Please share the link or source about essar group legal troubles.

Posts in category Value Pickr

Rohit’s Portfolio : Requesting Feedback (03-08-2024)

With time have started to get more confident in timing entry/exit into stocks. Up 27% for the year (decent considering the size of the portfolio and no SMEs/new IPOs)

Key exits:

a)Narayana Hrudalaya – Mgmt is guiding for revenue and profit normalization. Still decently valued but why be bullish when mgmt is conservative?

b) Reliance – sold @2970. Was always a trading bet for me, will reenter if/when it corrects 10-15%. As always the play is to get the free businesses – Reliance Retail, Jio etc.

c) ICICI Bank – Sold at all time high P/B. Bit of a headwind in the financials space, stocks isn’t moving much – felt prudent to take profits and re-enter if correction happens

d) KPIT Tech – Sold @1500, missed 30% more rally but I feel we are at peak growth and peak PE. Kind of feel that another TATA ELXSI will play out soon. But its an insanely good business and superb execution by promoters. When I first bought it, it was 1/10 of ELXSI MCap, now its 20% more.

| Symbol | Sector | P&L | %Allocation |

|---|---|---|---|

| NEULANDLAB | Pharma | 221.24% | 8.8% |

| TIPSINDLTD | Consumption | 59.73% | 8.4% |

| POLYCAB | Infrastructure | 105.95% | 7.8% |

| GRWRHITECH | Auto | 33.75% | 6.9% |

| GRAVITA | Waste Management | 133.52% | 6.7% |

| NCC | Infrastructure | 111.51% | 6.6% |

| SWSOLAR | Energy | 57.62% | 6.2% |

| TATAPOWER | Energy | 98.58% | 5.6% |

| RACLGEAR | Auto | 47.95% | 4.4% |

| IEX | Energy | 20.90% | 3.5% |

| AARTIIND | Speciality Chemicals | 21.09% | 2.4% |

| VAIBHAVGBL | Consumption | -11.49% | 2.4% |

| PRAKASH | Metals | 22.24% | 2.3% |

| KDDL | Consumption | 37.48% | 2.3% |

| SENCO | Consumer | 12.78% | 2.2% |

| MASTEK | IT | 21.30% | 2.1% |

| EQUITASBNK | Financials | -18.57% | 2.1% |

| SAMHI | Consumption | -1.65% | 1.8% |

| SBCL | Energy | 20.82% | 1.6% |

| GPIL | Metals | 4.08% | 1.6% |

| INOXWIND | Energy | 21.43% | 1.5% |

| POLYPLEX | Consumption | 12.92% | 1.4% |

| BALAJI AMINES | Speciality Chemicals | 8.53% | 1.0% |

| VALOR ESTATE | Real Estate | -1.71% | 1.0% |

| APLAPOLLO | Infrastructure | -5.63% | 0.9% |

| KAJARIA CERAMICS | Infrastructure | 1.97% | 0.8% |

| NITIN SPINNER | Textiles | 1.57% | 0.7% |

| WAAREE RTL | Energy | -12.09% | 0.3% |

| EYANTRA Ventures | Consumptions | 16.20% | 0.2% |

| Gold Bond | Gold | 92.16% | 0.6% |

Would be great to get feedback on top allocations and new sectors to look at ![]()

Basilic Fly Studio Ltd (03-08-2024)

As management informed in concall, Growth of less then 30% by sep 2024. After that sept to March 2025 growth of 50%. In addition, One of US acquisition where they have 300 Artist. Hollywood strike finished. One more thing I am positive about cost of good VFX in developed world is 4 times then in India, so they have to come to India to reduce their cost.

D: Invested

Gujarat Ambuja Exports – aMAIZEIng Story (03-08-2024)

Not good result

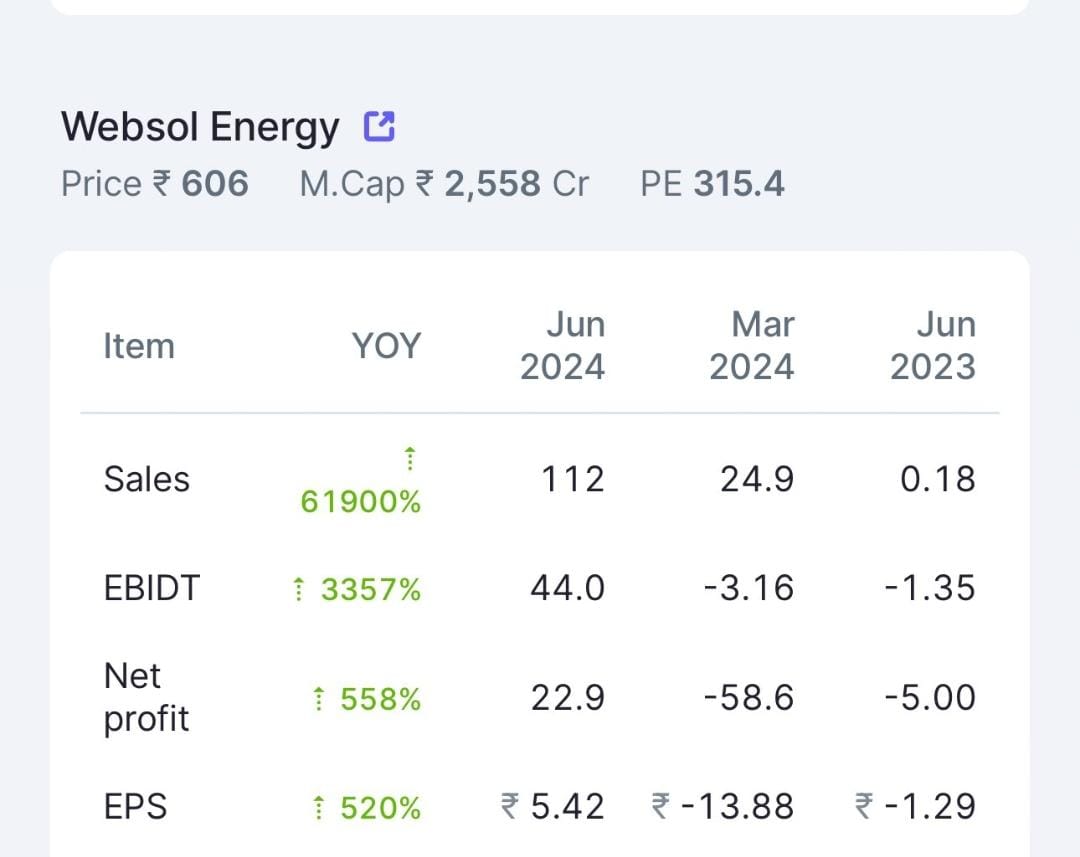

Websol energy system ltd (03-08-2024)

Irrespective of short term price action. It’s clear that we should be sitting at 100cr annual PAT with the current capacity only. Get your valuations hat on. It’s a 10,000 cr mcap company 18 months down the line. Atleast.

4x from here.

Assuming the capex will rampup to 2.4gw by next CY 2025 December. And the company will further have aspirations to double the capacity.

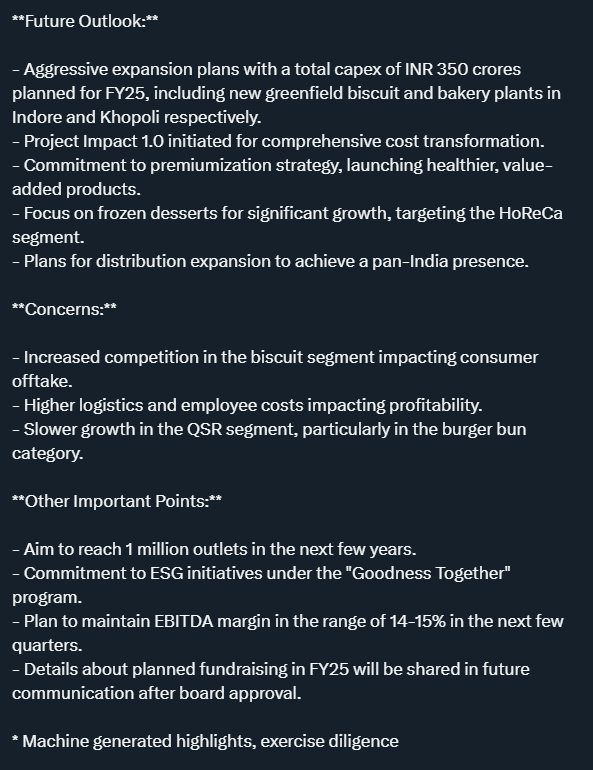

Mrs Bectors Food Specialities: Can it beat the industry? (03-08-2024)

Curtesy – scoutquest

Vaibhav Global ~ Vertically integrated value e-tailer of Jewellery and Lifestyle Products (03-08-2024)

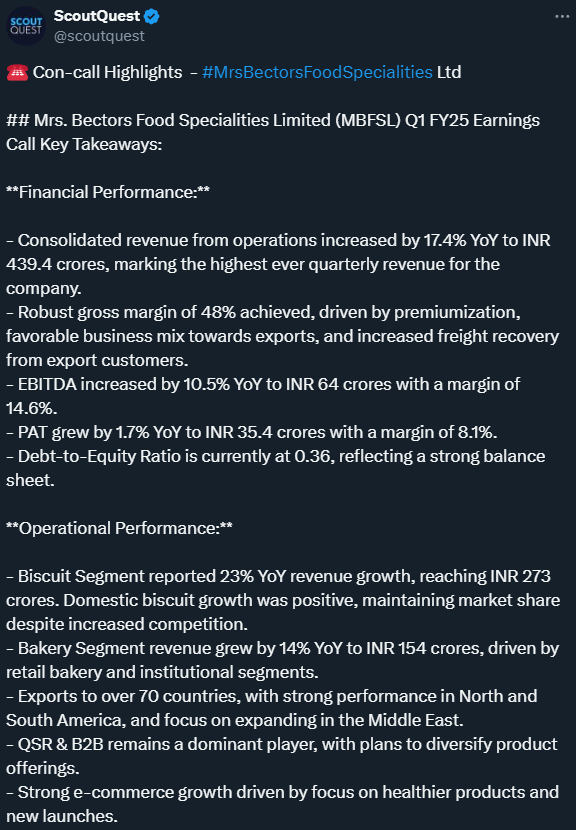

Vaibhav Global Q1 FY25 Concall notes (posting only key takeaways from my POV)

-

Maintains guidance for 14-17% revenue growth in FY25. The range is due to uncertainties due to US elections, else they’d have been confident guiding for 17%

-

Content and broadcasting cost was 20% of topline in Q1, expects to finish the year at 18% of topline. This is a 1.5% YoY growth for the line item. Investments here being made for ramping up their newly acquired online businesses of Ideal World and Mindful Souls as well as the new territory of Germany. They have also spent some amount in improving TV positioning in USA. This line item as % topline has increased from 12.5% in FY20 to around 18% in FY25E. One hopes that a lot of this is leverage and the ratio was settle below 15% once the new businesses reach steady-state. Looks like they are targeting higher growth (mid teens guidance for medium term) via higher investments in content and broadcasting with some leverage.

-

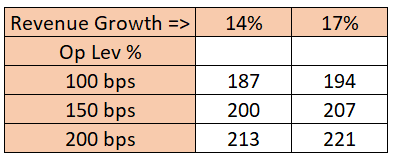

Overall expect to deliver 150-200bps of operating leverage in FY25. Expects 200bps GM expansion due to better product mix, 100bps expansion from employee costs line item and possibly another 50bps from other line items such as travel expenses and freight. There will be a 150bps negative leverage due to B&C costs as discussed above, so net/net there’s a possibility of 150-200bps EBITDAM expansion YoY

If management indeed is able to deliver 15% revenue growth and 200bps EBITDAM improvement over the year, PAT here can comfortably cross 200Cr. Here’s how I see PAT playing out for various combinations of growth and leverage. I have assumed 20cr Other Income and 25% tax rate.

Depending on which scenario plays out, there could be a 50-75% YoY PAT growth and the stock is likely trading between 24-29x FY25 PAT. If the upper end of the PAT assumptions plays out, I won’t be surprised to see the stock trading at 8000Cr MCap.

Chart wise, 273 seems like a strong support zone. I don’t expect the stock to test that support unless there is panic about a US recession. From what I know, recessionary conditions on ground normally top out well before a recession officially shows up in GDP nos. So the worst in terms of consumer sentiment for the business may actually be behind them and that seems to be what management is also indicating. However, Western economies aren’t in the best of health and adverse risks remain which need to be monitored.

Disc: Invested.

Kovai Medical Center and Hospital – Health and Wealth (03-08-2024)

Size of land parcel is very small 1.28 acre only. To build a decent hospital in a Metro city at least 3-5 acres would be required. They had 3 acre land parcel in Chennai earlier as well, had plans to set up a hospital later on dropped that plan & did set up medical college instead.

let’s see how this unfolds

Disc. : Holding from low levels

Journey and Portfolio of a goal-based NEEV investor (03-08-2024)

Fantastic Summary.

While I agree with majority of what has been conveyed but would like to point out few places where the story hits speedbumps.

On the jewelery front, no complaints with execution, marketing or the recent expansions with Carat Lane and overseas Tanishq outlets.

Watches as a category they are doing well. But there is lack of significant growth whether it is in smartwatches or core business. I think two-year CAGR is just 10% when they should be dominating in smartwatches. Again 10% is not bad but it is not something that is exciting.

On the Eyewear division, they have completely dropped the ball. This should have been a business where they could have touched the watches business in terms of revenue but have significantly underperformed with too many changes in management, Franchisee formats etc. They have lost first mover advantage to Lens Kart and others and now changing strategies to try and catch up.

My overall concern is there are Jewelry dependent, and their growth will be tougher with more competition on organized side, city and region-based players now are updating brand presence and ensuring quality and therefore retargeting customers they lost to Tanishq. This is something management themselves acknowledge in FY24 concall.

I love the brand, use it and of course it has had phenomenal staying power over last few decades and shown the ability to manage frequent thorns in the road, but this is just to give a not so rosy picture.This slightly negative viewpoint is just to show that they have hurdles to cover.

P.s : To get to LVMH status they need to upgrade across product, marketing internationally.

Disclosure: Have invested in recent correction through family PF.