Kiri Industries could be better bet at current level. The last few Qtr results were bad, but coming Qtrs will be much better comparatively.

At current price, looks like there is not much rooms for further downside move.

Posts in category Value Pickr

Sudarshan Chemicals: 3rd largest pigment manufacturer globally (30-09-2023)

Aurobindo Pharma (30-09-2023)

Appreciate if ppl can give a tldr while posting videos mods can delete my post in 24 hrs

Krsnaa Diagnostics – what is the diagnosis? (30-09-2023)

Hi

@SKMohite Karsnaa operates largely on B2G model while others have largely B2C model hence better margins & cash flows.

e.g. Cash conversion cycle of Krsnaa is ~60 days while that of Dr Lal Path Labs is -87 days.

Indiabulls Housing – A compounder from here? (30-09-2023)

is this the 1st time management has discussed induction of strategic partner or this is already known to the market ?

BSE (Bombay Stock Exchange)- Bet on Financialization? (30-09-2023)

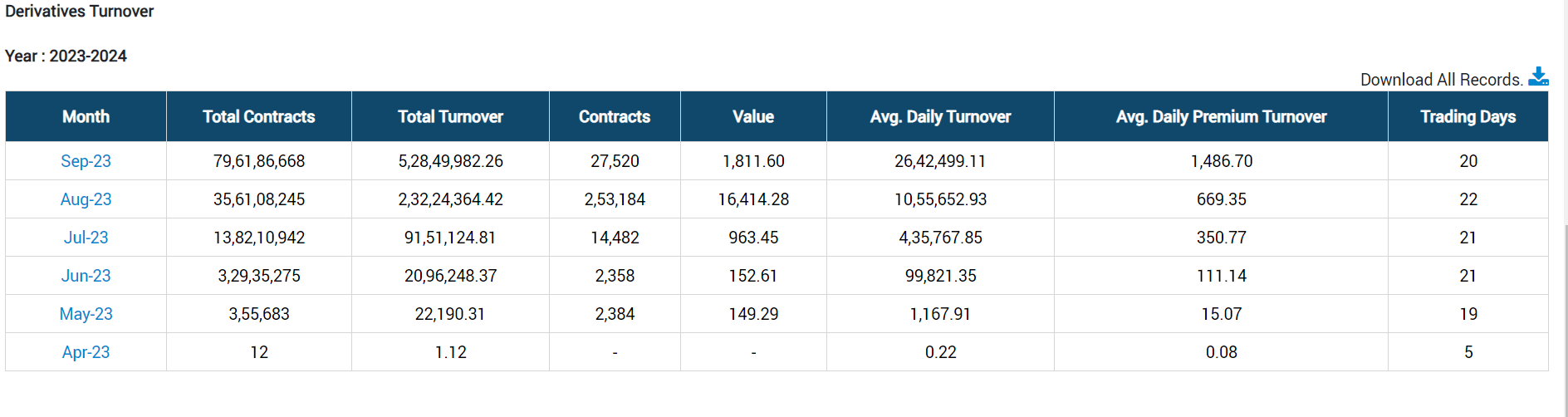

As we end Q2, i think it would be interesting to have a relook at how some of the key verticals has performed during the quarter:

Derivatives: The numbers are roughly doubling month over month. I expect the revenue to be >2.5 Crore based on the existing pricing model of Rs. 500 per premium turnover of 1 Crore.

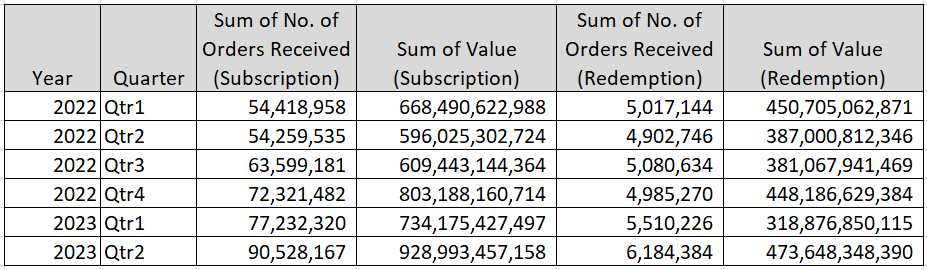

Star Mutual fund update:

The subscription orders have roughly grown by about 17% as compared to Q1 2023 and 66% compared to Q2 2022. Expect the revenue growth to be roughly in line with volume growth.

The IPO market being as robust as it is and significant growth in derivatives and Star Mutual fund, we are most likely going to see the best quarterly results(after removing one offs) since listing.

For the coming quarter we should continue to look out for the growth in Sensex derivatives and see if the Bankex can get any traction post the change in expiry date effective mid October.

It would also be interesting to see the fate of the buy back announced.

Thanks,

AJ

Disclaimer: Remain invested. Have a positive outlook.

Hitesh portfolio (30-09-2023)

Good Day @hitesh2710

Hope you are doing well

Recently most people that I know off : people are just investing by the name so called “ordebook investing”

The kind of rally that was in railway just scares me off that too 4x within a year…

How one should look at sectors like power, railway or construction wherein the major orders for these are government?

Because my past experience in public sector is too bad, how one should look at order book investing and given the fact that elections are close what’s your views on order books backed by government, is there any risk?

Praveg Ltd: Play on Indian Tourism Industry! (30-09-2023)

If we keep the stock manipulation aside, the rest of this is perfectly legal and common. It’s basically a reverse IPO where a private company acquires a public company to list itself. This way, they bypass the scrutiny for IPO listing and can list on the mainboard instead of SME.

Let’s take this company for example. Sword & Shield Pharma Limited was acquired by Praveg Communications Limited in 2019.

They increased their shareholding by a scheme of amalgamation with these terms. “In accordance with the Scheme, upon the Scheme becoming effective and in consideration of amalgamation, Praveg Communications (India) limited shall issue and allot 75 (Seventy Five) fully paid up Equity Shares of Rs.10/- each for every 1 (One) Equity Share of Rs.10/- each fully paid up, to the equity shareholders of Transferor Company i.e. Praveg Communications Limited, whose name appear in the register of members as on the ‘Record Date’ i.e. March 6, 2020.”

They wanted to enter into the real estate and energy business.

“At present, the Company is engaged in the business of Exhibitions and Events Management. The company has various plans for expansion of its business operations from the present level and accordingly, it is proposed to start the business of Real Estate and Energy Business. In order to commence the same, it is proposed to alter the Main objects clause of the Memorandum of Association (MOA).”

They liquidated some of their holdings to buy Jhaveri Credit.They may be starting the real estate or energy business with Jhaveri Credit after acquisition. Since this company is not an acquirer, they have no obligation to report to exchange regarding this.

Jyoti Resins & Adhesives Limited (with bloated reserves) (30-09-2023)

I don’t think the reach or network strength is a problem. It’s actually the execution piece, which is still underway to bring maturity in the states where they are currently present.

To highlight, they have recently entered into new two states (Delhi & UP with five branches), making the state count as 14 from the earlier reported 12. They have been good in tier 3-4 cities (smaller cities as per their IP), and when the states remain similar, the retailers and selling executive count have not grown much, mainly for these smaller cities/town. But if you check the numbers for operating branches (for bigger cities) has grown from 20 to 35 in that period. Even if you take growth from 20 to 30 (reducing the five new branches), this seems to be one of the drivers of topline growth.

Between the June 2021-2023 period, the topline growth & EBITDA Margin expansion, in my view, is a degree of three factors:-

- Increase in companies’ operated branches, resulting in better working cycle metrics

-

Increasing brand awareness and the demand outlook in matured states, mainly – Gujarat (the company claims 30% Market share), Maharastra, MP, Rajasthan, and Karnataka.

-

Favorable crude prices were reducing the RM Cost (which is changing now).

The other thing, that is making me sweat is the Margins (from 15% to 34%). The company said the ideal range should be somewhere between 22-23% which I earlier assumed to be 18%. 3 things that you should be aware of:

- Rising Crude prices are bad for the company’s RM cost.

- Their volume growth may not be reflected in their topline due to the accounting related to their carpenter reward policy. (this also answers the question raised by someone previously and is available in the concall for more details @ 20:30 – https://youtu.be/zbwvNoa4Gus?feature=shared) Once the carpenter starts claiming the rewards (I think in Diwali and the ongoing season) the company will book it both as Revenue and same time in expense) inflating the topline but affecting the EBITDA margins.

- Increasing the maturity and penetration in states or increasing brand awareness in newer states will have positive benefits on the EBITDA. This is also the reason why I think, the company margin profile is a bit superior to the previous range of 15-18% the company used to operate in.

However, at this point, a better judgment would be to expect the margins to revert back to the 20-23% range and some topline growth incoming. The million-dollar question if you’re investing currently… is it already built into the price?

Disc: Fully Invested

Multi-Disciplinary Reading – Book Reviews (30-09-2023)

Exit, Voice & Loyalty, Albert Hirschman, 1970 – When organisations, countries, groups, products, people deteriorate, their citizens, customers, members have an option to either voice their opinion if they want the product / service to be improved or they can exit. What drives people to do either, which ones are most efficient and under what circumstances is what this book is about. To think someone can take so abstract a notion and think so deeply about it is why we need things like sociology and political economy. This treatise is a work of a genius

My Notes –

-

Latitude for deterioration – Human societies create surplus above subsistence that lets them take considerable deterioration in their stride (higher the surplus, higher the latitude for det.)

-

Modern economy keeps despotism/destruction in check – no monarch, tyrant, despot can survive economic deterioration for long (coffee is incompatible with anarchy – Pinilla was driven out from dictatorship in Colombia when coffee prices collapsed) is a popular belief with growth in capitalism. This belief however is mistaken as economic growth has not prevented wars

-

An economy producing a surplus is not at liberty to not produce a surplus or produce less – thus its no different from an economy from a no-surplus or subsistence economy

-

The paradox is that production frontier expands but individual firms are barely getting by at any given point. Man likes surplus but is fearful of paying its price (our inability at understanding “enough” stems from this paradox)

-

Organisational slack – Firms are normally aiming at “satisfactory” rather than a highest possible rate of profits

-

Macroeconomic policies can’t cure microeconomic slack (can make it worse?) – while low rate of savings, high level of prices or insufficient r&d affect the economy, the micros – management, design, salesmanship, labour unions cause considerable slack (low rates for eg. can make this worse)

-

While slack is a bad thing, it also helps during downturn – there’s always ways to cut costs, improve efficiency by going after this slack (as Elon did with X). Slack is continuously generated in an economy. This decay generates its own cure (counterforces)

-

Slack gets cured through Exit or Voice. Exit is economical and Voice political (this is pure elegance in thought!)

-

Exit is felt through a set of statistics while voice through faint grumbling or violent protest. Former is straight-forward while latter roundabout and messy. Economists prefer the “Exit” option (invisible hand)

-

Exit in some domains can be branded as criminal (for desertion), defection and treason

-

Relying on “Exit” as an org – it can go beyond the point of no return where losses weaken the firm so badly that bankruptcy will occur before remedial measures can.

-

A drop in quality of product should never exceed the point of no return. When demand is inelastic, the problem (customers on the edge of “Exit”) may not show up until its too late. (Happens often with countries in downfall – you can’t renounce your citizenship easy). If demand is too elastic, the firm won’t have time to recuperate from a mass exit

-

A mixture of “alert” (who voice/exit) and “inert” customers (who grumble but stay) will provide the firm sufficient time to react (Amazon reviews make voice so dominant that makes every customer an “alert” customer though)

-

Exit could fail to cause revenue loss if firm kept gaining new customers as it lost old (hence SaaS firms monitor churn – though few do much to listen to the whys of the churn)

-

When uniform quality decline hits a industry, customers churn throughout and decline sets into the industry as a whole (mergers/monopoly might be preferred here)

-

Voice is the only option when exit is unavailable (family, state, church)

-

Voice is a more commanding option in less developed countries where options are less (Silent-exit is preferred when options are aplenty, as in developed economies)

-

What keeps a customer inert could be switching costs (rational) or loyalty (less rational)

-

Effort to voice would be proportional to the advantage to gained multiplied by the probability to influence a favourable outcome

-

Inexpensive, nondurable good vs Expensive durable good (automobile) can also influence voicing

-

Exit is either/or but voice is an art, constantly evolving in new directions. Presence of an exit usually atrophies the art of voice (classic eg. is brain drain)

-

State monopolies like alternatives so they don’t have to address glaring inefficiencies. A deterioration in rail service is not a serious matter if other long distance transportation like trucks exist. They are also insensitive to customers switching long as they have the backing of the national treasury (our PSUs have lived by the same logic)

-

If you dont like the management you should sell the stock results in perpetuating bad management and their bad policies

-

Customers who drop out first as price increases aren’t the same as the ones who exit as quality drops. Differences in quality inflicts very different losses to diff customers (even if quality can be expressed in price terms)

-

Easy exile in Latin American countries promoted Exit of political opponents to neighboring countries (it was in fact preferred). Japan offered no such option being an island and there was always compromise worked out through Voice

-

Those who have nowhere else to go are not powerless but influential – in a two-party system centrist views might isolate the hard-right or hard-left causing defection or sitting out

-

Loyalty makes exit less likely and might activate Voice. It is however just a barrier with a finite cost, like protective tariffs

-

Effectiveness of Voice is strengthened by the possibility of Exit, though willingness to use it also reduced by Exit

-

Boycott – on the border between Voice and Exit is the “threat” to Exit with a promise of re-entry (points of exit and entry will be far from identical though)

-

High fees for entry and stiff penalties for exit increase loyalty (cults work this way!). Loyalty leads to self-deception (severe the initiation, higher the self-deception – why weddings have so many rituals)

-

Penalties of excommunication, defamation or deprivation of livelihood keep Exits in check

-

Exit from public goods and some orgs/services may cause further deterioration (as is happening with Vi / Vodafone and in public schools in the US)

-

Some loyalists may prefer not to leave so as to not leave the org / country in a worser shape – worse it gets, the harder it is to leave (”right or wrong, my country” can become “the wrong-er the my-er”)

-

Domestication of dissenters is achieved by assigning the role of “official dissenter”. With the label, his official position becomes explicit and predictable and hence “powerless” (phenomenal insight)

-

Orgs that treat Exit as treason and Voice as mutiny are unlikely to be viable in the long run

I found in this book a useful way to think abstractly about several different situations that apply to countries, companies, societies and its orgs. Economics emphasizes exits as with Adam Smith’s invisible hand but its not as straight-forward in a lot of situations where Voice would have been preferred. We pay so little attention to Voice and it could be to our detriment if that option doesn’t exist or if it isn’t used. In a zoomed out view it is not hard to see why cryptocurrencies rose up and why current geopolitics is leading to long-term de-dollarization for eg. – without the threat of exit, there’s nothing that can improve fed and the US govt’s behavior (song and dance over debt ceilings and govt. shutdowns). Once you start applying Voice/Exit, you will see it everywhere. 11/10