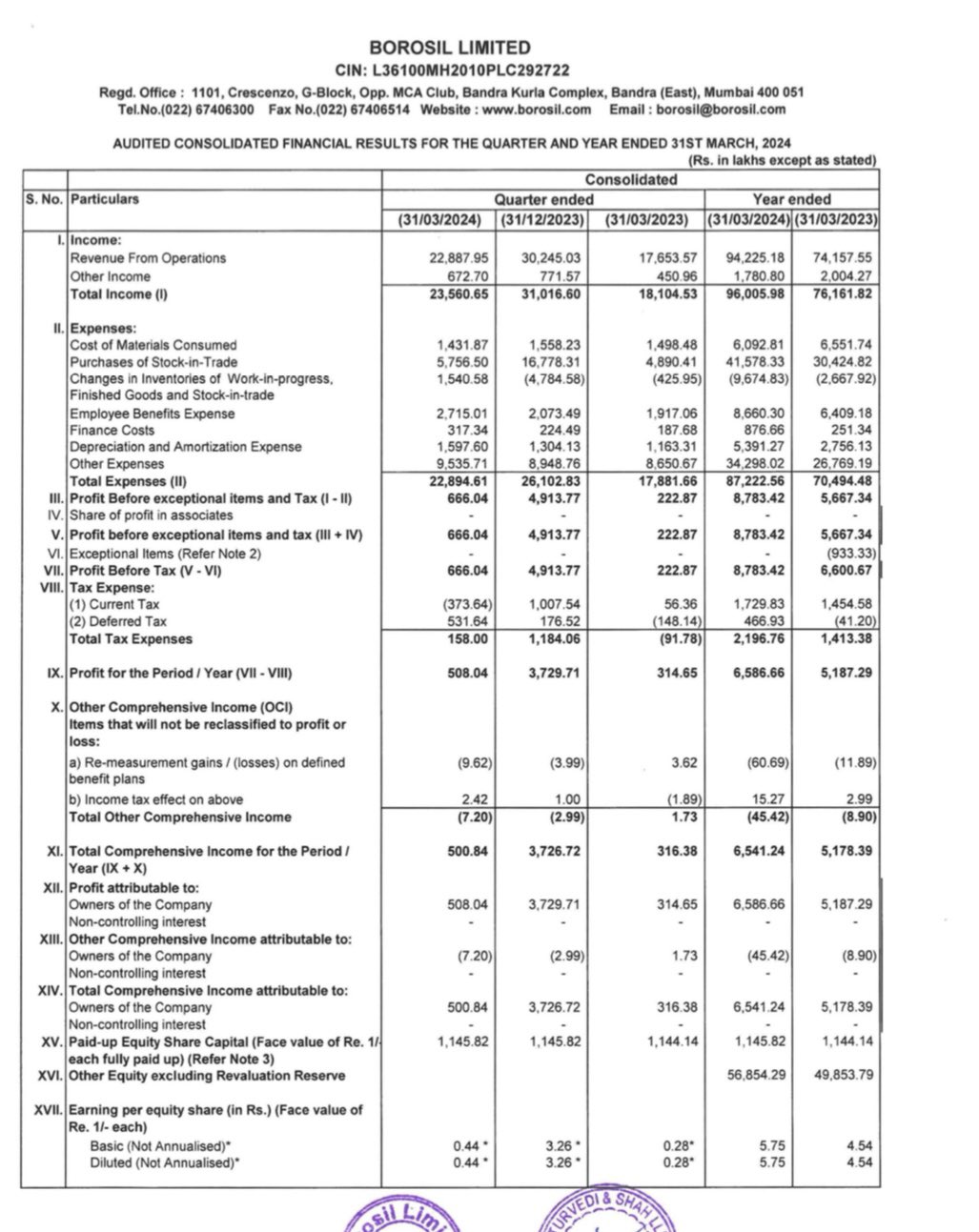

Results are horrible.

Couldn’t by any worse.

No investment rationale coming into play on this counter as on today!

Results are horrible.

Couldn’t by any worse.

No investment rationale coming into play on this counter as on today!

It appears the Q4 results are out and looks good but there seems to be some error in Q3 as it includes demerged entity numbers QOQ which should have been excluded but YOY looks fine

What is the head winds in this stock

Transcripts are already available

77b60446-9c1b-4070-b74d-c941203df1c5.pdf (bseindia.com)

AI generated future growth drivers.

Diversifying and bringing some stability to an equity-heavy PF by adding gold through ETFs or even physical gold, and participating in futures to make some profit are different.

With ETFs, there will be a chance of recovery if we wait, but it can be a long wait. With futures, there will be absolute loss at the end of expiry, and if we add more to recoup our losses for the next expiry, we can lose more if our view is wrong. And the toughest part is the fall that can happen in the middle of the duration, so more funds will be required. Nothing will teach FnO better than participation, so if you are inclined, you can do it with Mini or Guinea and experience, if you have not already. My experience did not feel worth the effort, so I invest and trade in ETFs.

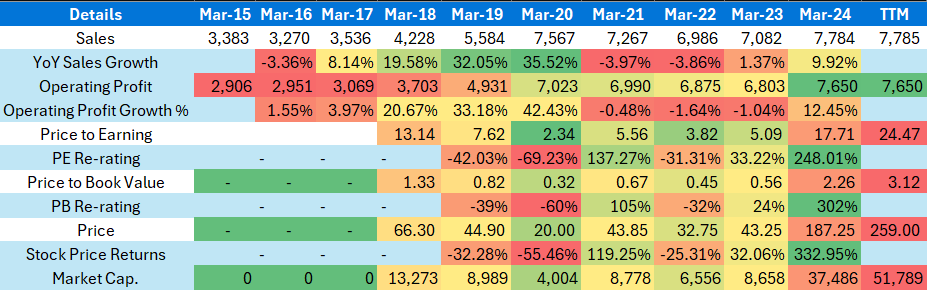

Galaxy announced a fair set of numbers today and seems to be making significant progress on the CAPEX front (CWIP up to 26 Cr for March ending, out of their assumed CAPEX of Rs. 35 Cr).

Providing a summary for everyone on this thread (and myself to refer back to):

Background: company was founded by Mr. Vinod Kangsara (passed away in 2019) – current main promoters are his wife (Indiraben Kangsara) and daughters (Shetal Devang Gor and Tuhina Bera) – who now seem to be NRIs and aren’t actively involved in the business operations. CEO is Mr. Nitin Santoki – who seems to be Rajkot based with a strong presence in the industry (no information on his shareholding). It seems that Mr. Nitin’s family has other companies in associated fields of the industry (common in auto ancillary businesses, wouldn’t consider it to be a corporate governance issue – refer to the link for Adico group below).

Catalyst/Trigger: Change in management post 2019, might have triggered a new approach to the business(speculatio). Dr. Devang Gor who is a Chair at the Department of Radiology in a leading healthcare network in Pennsylvania, USA was appointed on the board in August 2019 after completing an Exec MBA from Temple University (potentially to groom him for this role?).

Key business trigger seems to be a new product development as mentioned by Mr. Nitin in his interview (https://www.youtube.com/watch?v=ygyf4W54XCU&t=1s) – where they are manufacturing roller bearings with a hub casting attached. This saves their customer the time, effort and the cost of otherwise attaching the hub casting separately to the product.

It seems another competitor offering a similar product is Orbit Bearings (also Rajkot based), who has grown significantly by being the first taper roller bearing company to manufacture these bearings with a hub casting (Cylindrical Roller Bearings | Truck Axle Bearings | Taper Roller Bearings | Truck Hub Bearings | Orbit Bearings India Pvt. Ltd.). Orbit Bearings has scaled significantly and did a revenue of Rs. 624 Cr in 2022 with a PBT of Rs. 151 Cr. Orbit has a capacity of 10 Million pcs per annum, and it’s interesting to note that Galaxy has decided to set up a plant which takes their total production capacity to 9.5 Million per annum (in Phase 1)! Other smaller competitors also seem to be equally profitable (Turbo Bearings does a Sale of 99 Cr with a PBT of 27 Cr).

Has anyone studied the bearing industry in greater detail to check how they compare with SKF, Timken, Schaeffler?

https://www.adicogroup.com/international/group-of-companies.html

Why use net block? Should use gross block

Good inights, Rahul.

Thanks for taking the time to prepare this. I think HFCs deserve a separate thread of their own.

Let me chip in my couple of thoughts.

For example, Aptus and India Shelter is heavily held by Westbridge, Aavas by Kedaara, Home first by Warburg Pincus (Orange Clove) etc.

These PE players are basically funds which have end of life. Until these PE funds are on the cap table, expect these companies to face constant bouts of stock supply and therefore, prices may remain compressed despite 25-30% AUM growth and pristine asset quality. At least that is how these A-player stocks are playing out for now.

PNB housing might foray into microfinance under new leadership, Can fin homes might foray into digital transformation and risk management after Ambala incident, but give or take, these are 10-15% growers. Dont expect the moon from them.

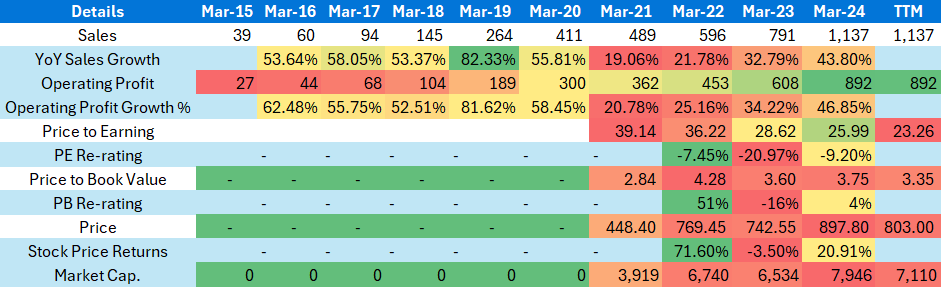

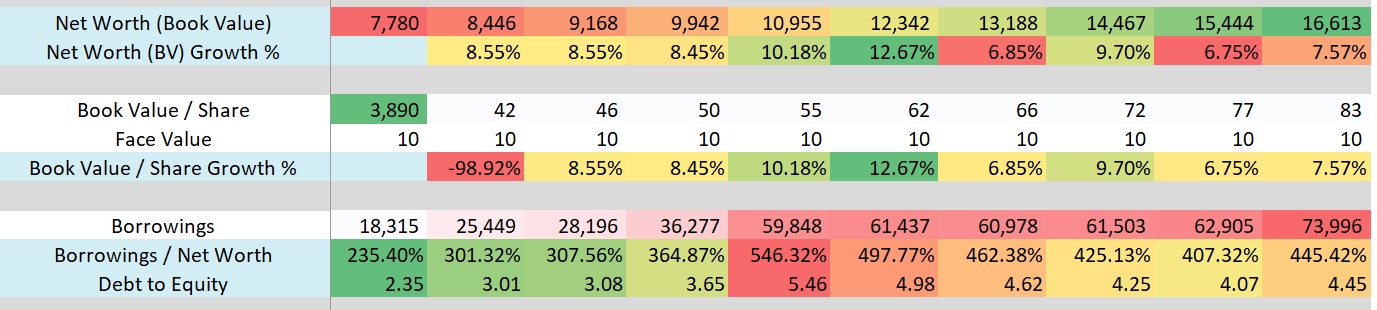

Here’s a look at Hudco at a high level:

In FY24, Hudco’s topline has grown by 9%, operating profits have grown by 12%, however its PB is re-rated from 0.56 PB to 3.12 PB, a whopping 6x PB update. Naturally the price has gained 6x not much because of fundamental growth but because of re-rerating.

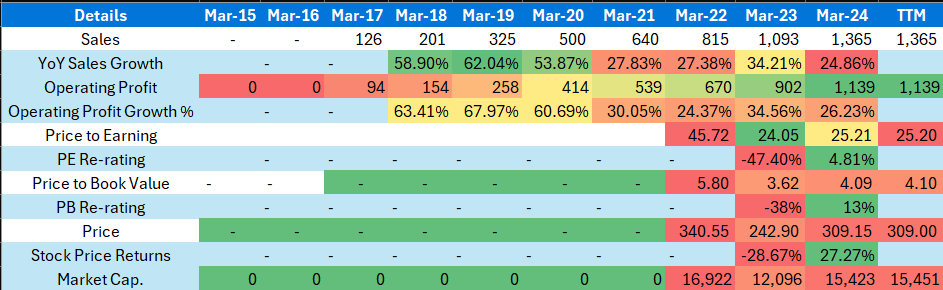

Take a look at an A Player, in comparison:

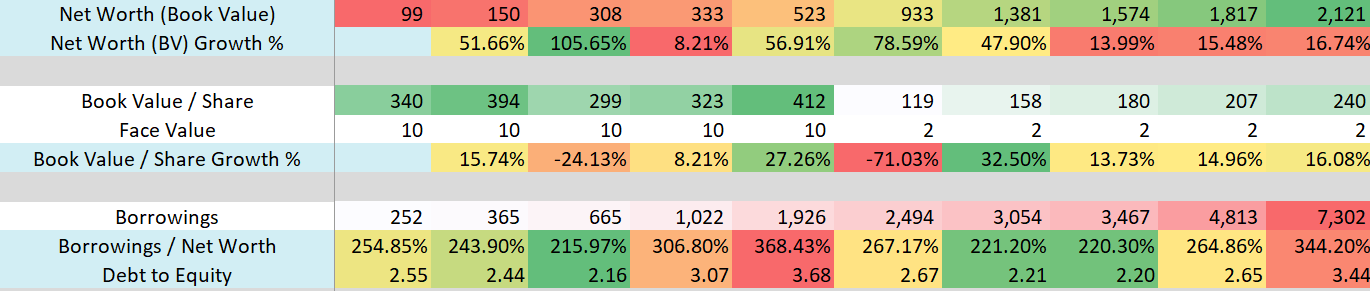

Home First:

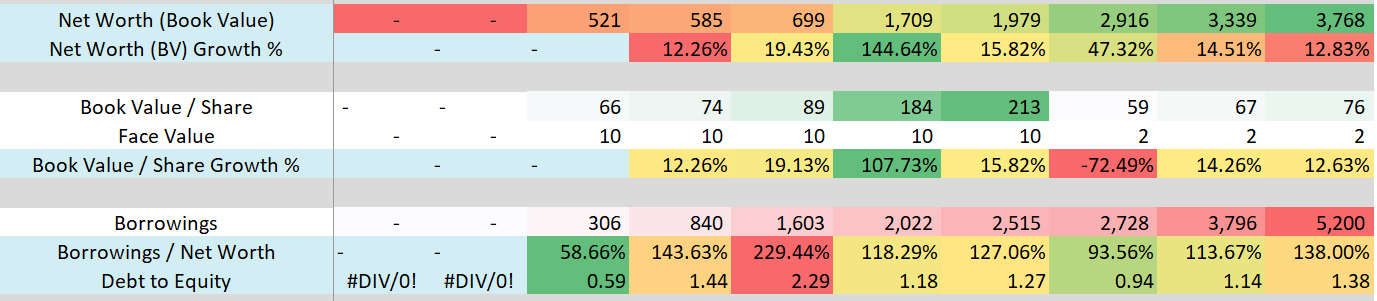

Aptus:

AUM and Book Value Growth wise, Hudco stands nowhere close to the A players:

Hudco’s Balance Sheet metrics:

Hudco’s AUM growth (Derived):

Home First’s Balance Sheet metrics:

Home First’s AUM growth (YoY):

Aptus’s Balance Sheet metrics:

Aptus’s AUM growth (YoY):

Clearly, the A players have better balance sheet, less leverage, higher AUM growth, less delinquencies and credit cost.

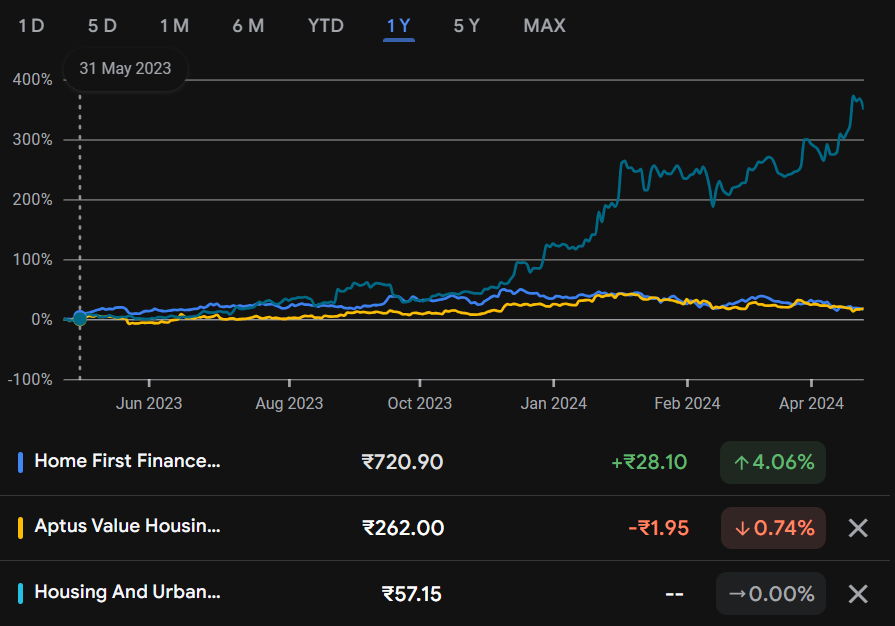

Now look at the price chart of Home first, Aptus and Hudco for last 1 year.

63 -15 = 48 out of 100 still too large for my comfort.

@mayank_raghuwanshi, Mayank, this is how I see Rategain. I have assumed 22% growth. Management has guided for 2,000 crores revenue by FY27 (including ~300 crores inorganic revenues). Margin guidance is 25% by FY27. I am comfortable with 2PEG.

| A | FY24 | FY25 | FY26 | FY27 |

|---|---|---|---|---|

| Revenue | 957 | 1168 | 1424 | 1738 |

| EBITDA | 190 | 257 | 342 | 434 |

| EBITDA Margin | 22% | 24% | 25% | |

| PAT | 145 | 196 | 261 | 332 |

| Current Mcap | 8440 | |||

| Forward PE | 43 | 32 | 25 |

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation . Also note that I recently joined a investment advisory firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.