Promoter buying in may 2023 and Feb 2023. Why is the promoter holding decreasing then?

Posts in category Value Pickr

Whirlpool of India (05-12-2023)

“Also they will be more open to external growth now that it’s a 51% sub in terms of maybe allowing contract export to group to gain more sales…”

Can you explain a bit more for clarity?

Hitesh portfolio (05-12-2023)

Hi,

I am not the right person to Answer your question as I also have not seen the Crash Or bear Market with Considerable Amount Invested. But I was in the same dilemma 2 years back when I started Investing and asked the similar question to Hitesh Sir and you can refer below:

What I have experienced from my limited experience is that You have to select Best Companies with Nearterm or midterm Growth Potential and your portfolio will do well over long time.

I suggest you before you start investing with considerable capital by your own, Learn Fundamental And Technicals from SOIC and read books of Peter Lynch, Stan Weinstin and Williom O Neil.

After reading and learing all this start practicing with Limited Amount which you afford to loose.

Develop Buying and Selling Rules, System and Process. Fine tune it with Limited Capital.

Once you develop the confidance and you Master Risk Management by which you shall be sure that You should not loose your own capital and even Major Chunk of Paper Profit during Crash or Bear Market then only start by your own with considerable amount.

As Buffet says Investing is Simple but definitely not EASY.

StoveKraft – Kitchen Appliances Company (05-12-2023)

The stock seems to have reacted positively after Income tax inquiries.

Now the company is expanding sales network in the North.

Balkrishna Industries (05-12-2023)

You might be right though YOY we could see a big improvement and PE falling as last December quarter had poor results (eps 5.41).

Hitesh portfolio (05-12-2023)

Hello @hitesh2710 sir ,

I don’t want to get caught in the ambush of the bear market and I have never seen one with much of my capital invested.

I have seen covid but did not act properly there and end up selling things except obviously tax saver fund.

Q1> How would you tread the periods of bear market?

Q2> How can I be ready for bear market without losing the joy of bull market?

Q3> How to be sure that bear market has arrived?

Q4> Any book recommendation to be ready for the bear market?

Q5> Does all the sector go down in bear market or there are outliers?

Q6> Does techno funda approach work in bear market?

Q7> Does all stocks PE correct or there will be some outliers? If yes, what is the percentage of outliers?

This question is more significant as recently I have decided to increase my direct small and midcap portfolio percentage and I don’t want to be caught in ambush.

My portfolio

20% us stocks directly plus index(no new investment now)

20% fixed assets

20% direct small and mid caps stocks

30% ppfas tax saver and nifty index fund

10% small cap mfs

Shree Renuka Sugar Turn around story (05-12-2023)

The Roadmap for Ethanol Blending in India 2020-25,prepared by an inter-Ministerial Committee, estimated ethanol requirement of 1016 crore litres to achieve 20% blending targets in ESY 2025-26. The current ethanol production capacity is 1364 crore litre.

Ambika Cotton Mills (05-12-2023)

This question was asked and discussed multiple times in this thread. Please help yourself searching this thread with “buyback” and repost your question if it’s over and above what’s already answered!

Globus Spirits (05-12-2023)

The company had a very tough time in the past 8 to 9 quarters. As far as input costs are concerned, I don’t think the situation could get any worse than it is. The only silver lining could be that there were no issues in offtake by OMCs. Broken rice prices started moving up first followed by the power prices. After the coal prices came down there was some respite in power prices. But then broken rice prices started going through the roof. Then, the company was able to procure rice from FCI at a fixed price but with Govt stopping supply of rice Globus had to buy rice and maize from the market.

Even in such adverse market conditions, Globus was able to increase its quarterly sales from 382 cr in Sept’21 to 567 cr in Sept’23. However, the margins fell from 23 % to 7 %.

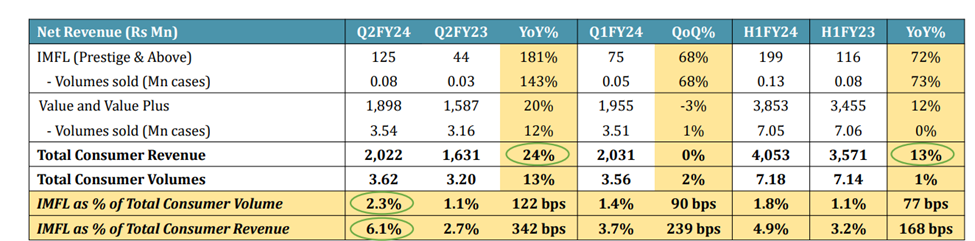

One of the major reasons for the fall in margins is raw material prices. Also, the increased contribution from the bulk segment is another factor. With newer capacities coming in the contribution from the bulk segment has significantly increased. Also, the company started investing in marketing for their prestige and IMFL division.

Demand for ethanol remained strong with prices revised multiple times by the OMCs.

The company sees the IMFL segment to be the growth driver for the company.

Company’s presence

The company has an IMIL presence in Rajasthan, Haryana, West Bengal, and Delhi. Globus dominates the Rajasthan market as far as value and value-plus segments are considered. They were able to further strengthen their market share which is now 35 % of the value segment and 61 % in the value plus segment. The company has plans to foray into one new state in IMIL. However, they have not disclosed which state it is. Doesn’t have plans to move into the IMIL business in Jharkhand and Orissa. Must be UP.

The company has not been able to gain any major market share in West Bengal. The company has blamed the route to market for this.

IMFL revenue is currently 6.1 % of the consumer revenue

They have a presence in Delhi, West Bengal, Haryana, Uttar Pradesh, and Punjab. They entered Uttar Pradesh and Punjab in the last year. Have plans to enter Rajasthan in Q3 and Jharkhand in Q4. I am very positive about the company’s foray into Rajasthan. The company has a very good presence in the state for a very long time. However, the company has mentioned that the distribution and marketing required for IMFL and the value segment are very different.

As per the management, it may take 3 years for the IMFL business to stabilize in a state. Marketing of a brand is not going to be easy.

Debt and other metrics

Debt has increased significantly over the last year with the company increasing its capacity aggressively.

Debt increased significantly to 291 crores in March’ 23 from 180 crores in March’22, which further increased to 352 crores in Sept’23. However, the company mentioned that they reduced the debt by 37 crores in last quarter. It seems that debt repayment is something the company will focus on going forward. The good thing is the cost of debt is close to 4 % which is keeping the interest costs at the levels we see now.

Trade receivables and inventories have also made a huge quantum jump, which could be due to higher contributions from ethanol sales. The effect of this is offset partially by the increase in trade payables. Going forward inventory days may go up as the company informed that they may start stocking up raw materials in the season from next year onwards. The working capital and conversion cycle may get extended due to this.

Capacity Expansion

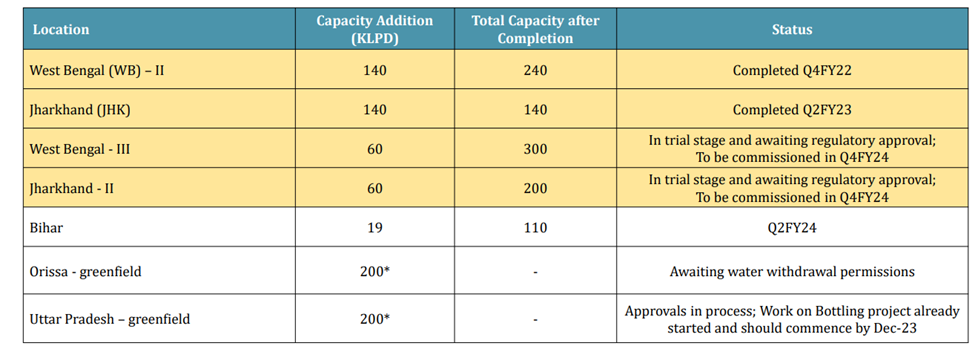

An additional capacity of 120 KLPD will be onstream in Q424. The bottling plant is expected to commence in Dec-23. The bottling plant seemed to be of strategic importance in bringing down the costs of consumer business.

The company expects margins to start increasing from Q424. With the Kharif crop season, the availability of rice may increase bringing some respite to prices. However, as per forecasts, the rice crop is expected to be lesser than last year even though the area under paddy cultivation is slightly higher than what it was last year.

TAAL Enterprise – cheap valueations (05-12-2023)

Post GC years have been difficult for most business. No opinions on the ISMT CEO performance at that time.

Difficult to compare, since they are two different sector companies, ISMT was more commodotized compared to Taal business which is somewhat niche in IT Services.

Taal Enterprises was demerged around 2015 from Taneja Aero, when Salil took over. Taal Tech the main subsidiary (now 100% owned) was run by another person/co-owner, who left 3-4 years back, and since then Salil has been managing it also.

From AGM, my experience is, he does not over commit, never gives futuristic guidance, does listen to suggestions politely without committing. He sounds very boring in a good way. He understands that talking too much might be revealing certain things to competition, so refrains. I think he is doing well at Taal, and some directions taken by company have been inline with suggestions given in AGM. Thanks.