Thanks! As I am holding this company since long time(& holding it from lower level) and I am trying probe what would be right valuation for this business as revenue quality is also improving due mix from value added products are on rise. I think reasonable PE should be b/w 15-20 but if you see it’s real competitor Pyramid, it has got rich valuation compared TT but it has also better return ration (which I am expecting in future for TT, if they continue on this path).

Posts in category Value Pickr

JK tyres – Catching the speed (16-12-2023)

Recent event at Bangalore

Dollar Industries ltd – Fit Hai Boss (16-12-2023)

Historically it’s been a slow growth company. Good money was made in riding the recovery of the cycle but not from the sales/profit growth.

But yes, Project Lakshya can help them improve market share driven by growth. With increased efficiencies they may be able to deliver better growth or it may make sense to grow at higher rate if the ROE/ROCE improves.

Disc: No reco to buy or sell

Praveen

The HS Portfolio (16-12-2023)

Small Changes in the portfolio. Sold Cochin in last week as it did not play out as expected.

I did add HAL to the mix same day. Have sold that out yesterday.

Present portfolio is almost same on atleast the bigger weights

| Symbol | Average Price | Previous Closing Price | Unrealized P&L Pct. | Current % |

|---|---|---|---|---|

| TATACONSUM | 834 | 955 | 15 | 12.85% |

| CHOLAFIN | 1208 | 1244 | 3 | 10.92% |

| LAURUSLABS | 379 | 386 | 2 | 8.33% |

| HCC | 31 | 32 | 2 | 7.80% |

| COALINDIA | 237 | 350 | 48 | 6.14% |

| NTPC | 239 | 305 | 27 | 5.98% |

| SJVN | 34 | 96 | 184 | 5.64% |

| ADVENZYMES | 367 | 370 | 1 | 5.20% |

| PREMEXPLN | 1285 | 1619 | 26 | 4.72% |

| MOTILALOFS | 1199 | 1215 | 1 | 4.26% |

| ARE&M | 618 | 765 | 24 | 3.58% |

| ZENTEC-T | 779 | 765 | -2 | 3.35% |

| TATASTEEL | 127 | 136 | 7 | 3.19% |

| CCL | 650 | 640 | -2 | 3.18% |

| ZYDUSLIFE | 598 | 646 | 8 | 3.02% |

| TVSMOTOR | 1534 | 2019 | 32 | 2.95% |

| JAICORPLTD | 334 | 336 | 1 | 2.45% |

| DEEPAKFERT | 680 | 658 | -3 | 2.31% |

| WOCKPHARMA | 353 | 415 | 17 | 2.31% |

| HINDCOPPER | 158 | 188 | 18 | 1.10% |

| NETWEB | 873 | 1291 | 48 | 0.38% |

| KRISHANA | 246 | 243 | -1 | 0.14% |

| ECORECO6-XT | 192 | 423 | 120 | 0.12% |

| RELIGARE | 258 | 222 | -14 | 0.06% |

The harsh portfolio! (16-12-2023)

I have been hoping that price dips a bit more and I can buy more. The last time I bought was in Feb 2022, so its been a while. Every few years, PI sees a 30% price drop and I try to buy each time that happens.

Coming to pyroxasulfone, broker reports suggest that it contributes 45-50% of their CSM business which brings in a concentration risk. The last time this happened was in FY17, where pyro was a large part of their CSM business. As a result, their FY18 nos were quite muted and stock also underperformed for a couple of years.

The key difference this time is they have a much larger product basket, which management is hoping can fill the void (if demand for pyro stagnates). Their CSM product basket has increased from 10 at that time to 20-25 now. Also, pharma is a growth driver and is higher gross margin compared to agchem CSM. I actually feel more bullish about their future prospects now, than in 2022 when I had last bought.

Much higher growth, Dharmaj is growing at 25-30% vs Dhanuka growing at 10-12%. On business front, Dhanuka is probably the best managed domestic agchem co.

SmallCap Hunter : Trying to find the dark horses with triggers (16-12-2023)

I am now studying about Adeshwar Meditex. They are company which does marketing and trading of medical disposables like surgical dressings, first aid kits, etc. Recently the promoter has changed. The new promoter has decades of experience in the medical field and has been a minority shareholder in the company since 2017. His son has been the CFO for some time. Together they own upwards of 50% of the company already. If the open offer succeeds fully they will own roughly 86% of the company along with their PACs.

There are a couple of questions that I still have though.

- The current promoter sold her stake at 6.5 rupees per share which is lower than the current market price

- The new promoters haven’t disclosed any plans on what they plan to do with the business. All they have written in the open offer document is that they plan to continue with the same line of business.

So I am still not decided whether I want to invest in the business or not. I will update when my thinking evolves.

Shriram Pistons & Rings Ltd (16-12-2023)

Not aware of any further selling after the one in Nov

That essentially means that out of 88,49,830 equity shares, which KS Kolbenschmidt GmbH holds in the company, only ~3% selling is done.

The harsh global folio! (16-12-2023)

InMode, VFC and BAT are very different.

InMode: I feel very confident about this, and have been buying regularly. Its not very often that one gets to participate in very high ROE, very high margin free cashflow generating business at 10x PE. I am hoping that growth slowdown is temporary.

VFC: Here stock price has gone down when business is facing challenges. I haven’t done anything after February 2023, when I last bought around $25.

BAT: I feel very confident because business has not been affected and its largely a perception issue. Also they are not highly leveraged and are generating a lot of freecashflow.

If you know which stock will move tomorrow, its better to sell everything and buy that. Unfortunately, I dont know that.

Ranvir’s Portfolio (16-12-2023)

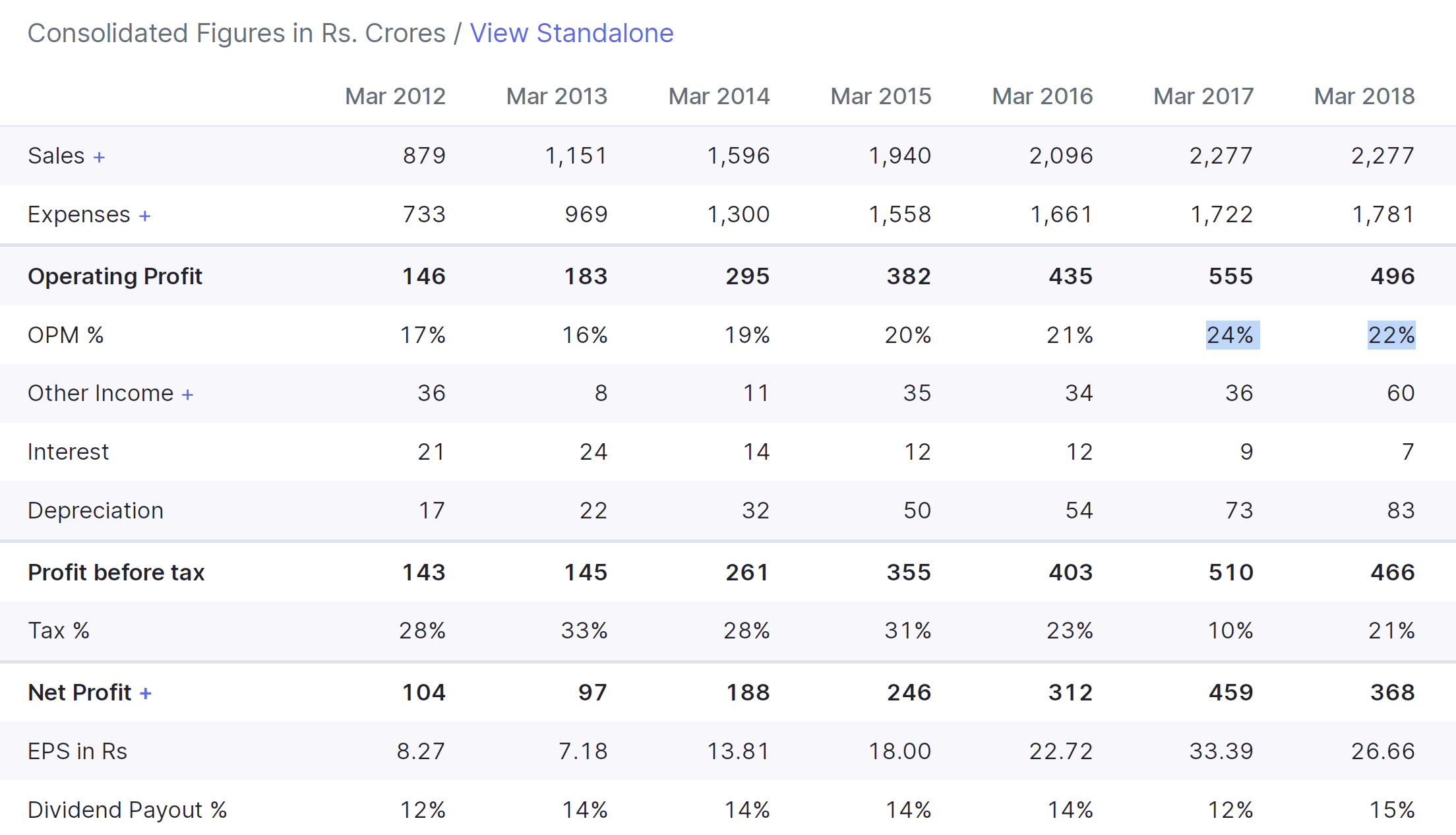

Time Technoplast –

H1 andQ2 updates –

A leading manufacturer of Polymer and Composite materials based storage and other products ( like HDPE pipes, auto components etc )

Strong presence in Asia, MENA regions

Marquee clients include – DuPont, IOL, Gulf Oil, ExxonMobil, Bayer, BASF, Huntsman, GE, L&T etc

Product basket includes –

Polymer based – drums and containers, Jerry cans, Energy storage devices, auto components

HDPE pipes

Composite material based – IBCs (intermediate bilk containers), Composite cylinders, MoX films

H1 financial performance –

Sales- 2274 cr, up 16 pc. Volume growth @ 18 pc

EBITDA- 315 cr, up 22 pc (margins @ 13.9 vs 13.1 pc)

PAT- 126 cr, up 34 pc

Cash Profit – 219, up 23 pc

Share of value added products has gone up from 23 pc (last yr) to 25 pc this yr

Sales for IBCs and composite cylinders grew by 110 pc in H1 vs LY

Segmental performance –

Polymer product sales – 1481 vs 1306 cr, up 13 pc

Composite products sale – 792 vs 661 cr, up 20 pc

H1 capex @ 100 cr. out of this, 40 cr spent towards legacy products. Additional 60 cr spent towards IBCs and Composite cylinders

Other comments –

Demand for HDPE pipes being mainly led by Govt schemes like Har Ghar Jal, Swachh Bharat, Infra spending

Demand for IBCs led by private capex – both brownfield and greenfield. Exports to emerging economies are also doing well

Composite cylinders (LPG) demand being fuelled by PM Ujjwala, orders from IOCL etc

Company receiving overwhelming demand for CNG composite cylinders. These can also be used to store liquid Hydrogen. Fresh Capex initiated for CNG composite cylinders

Composite CNG/LPG cylinders can be a 2000-2500 cr business in 3 yrs time !!! Company commands a mkt share of 75 odd pc in India

IBC business should grow at rates > 15 pc for next couple of years

Aim to reduce Debt by 150 cr via internal accruals (not factoring in the sale of International assets ). Company likely to sell its non core overseas assets this FY. Money received shall be used to further reduce debt and other business purposes. Expected to receive around 1000 cr from the same

Share of value added products to cross 35 pc in next 3 yrs. Once this happens, EBITDA margins should cross 15 pc

Total business likely to cross Rs 5000 cr this FY as second half is always stronger

Disc: holding, Biased, not SEBI registered