Carysil, due to their SAP implementation?

Posts in category Value Pickr

Priyank’s Portfolio (31-08-2023)

Notes on chemical sector:

- Fluoroploymers industry will likely see consolidation over next few years.

- There are only 5 naturally occurring compounds that contain C-F bond. Hence, the body does not know how to handle them, making C-F carrying drugs easier to kill cancer cells, viruses, bacteria etc.

- Navin Fluorine International does CDMO in pharma – no other Indian listed entity is into this space.

- Tesla sources batteries from Panasonic and brands them as Tesla

Source: Prabhudas Lilladher

Archean Chemical – Specialty Chemical Leader (31-08-2023)

@Aditya_Bajoria : Thank you for cross checking the IPO document, which i could have missed.

-

They are paying money but in last 5 years lease didn’t extend. As you know all industrial salt, Bromine everything comes from this one location. They can clearly write that.

-

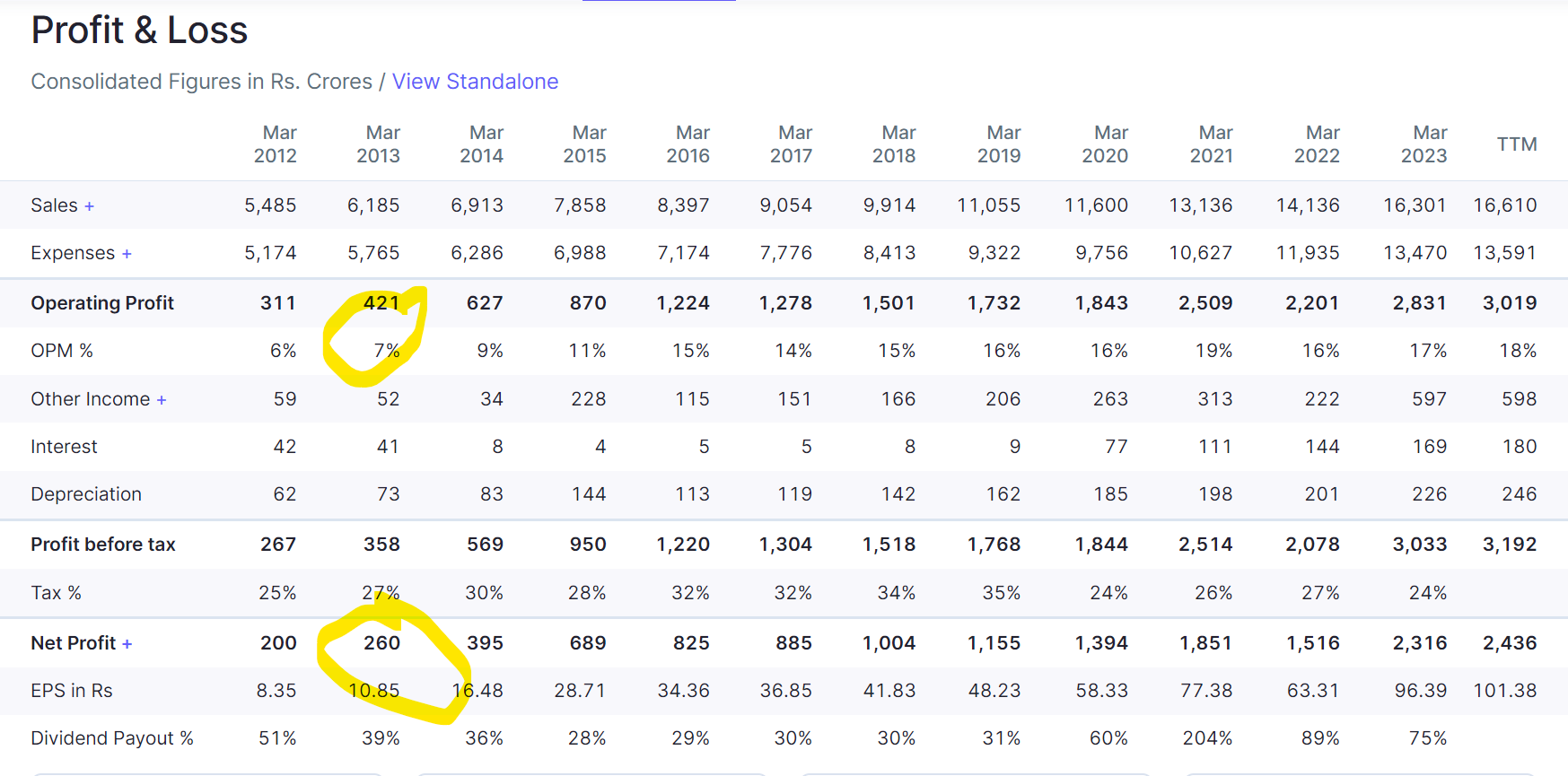

Lets consider this case of taking 2-3% in revenue as commission, if you go through RHP you will see that in the last 5 years (2018-22) . They have 2 bad years where they are negative profits and excessive rains erased all their margins on both the years. 2022 is where ACL had good profits and also inventory turnover. They raised cash at their peak year at 27~28PE to 2022 profits which is their peak year probably. After IPO proceeds they retired debt and all interest costs came to bottom line.

To think through what i surfaced, promoters just raised money from people at a very good valuation(check interest rates they are paying on their previous loans and valuations at which they diluted equity). ACL made good money through IPO and even before first year got completed Promoter had his eyes money.

- IPO proceeds are 1462 crores according to RHP.(Page 78) (657Cr to Promoters and 802 Cr new issue).

Lets look at their net cash rough estimate

ipo proceeds 807 cr

Net Profit is 384 cr (not adjusted for recievables)

underwriting expense -40 cr

total 1151 Cr

retirement in debt 828 cr

so total remaining is 323 crores(1151 – 828)

how much did the balance sheet swell by (1756-1532Cr) = 224 Crores.

we now see a differential of ~100 crores.

Lets look at Cash flow statement (FY2023 – FY2022).

- Inventories changed by -37 crores

- Trade receivables changed by 120 crores

- Trade payables changed by 20 crores

- Other liabilities changed by 70 crores

Balance sheet

- Inventories changed by 47 crores

- Trade receivables changed by -40 crores

I was unable to understand how did the numbers differ here between balance sheet and cashflow.

I was probably wrong in using the number 250 Cr, it could be lesser or i could be wrong with my assumption. The numbers didn’t tally for me, so i gave it a pass.

i wasted almost 1.5 month on this, If you could point out what is wrong in my calculation i will change my mind as well, because you rarely get 10x inventory turnover and 40% opm hand in hand.

Edit: Provisions of 8.5 crores were not included in cost…

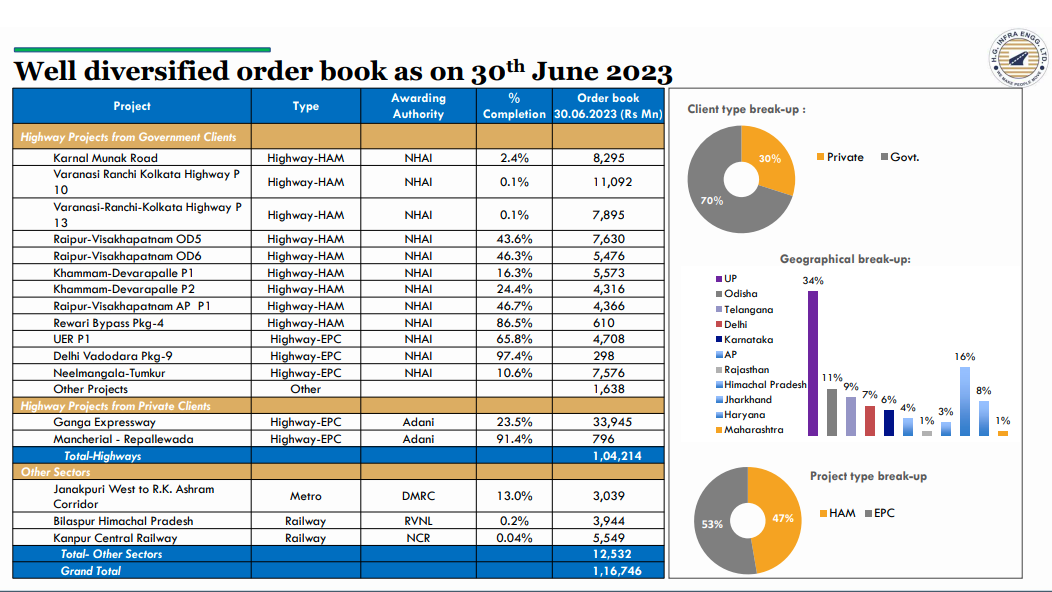

H.G. Infra Engineering Ltd : Paving the Path to Success (31-08-2023)

My notes of 1st August 2023 concall

- Revenue Guidance:

- Revenue for the year is maintained between INR 5,500 crores and INR 5,600 crores.

- Margins are expected to be around 16%.

- Order inflow guidance is revised to INR 7,000 crores to INR 8,000 crores due to project award delays

- Approximately INR 2,000 crores are expected from sectors other than highways, such as railways and metros.and a reduced order guidance.

- The goal of achieving INR 10,000 crores revenue over the next 3 years.

- Revenue Breakdown:

- Ganga Expressway project contributed around INR 475 crores in Q1 FY ’24.

- Existing HAM projects contributed approximately INR 500 crores in the same period.

- Clear focus on contributions from the Ganga Expressway project, SPVs, and NHAI EPC projects.

- Revenue Composition for Future:

- Projected contributions from HAM projects and non-road sector projects remain largely the same.

- Monetized Asset Approvals and Inflow:

- Approvals for the monetized assets with KKR are in progress.

- Two projects with CODs are already with the finance department for in-principle approval, with the third project expected to follow soon.

- The finance department typically takes around 7 to 10 days for in-principle approval.

- Despite a recent delay due to NHAI organizational changes, the inflow is expected by October or November.

- Project Pipeline and Awards:

- The company aims to achieve around INR 4,000 crores to INR 5,000 crores of project awards from NHAI.

- Awards from MSRDC and other sectors will contribute to the remaining projects.

- Specific mention of participation in the Pune Ring Road tender and expectations of award by October or November.

- Railway Opportunities and Capabilities:

- The company is actively participating in railway projects, including permanent track linking works.

- Opportunities are seen in Maharashtra, Gujarat, and Uttar Pradesh.

- Collaborative ventures and MOUs are being explored for railway projects.

- Railway station redevelopment projects are also considered for bidding and participation.

- Equity Requirements and Bid Pipeline Overview:

- Equity requirement for next 3 years: FY ’24 – INR 407.4 crores, FY ’25 – INR 268 crores, FY ’26 – INR 158 crores.

- Bid pipeline: Strong pipeline for MSRDC projects (INR 30,000+ crores qualified), NHAI projects (INR 45,000+ crores active), railways, and metro.

- Working Capital:

- Working capital increased temporarily due to delayed payments from SPVs and clients, but expected to return to usual levels.

- Asset Monetization and Debt Reduction:

- Expected reduction in debt by INR 200-odd crores by year-end.

- New capex may add INR 60-70 crores to debt during the year.

- Projected debt range: INR 425 crores to INR 450 crores by year-end (excluding asset monetization).

- Order Inflow Guidance and Bid Pipeline

- The company aims for INR 7,000-8,000 crores order inflow this fiscal year.

- Limited order inflow received in H1 with challenging Q4 ahead.

- Around INR 5,500 crores outstanding bids expected to open soon.

- Estimated INR 1,000-2,000 crores potential from ongoing bids.

- Bid pipeline includes INR 1,50,000 crores projects.

- Targeting to bid for INR 90,000 crores projects.

- Historical bid strike ratio of 7-8% gives confidence in achieving target.

- Bids to be completed in Q2-Q4 for substantial future opportunities.

- Operational Efficiency and Equipment Utilization:

- The company has strategically invested in construction equipment, contributing to operational efficiency and margin improvement.

- The new equipment has led to reduced dependence on external vendors, translating into better control over operational costs.

- The equipment utilization rate has been decent, and the benefits of internal strategic investments are being realized.

- Margin Expectations and Revenue Breakup

- The company has guided for 20% to 25% revenue contribution from the non-road sector in the annual report.

- There is a cautious approach in bidding for projects outside the highway sector, with a gradual expansion plan over three years.

- The aim is to be selective and avoid desperate bidding, which is intended to help maintain similar margins.

- There is confidence that maintaining margins will not be a significant challenge even as the non-road order book increases.

- Competition Intensity and Project Mix

- The competitive landscape in the industry has seen a correction in recent months, with a decrease in the number of bidders for projects.

- The number of bidders in EPC projects is still high, ranging from 35 to 40, while in HAM projects, it’s around 7 to 8.

- There is a cautious approach to bidding, with an emphasis on avoiding margin shrinkage and compromising on profitability.

- Despite the competitive environment, there is confidence that the company can target the goal of adding around INR 5,000 crores worth of highway projects without compromising on margins.

- The target for road inflow is expected to be a mix of around INR 2,000 crores from EPC projects and the remaining from HAM projects.

Project statuses:

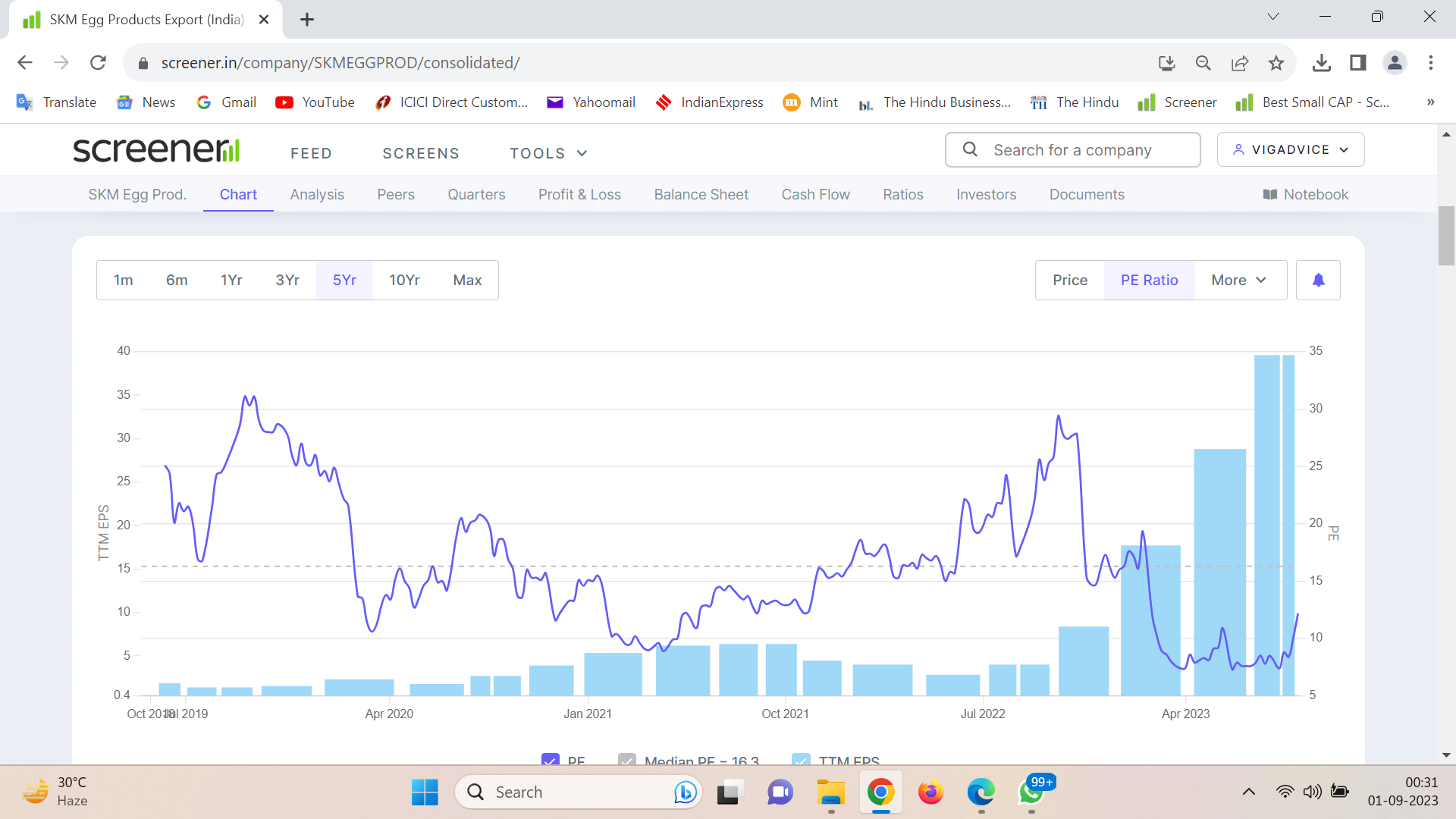

SKM Egg Products – thinking out of the shell (31-08-2023)

Remarkable decline in its PE. One year back it was more than 25. It has more than halved.

EPS has multiplied from 3.98 to more than 39 during this period. Any surprise its price has climbed about 5 times during this period.

Disclaimer: Have a small holding.

IDFC First Bank Limited (31-08-2023)

Hello community. I am confused about this whole MSCI rejig and its impact. As we all know, futures are trading at deep discount since last many days. I thought that this is happening due to MSCI rejig. But today was something extraordinary – Sep/Oct futures trading at almost INR 6 discount. I am not able to understand the reason. Is it like some institutions are short selling in futures? As I understand, MSCI inclusion should bring in $210M in this stock, so price should go up. Then why people are short-selling it?

Another puzzle is today’s 11.5 Cr selling by “BNP Paribas Arbitrage”. By name, it sounds like an arbitrage fund, trying to benefit from this MSCI story by shorting this stock. Again the same question – why would someone short, if there is clearly an increased fund flow in to the stock (and hence more demand for shares).

Please help. Thanks in advance.

Capacit’e Infraprojects (31-08-2023)

Yes, they are increasing the authorised capital. This needs to be done first before they can issue further shares. At this point (where auth. capital is being increased) no shares will be issued. It is a procedural thing.

BSE (Bombay Stock Exchange)- Bet on Financialization? (31-08-2023)

The opportunity in BSE.

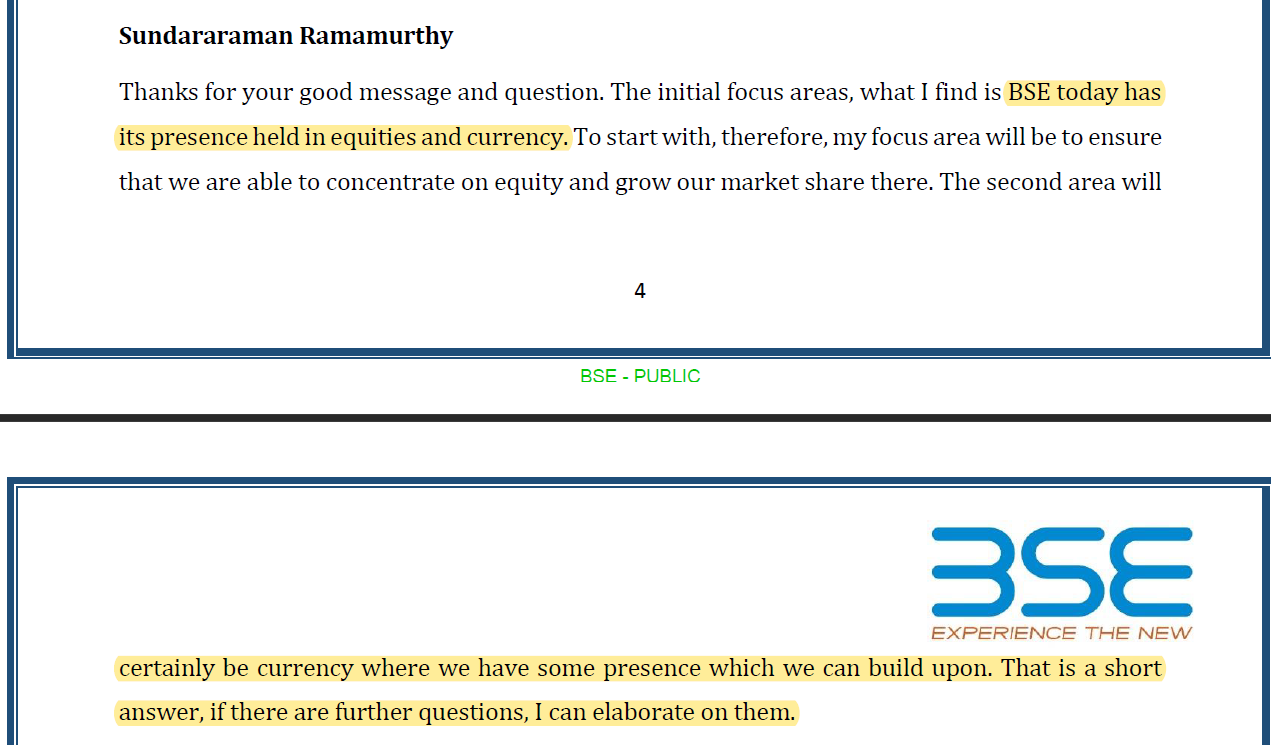

BSE is a special situation (Management change). Mr. Sundararaman Ramamurthy joined BSE on 4th Jan’23 and by 7th Feb, he started the first ever post Q3 result concall and handed most of it single handedly. He is an old seasoned hand at exchange business, having served 20 years in senior leadership role at NSE. Could his entry be similar to the Varun Berry episode for Britannia ? Let’s explore the possibilities !

Varun Berry joined Britannia in Feb 2013 as vice president & COO and was appointed as MD in April 2014. The rest, as they say is history.

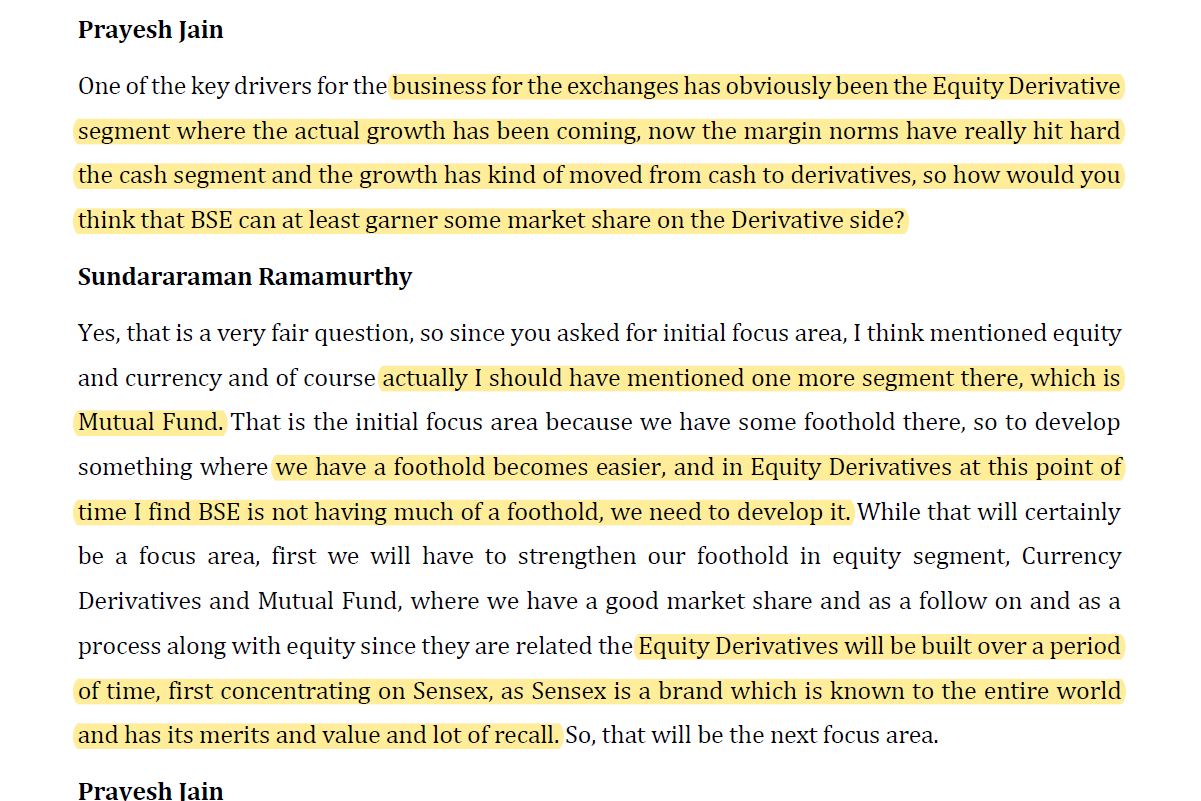

BSE has been losing market share in cash segment since years and held just 7% share at end of last year. It’s derivatives segment was a non-starter and never took off. It’s major saving grace or growth engine was it’s star-MF platform which held 50% market share. Trouble is, derivatives are the mainstay of income for exchange business and there was no mgmt. focus on this segment till that point. Even in the first call, when Mr. Sundar was asked for his 3-4 top priority, derivatives was not in the list and it seemed like an after thought as he referred to it later in the call.

However, one thing came clearly even in that very first call, the power that be, don’t want India to be a single exchange country. 2 thriving exchanges is in best national interest

This point has been reiterated by Mr. Sundar as well as SEBI Chairman on different forums (as shared other posts in this thread).

Both of them also referred to multiple steps that will be taken during the course of time to improve the situation for BSE. Let’s explore the steps taken so far and what might be already cooking in the background.

Step No. 1

By the time of Q4’23 call Mr. Sundar had got his priorities refined. Not only equity derivatives featured in his top 3 list, but he had already re-launched a revamped derivatives segment having done all the background work on this in the last quarter.

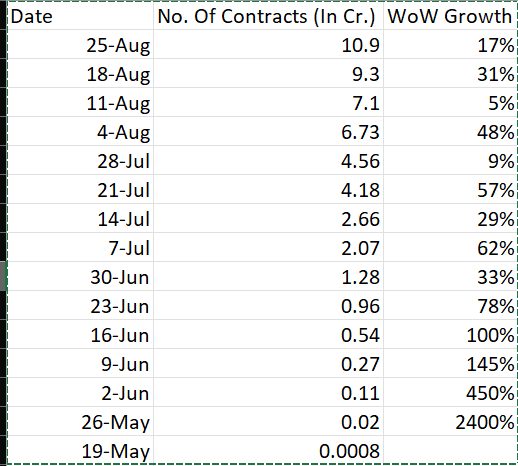

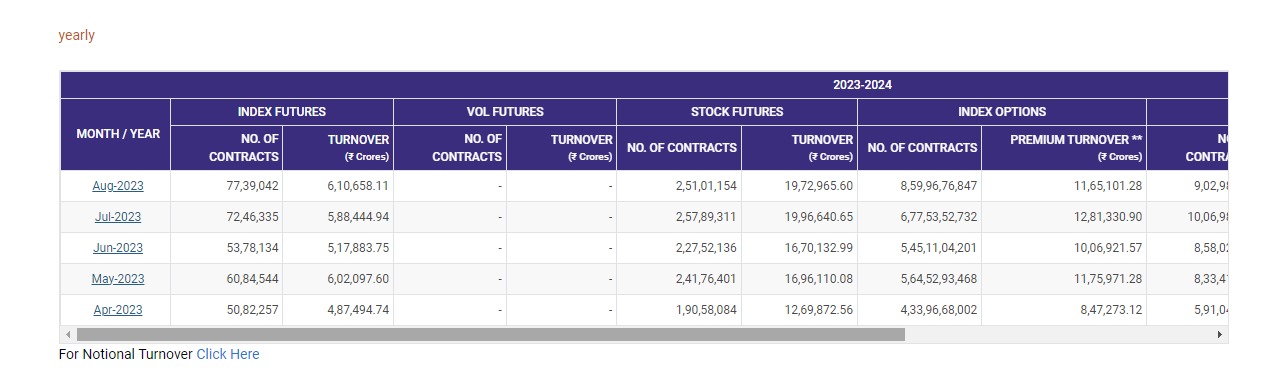

To his credit, it’s been showing result and how ? Just in 3.5 months since launch, BSE has done volumes which are 3.5% of NSE’s volume. That’s remarkable, specially, given how they are doing in cash segment.

Last column stands for Week On Week growth.

HDFC Sec report estimates that by FY24 end BSE could reach 10% market share. i,e, ~3x current volume in next 7 months. Even today, not all major brokers have enabled the BSE derivatives trading. There is backend work that is required to be done by software vendor and then brokers to enable the processes for the derivatives trading. For example, Kotak just started last week https://twitter.com/kotaksecurities/status/1695000451534696596?s=20

and then there is the most important part, where participants want to see the volume before they join the bandwagon. Then at some point the network effect takes over I guess and it’s more a hard sell. Given all this background i think the results so far are nothing short of outstanding. Management deserves kudos for it.

In Q1’24 call, BSE said that they did a revenue of about 26 lacs for the week of 4th Aug in which they did 6.73 cr. contracts. This is while they are charging 1/7th the price of NSE (as per HDFC Sec report). NSE gets nearly 10,000 cr. revenue from this derivatives segment, with option derivatives accounting for nearly 99% of the derivatives volume.

So one can imagine the possibilities.

Step 2:

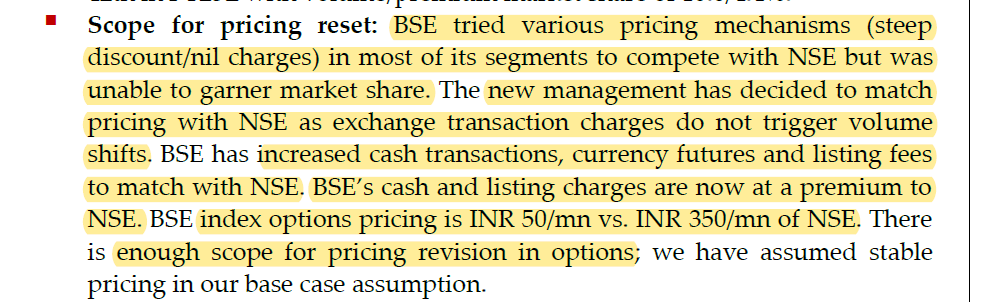

There is a new found aggression on the pricing front. BSE no longer wants to be the poor cousin of NSE and charge less for everything.

Example ? This is from HDFC Sec report.

Also, see this,

In fact I got this clarified in the Q1 call, and this was the response. They have about 70k AP’s on their system and this straight away adds about ~15% of current bottom line. IMHO there isn’t any commensurate additional expenses for this. It’s just a toll which both exchanges decided to extract and the AP’s are just price takers. Some of them drop off, but others will swallow it as cost of doing business.

So at some point that will charge appropriately for the derivatives too

Step 3:

Having tasted success with this Sensex options, now the aggression is visible even in bankex

Best part, the mgmt. suddenly seem to be listening to participants voice and doing changes as a market player should do.

What could be future steps ?

Step 4

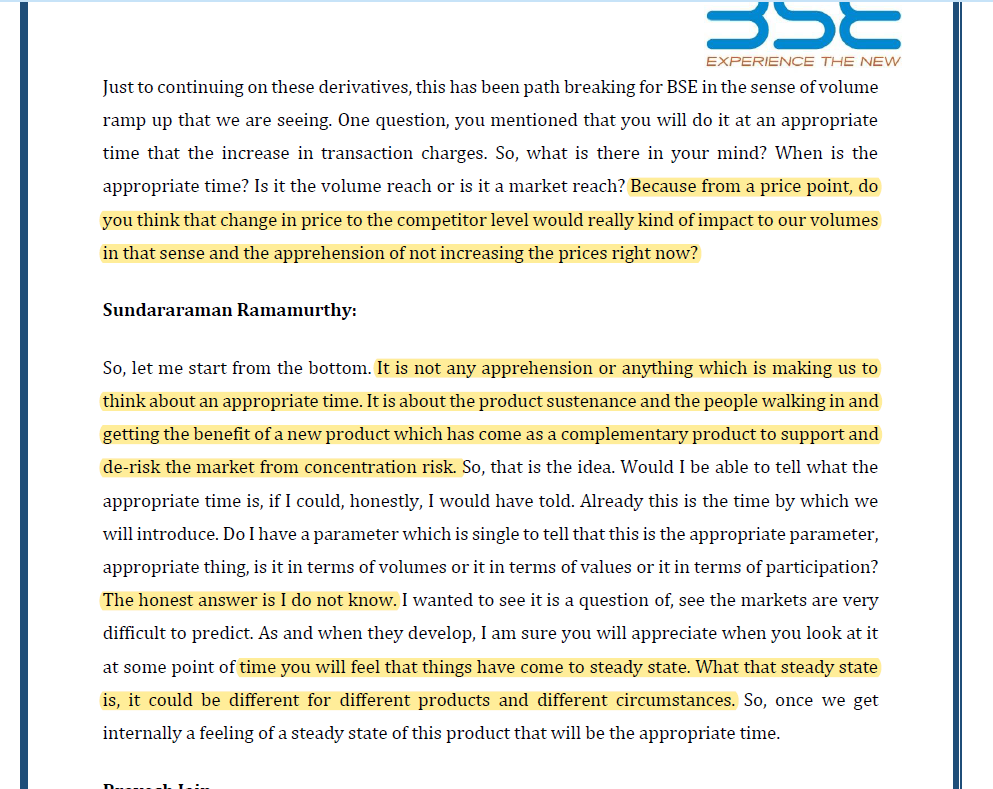

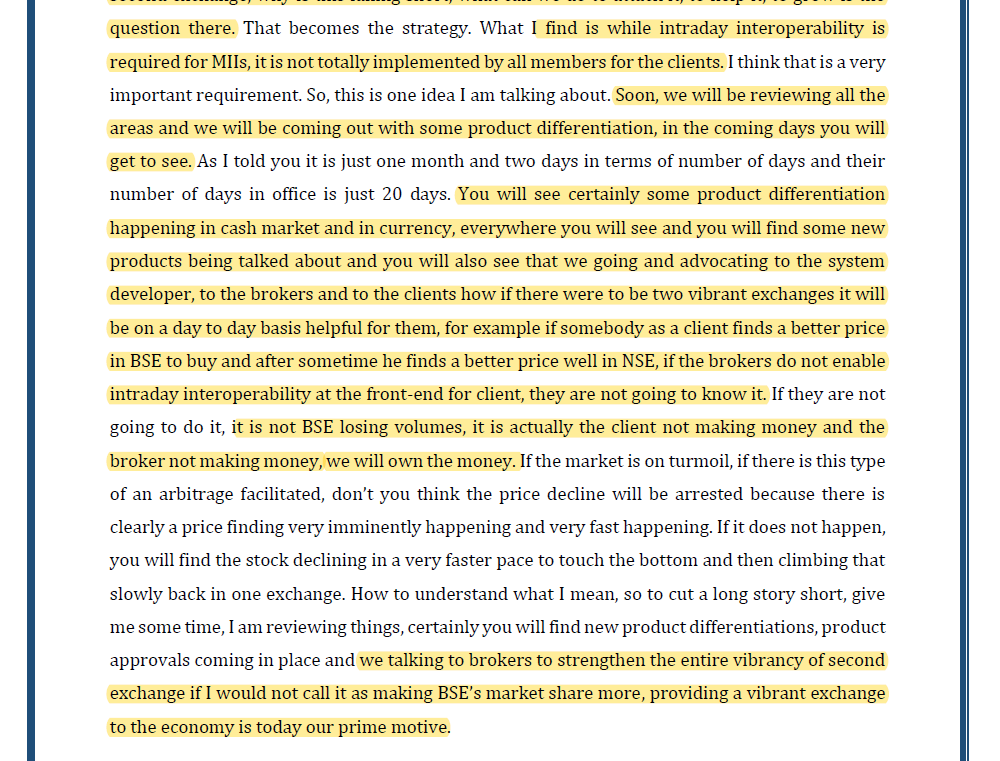

He has been batting for intraday interoperability for sometime now. My understanding is this could give a boost to volumes in cash segment for BSE.

All this for a price of ~14k cr Mcap. Of course they also hold nearly 15% of CDSL which is valued at ~12k cr. Mcap and some cash on books. NSE did an EBITDA of 10,426 cr. for a revenue of 12,765 cr. in FY23. The derivatives volumes in FY24 are just going through the roof for NSE too. nearly doubled since beginning of the year.

Step 5

Focus on SME listing ?

Disc: Invested from 550 levels and have added more along the way .

Archean Chemical – Specialty Chemical Leader (31-08-2023)

My understanding on 3 questions raised:-

-

The Company entered into Memorandum of Undertaking (MOU) dated August 10,2010, with Government of Gujarat (GOG) for the Land lease which expired on July 31, 2018 and the Company had made an application for renewal on December 28, 2017. As per the MOU with GOG, the lease term can be further extended for a duration and conditions as mutually agreed at that time. There is also a GOG circular no 1597/1372/ dated October 9, 2017 which states that such leases can be extended for a period of thirty years. The company has also been receiving demand note annually for the revised lease rents as per GoG circular and the company has been meeting this payment.

Management made an assessment of the facts disclosed above and taking into consideration

of similar experiences during renewal in group company, is confident of obtaining the renewal of land lease. The Useful life of PPE and ROU assets have been determined by the management considering that the lease would be extended. The entire production facility is located on this leased land. -

The table is being published in quarterly PPT but if you can show me how you are getting this number.

-

This is being answered and we can see this in Annual Report as well. Around Rs.18.60 crore as commission to MD which is obviously odd but not hidden.

Capacit’e Infraprojects (31-08-2023)

Isn’t the 6th point in the AGM notice shared yesterday that I have shared as screenshot say they intend to increase? Am I missing something?