Posts in category Value Pickr

Is Buy and Forget a Myth? (14-09-2023)

There was even a study conducted where people who switch from company to company to miss out on opportunity cost eventually end up making less CAGR compared to holding on to the same winning formula.

“Polyplex Corporation “ Are Good Days Ahead? (14-09-2023)

Did anyone attend the AGM today? Highlights ?

The Co. does not post Audio Transcripts of its AGMs and hence they are not available on Co website.

Hitesh portfolio (14-09-2023)

Selling is always a tricky issue. Not any specific book on how and when to sell stocks. We can learn from our own mistakes. And keep observing stocks that have made major tops and reversed and see how things have changed for the company at that period of time. Read comments on VP thread on that particular company, particularly at the time of the stock price topping out. Often it provides important learnings.

An important aspect to selling is to know which kind of company you are holding.

If it is a high growth stock, then it might make sense to keep holding on, even in the face of a strong run up. If these correct at all, these will go for some sideways consolidation before resuming their upmoves again. You can see a lot of such examples in current markets. Most of the times these kind of stocks do not fall more than 20-25% from their latest tops.

If you are holding a flavour of the season kind of stock, then it makes sense to exit when there is a lot of extrapolation related to its future prospects. We have seen these things happen in the past in chemicals, pharma, etc. Defence, railways etc sectors seem to have heated up a lot and there are a lot of expectations related to their growth built only on their order books. The party still seems to be on and could last much beyond anyone’s expectations , but I feel that sector needs watching for any signs of topping out.

Technically it is a bit easy to figure out short term and major tops. Short term tops are often seen by smallish double top patterns after sharp run ups. Or at times, a doji candlestick after a breathtaking rally. Or other bearish candlesticks. Or a gap down fall with huge volumes.

If someone wants to sell on the way up , then one can use RSI over bought indication on weekly and monthly charts to start lightening up positions. Usually when weekly or monthly rsi tends to go beyond 90, or if there is some divergence in RSI and price, it’s often a signal for trimming positions and then gradually plan total exits. In many instances, definitive breach of the 10 week moving average in stocks which have rallied hard and correct gives early indication of a top.

If someone is a long term investor holding consistent compounders like HUL, Pidilite, PI Inds, Nestle, HDFC Bank, Kotak bank etc, then there is no urgency to sell. There idea should be buy when there is big correction and then sit back.

Praj Industries (14-09-2023)

Apart from EBP program, this Global Biofuel alliance will enable Praj to do more international projects, which have higher margins than domestic projects. Also, i feel after ethanol, next big thing is SAF and CBG.

SWELECT ENERGY SYSTEMS LTD – some information from Annual report (14-09-2023)

Hi, Thanks for this thread!! I am interested in this company since it is starting it’s new Module PV plant which is much higher than the closed one.

Since you have done a bit of work on this company and also gone through the AGM Video, can you just on the back of the paper estimate the Capacity Utilization Levels from this new plant? And what could be the potential revenue coming out of this plant for FY24?

Also, with all segments the company has viz. Casting, EPC, IPP, and this new manufacturing, how much do you think the revenue will flow in for FY24 and a rough-margin range? I am asking this because if there is some good uptick in Profit then valuation might look cheaper and encourage us to put more time into evaluating further in detail.

Regards,

Mukul Jain

Sona Comstar BLW – Direct EV Play (14-09-2023)

On the Question of estimation of orderbook : Generally during the RFI/RFQ phase the lifetime quantity is discussed. From my experience of working at a TIER-1 , we used to ask the OEMs for the Quantity over the lifetime.

If the Quantity was less ( in our case < 100000), we would usually ask them to take off the shelf product (if that was a part of the offering) Additional costs were put against Software modification , hardware configuration etc.

If the Quantity goes above 1 million, the price would get negotiated and we would aggressively bid for the project. The contract also had compensation terms in case the quantity was not fulfilled. Sometimes we would track this on an annual basis.

The development cycle of a 4 W EV is approximately 3-4 years ( and it is getting shorter ) RFI /RFQ are sent within 6 months and suppliers are finalised within 1.5 years.

Power grid – a superior alternative to Invits (14-09-2023)

This is the reason why PGinvit is stinking and has fallen from 140 plus to 106…if there is no addition of new project, eventually maintenance costs will eat cash flow and you can keep dipping into reserves so much, so as to keep paying the DPU. Market is expecting DPU to fall in this invit…and even the venerable Indigrid is not in its usual form these days but in much better shape than PGinvit…all my 2 cents…take it with a pinch of salt

Gokaldas exports — cup and handle/rising channel (14-09-2023)

Given the specific situation (as detailed above),

I would discuss the relevant factors i.e. numbers to get to the Valuation.

And happy to hear contra opinions here.

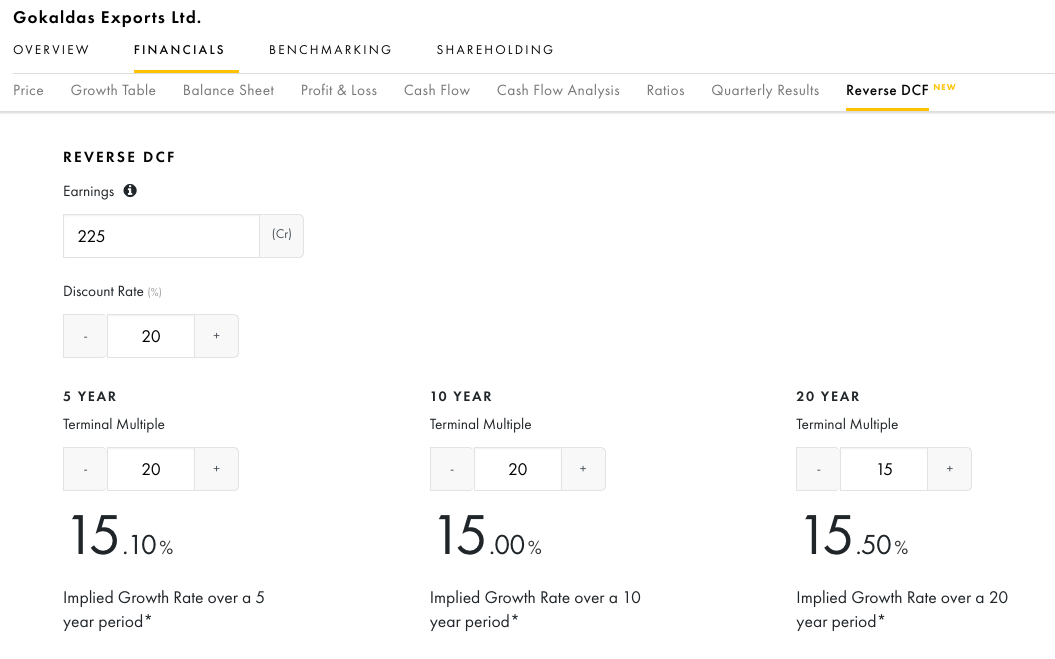

@wiseunwise shared the approach of Reverse DCF above.

It looks like a good way to look at Valuations.

I’m assigning the numbers that look rational to me.

-

Earnings

Atraco’s current earnings are 30% & 35% of Gokex’s revenue & profit’s resp

Adding a conservative 30% to last yr’s Profits of 173Crs, comes to 225Crs.

Let’s take 2 scenario’s of discount rates 15 & 20% (reasonably high benchmarks)

-

No of Yrs & Terminal Multiples go hand in hand

A. No of Yrs

Once the FTA’s are in place, the growth should sustain for a long time.

Let’s take the 5/10/20 yrs as scenario’s

B. The Terminal multiple – the average P/E from last 3 yrs, is around 20.

The way Gokex has progressed, by now, it looks like a formidable player.

So P/E of 20 looks like a conservative benchmark.

I’m assigning terminal P/E of 20 on a 5/10 yr period & 15 on 20 yr period

We get a Implied growth rate of 10/ 15% depending on the Discount rate.

The Management has guided for 20% growth rate for long term

(The MD, Siva Ganapathi ji looks conservative in his approach & quite credible, so far)

Onto the FTA, the Textile minister, and Geopolitical context.

The closure of FTA has been widely speculated since a while now.

I have been following Piyush Goyal ji’s mentions on newspapers since a while now, and surely there’s prominence to FTAs.

Also, G20 seems to have gone well, and further consolidates Inda’s position globally.

And daily we are looking at corporates validating India’s manufacturing Renaissance.

So India’s Textile manufacturing growth looks quite assured.

Given all of the above, I’m quite comfortable with the company’s current Valuation.

Disclaimer: Invested & Biased. Imho, the discussion’s primary focus is Valuation.

And in that regard, would humbly request to kindly highlight any apparent mistakes/ flaws in the approach/ thinking to avoid going wrong on a high conviction bet.

Delta Corp – A huge but risky opportunity (14-09-2023)

i agree with you . but frankly speaking these terms like Gross gaming revenue (GGR ) etc are too complex term for me . and dont understand too well

but one thing i am sure about this that Govt is also one of biggest partner in any buisness in india . if it feels that they are loosing tax revenue to other countries like macau or nepal , definately they will reverse or modify there decision .

i have seen this in buisness of ciggrette when they felt that organised market is loosing market share to unorganised market they stopped increasing tax

same is import duty on Gold , when they became aware that high import duty leading to smuggling they reduced import duty

my point here is that major money is made in extreme passimisim and when there is no way out and when everyone start calling buisness as its end .

just see what people are taking about PVR just few months back that it will be doomed due to OTT , if anyone made investment there could have easily made around 30 percent from there .