I was outfoxed in anticipating the combined BV, which is now published officially in the latest presentation – Link. However, even the big fish like Nomura seems to be in a similar situation:

Disc: Hold position in family account.

I was outfoxed in anticipating the combined BV, which is now published officially in the latest presentation – Link. However, even the big fish like Nomura seems to be in a similar situation:

Disc: Hold position in family account.

#PHIL FISHER 10 DON’T

#PHIL FISHER’S 15 QUESTION

1)Does the company have product or service with sufficient market potential to make possible a sizeable increase in sales for at least several years ?

2)Does the management have a determination to continue to develop product or process that will still further increase total sales potential when the growth potential of currently attractive product lines have largely been exploited ?

3)how effective are the company R&D Efforts in relation to its size ?

4)Does the company company have an above avg sales organisation?

5)Does the company have. A worthwhile profit margin?

6)Does the company doing to maintain or profit margin?

7) Does the company have outstanding personal & labour relations?

8)Does the company have outstanding executive relationship?

9)Does the company have depth to its management?

10)How good are the company cost analysis & accounting controls ?

11) Are there are other aspects of the business, somewhat peculiar to the industry involved , which will give the investor important clues as to how outstanding the company may be in relation to its competition?

12) Does the company have a short range or long range outlook in regards to profits

13)In the foreseeable future will the growth of the company requires sufficient equity financing so that large numbers of shares then outstanding will largely cancel the existing stockholders benefits from the anticipated growth?

14) Does the management telk freely to investor about its affairs when things are going well but ” clam up ” when trouble & disappointment occurred?

15)Does the company have a management of unquestionable integrity ?

Hi

I think the cost of capital here is high as the pedigree, loan book quality and brand comes into play. Plz correct me if that’s not the case.

Also India bulls lending profile is risky as it lends at quite higher rates ( since the coc is so high). So the asset quality should always be on a watch and I assume that here npa would always be elevated as compared to similar business.

Now this story can be broken in two parts. First will culminate with the change of name soon and second will start when reliable growth numbers with decent asset quality will start pouring in. Going back to BV will depend on the second part imo. Let’s wait and watch and also hope the sticky inflation doesn’t make cost of borrowing go higher and difficult for the nbfc group.

Best

Divyansh

Disc : invested

Made multiple entry/exits so cost of holding is lower

quite confused should I book profit now. Invested at elevated level. Nearly 40 percent gain made. felling like double edge sword , if i book the profit will the long term opportunity will be missed.what is ur opinion in this type of situation?

There are two major risks in too small a stock

This under 400cr stock overcomes the first with LMW. A famous and old empire in Coimbatore which shares common management with LAKSELEC ( Lynch said the worse the ticker name, the better chances of people not discovering until it is already an obvious buy:)). LMW’s textile mills drives 80% of revenue for this company which supplies textile machinery.

Second risk is the inevitable risk we bear to invest in cos >1000cr. But also can be the reason why it is locked in circuit (upper or lower).

Why I’m studying this company?

Under 20 PE for a stock that has shown extraordinary growth with more promise in the future.

Company’s textile business is a consistent cash cow (set customers, textile businesses are on multi-year up-cycle). Company is foraying into exciting spaces like smart meters and EV chargers.

Will share research here soon. @Malhar_Manek invite you to start us off here.

Please include me into the Zoom invite. I would like to enhance my knowledge into stock market and chart analysis.

Please let us know the date and time in advance so that we can plan accordingly.thanks

My take as below:

Dont know impact on Book Value but I feel that conversion would be best for company as it will free up the capital for growth. Stock already at significant discount to BV so equity dilution would make base for higher levels with additional capital.

Debt raising is based on their AA rating and rates can only improve when their AUM increases with less NPA giving more stable future earnings. I feel Gagan and team has brought the company from difficult situation and things are only bound to improve from hereon. Change in perception by market is evident and if overall sentiment remains stable, IBH should cover its gap from BV.

This would mean a really large capex. It may though take a long time.

Disclosure: I have some investment.

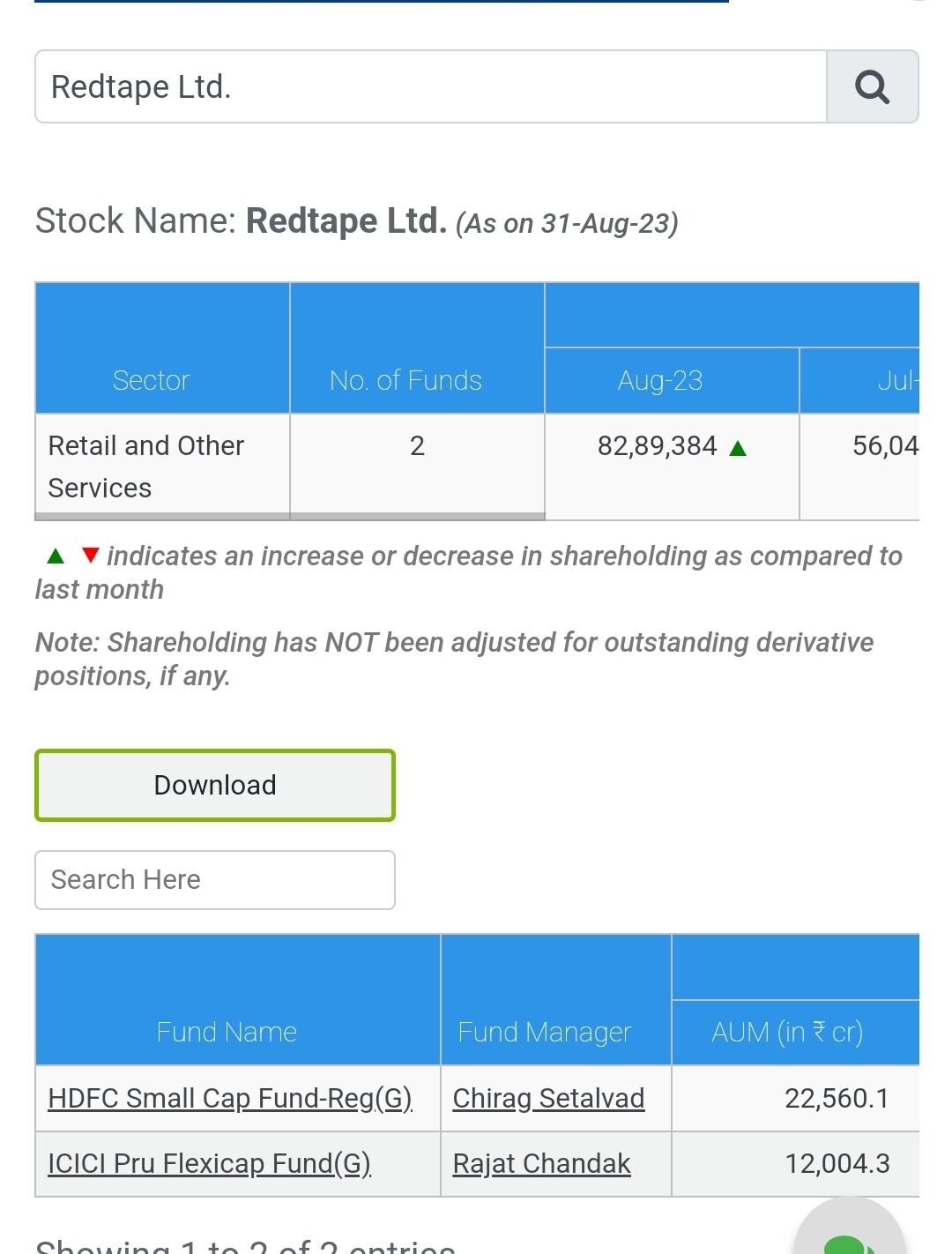

Icici flexicap added close to 26 lakh redtape shares last month