are no fixed assets on the standalone balance sheet), the revenue generated by the segment seems suboptimal. The ROCE of the segment looks poorer.

- Coming to the recent announcement related to the electrolyser business, I could not find any information regarding the contours of the project. I tried to gather some information on the project-partner Splitwaters, but couldn’t really find anything that could establish their ability to set up a manufacturing capacity of 1 GW. Splitwater itself seems to be small scale player.

Further, I really wonder if it is a wise idea to go after a new line of business before the company has established itself in the current one, especially with regards to the RESCO business.

Like many other investors in the current market, I was excited about the prospects of the company, given the many sectoral tailwinds, impressive growth shown by the company and reputed names in its order book/client list. But, having gone through the available data deeply, it seems a lot of questions need to be answered before one can take an informed decision.

Maybe, other forum members can add some insights.

Xpro India – getting bigger? (11-08-2024)

Ravi – I had the same question and checked with Xpro’s IR. I received a prompt response, which I have reproduced below. This makes sense to me.

Rs.139.84 million transferred from designated bank account to CC accounts and utilised therefrom. Rs. 259.58 million has been used directly from the designated account for settlement of working capital related bills. This internal bank transfer has been detailed in the monitoring agency report. Trust this clarifies.

Parameters to check before buying a stock (11-08-2024)

You can have a look at their track record and education. But its not possible to read about management a lot of times for smaller companies. Sometimes its also implied in the Speech and aspirations while it also reflects in the commitments and ACTIONS doe by them.

So there are some direct and indirect wyas as well. I rely on indirect ways more than direct.

Prevest Denpro Limited (11-08-2024)

Playing out exactly as a below average student…