Posts in category Value Pickr

How to build a concentrated PF (22-08-2023)

Value investing is tough compared to growth investing, in the sense that, it is relatively easy to go with where there is activity, where there is participation, where there is coverage, more things come to light, valuations could be high, sure, but they could remain so for more quarters, and investors who do growth or GARP type investing are reasonably sure if such valuations can sustain or not, and may think of coming out, and they find another such story.

Even for investors with many years of experience, it could be frustrating to see the price not moving as per their vision, there are a lot of moving parts.

The person who you replied has deep understanding of the business, so he bets on value, for others without such understanding, it is tough to make such calls.

As for me, I try all kinds, because they all work, I may not be able to do properly, but they all work depending upon some factors and in certain contexts. This is the reason why there exist many books on different philosophies in the market, because they all work. Jim Simons is correct, Buffett is correct, Lynch is correct, Joel Greenblatt is correct, Minvervini is correct, Michael Burry is correct.

Just saying.

Bull therapy 101-thread for technical analysis with the fundamentals (22-08-2023)

Doing pretty well, 1250 is big resistance, once this is taken can see 1500 to 2000 levels

Inox Wind Ltd

-

Management guiding for 500MW(2000cr-2500cr) installation this year and will conservatively do 700MW(2800cr-3500cr) my estimate in FY25. Current sales of 700cr.

-

Company will be debt free by Q4 FY24 (current interest cost is 330cr). They did a 500cr QIB on 8th august which will be used for clearing debt.

-

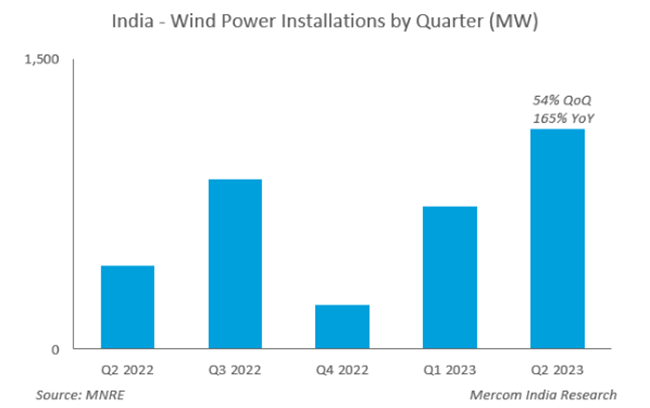

Current wind installation run rate is 4GW per year which will easily cross 5GW in FY25 and Inox historically maintained 20% market share hence ideally they should do 1GW.

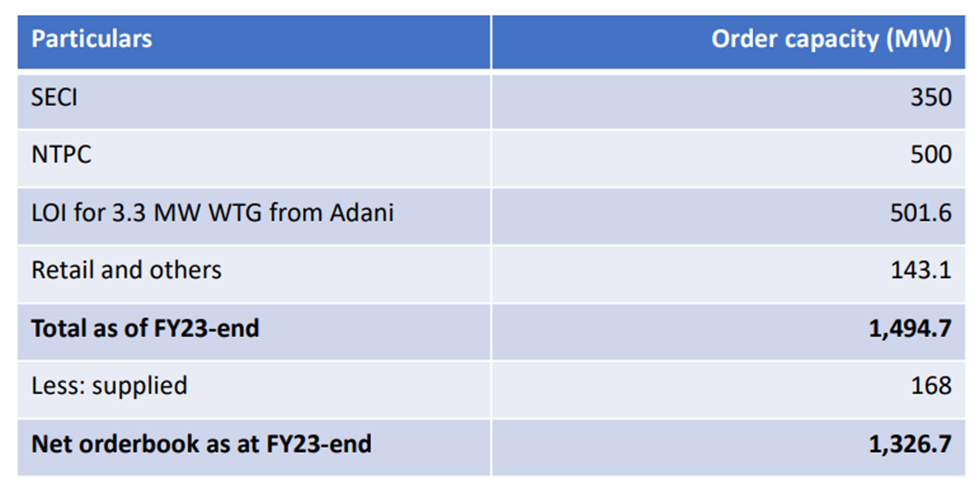

- Their current order book is 1.3GW and we still have 2.5GW of auction to be done this year from center (private not included) so as per me the demand> than supply. Hence the key thing now is execution apart from that everything is in place

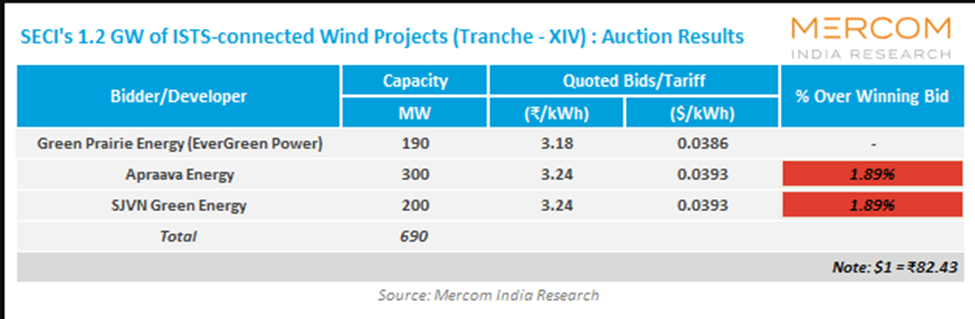

- Once of the biggest reason for the collapse of wind industry was tarrif. In a 1.2GW auction in June 2023 by SECI only 600MW qualified as bidding price were above cut off tariff. Margins will be at historical level 14% – 15%. Tariff went as low as 2rs per Kwh in 2019-2020, Currently at 3.24

TECHNICALS

Recently gave a big breakout and I expect from H2 we would see significant improvement in numbers.

- Current suzlon valuation is 17-20 times FY25 EPS ,if inox gets these valuations they should trade at 300 to 350 (Please note I am assuming a PE of 17-20, this is my base case assumption) @fundoo

I have already posted about them on their thread the reason I putting it here again is after the recent fall I have increased my initial position by 35% and at these levels the RR looks good..

Disc – Invested, with average price of 175

Bull therapy 101-thread for technical analysis with the fundamentals (22-08-2023)

Doing pretty well, 1250 is big resistance, once this is taken can see 1500 to 2000 levels

Inox Wind Ltd

-

Management guiding for 500MW(2000cr-2500cr) installation this year and will conservatively do 700MW(2800cr-3500cr) my estimate in FY25. Current sales of 700cr.

-

Company will be debt free by Q4 FY24 (current interest cost is 330cr). They did a 500cr QIB on 8th august which will be used for clearing debt.

-

Current wind installation run rate is 4GW per year which will easily cross 5GW in FY25 and Inox historically maintained 20% market share hence ideally they should do 1GW.

- Their current order book is 1.3GW and we still have 2.5GW of auction to be done this year from center (private not included) so as per me the demand> than supply. Hence the key thing now is execution apart from that everything is in place

- Once of the biggest reason for the collapse of wind industry was tarrif. In a 1.2GW auction in June 2023 by SECI only 600MW qualified as bidding price were above cut off tariff. Margins will be at historical level 14% – 15%. Tariff went as low as 2rs per Kwh in 2019-2020, Currently at 3.24

TECHNICALS

Recently gave a big breakout and I expect from H2 we would see significant improvement in numbers.

- Current suzlon valuation is 17-20 times FY25 EPS ,if inox gets these valuations they should trade at 300 to 350 (Please note I am assuming a PE of 17-20, this is my base case assumption) @fundoo

I have already posted about them on their thread the reason I putting it here again is after the recent fall I have increased my initial position by 35% and at these levels the RR looks good..

Disc – Invested, with average price of 175

My portfolio updates and investment journey (22-08-2023)

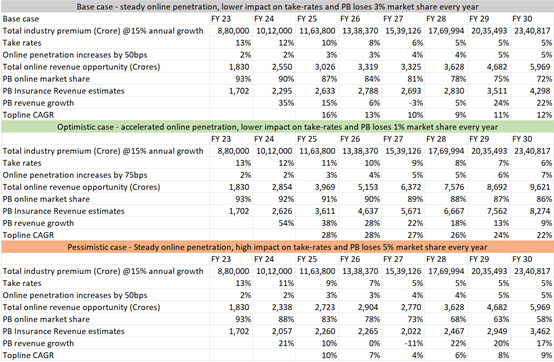

Satish thanks a lot for your comments. You raise excellent points. PB, PhonePe and Paytm Insurance are just brokers so I beleive there is some pricing gimmick. Either PhonePe is subsidizing it with low take rates or products offered are no-frills. The main strength of all these players is customer reach and conversion ability. As an investor we need to monitor and take the pain whenever necessary. We can take assumption and work with those. I have following back of envelope worst, base and optimistic scenario:

I assumed 15% insurance premium growth in all scenarios. In all scenarios in 6 to 8 years, return (CAGR) range is 4% to 28%. While on 2-3 years basis range is 7% to 28%. I played around with online penetration, take rates and lose in PB’s market share. All scenarios are on topline, while bottom-line growth might be higher than top-line owing operating leverage. Also note that PB has 5k crore cash, which can be used for buybacks in future.

In my assumptions Insurance online penetration best level is 7%, vs. 14% in United states and 6% in China.

Keep an eye, no investment is sure shot investment.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation

My portfolio updates and investment journey (22-08-2023)

Satish thanks a lot for your comments. You raise excellent points. PB, PhonePe and Paytm Insurance are just brokers so I beleive there is some pricing gimmick. Either PhonePe is subsidizing it with low take rates or products offered are no-frills. The main strength of all these players is customer reach and conversion ability. As an investor we need to monitor and take the pain whenever necessary. We can take assumption and work with those. I have following back of envelope worst, base and optimistic scenario:

I assumed 15% insurance premium growth in all scenarios. In all scenarios in 6 to 8 years, return (CAGR) range is 4% to 28%. While on 2-3 years basis range is 7% to 28%. I played around with online penetration, take rates and lose in PB’s market share. All scenarios are on topline, while bottom-line growth might be higher than top-line owing operating leverage. Also note that PB has 5k crore cash, which can be used for buybacks in future.

In my assumptions Insurance online penetration best level is 7%, vs. 14% in United states and 6% in China.

Keep an eye, no investment is sure shot investment.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation

Dynemic Products (22-08-2023)

(post deleted by author)

Dynemic Products (22-08-2023)

(post deleted by author)

Astec Lifesciences (22-08-2023)

Q1-2024(aug 2023) con call on astec life

(from godrej agrovet)

1…PERFORMANCE

There are 2 segments of the business.

A…Enterprise business

B…CDMO segment

A…Enterprise business

Poor performance was due to

A1 -Demand-supply imbalance and depressed realizations

in enterprise products portfolio in both domestic as well as global markets

=Topline and profitability were severely impacted due to sluggish demand, lower realizations and high-cost inventories of

enterprise products

A2 -High-cost inventories further impacted profitability

B…CDMO business

=Revenues grew 3.0x y-o-y led by new product development while profitability also improved

2…CDMO BUSINESS

=CDMO business in Astec LifeSciences expected to see 20-30% growth YoY.

=Capex plans include expansion in Mahad and new multipurpose plant.

=If you look historically for the CDMO business, we have been doubling our revenue, obviously from a smaller base, but we have been doubling our revenue year-on-year. So our revenue was close to INR 84 crores a couple of years back, last year we closed at INR 162 crores. And coming year,

we would like to maintain almost similar or closer to that run rate. So that is our guidance on

how it looks like.

= I think one of the key requirements for a successful CDMO portfolio is R&D, and I can definitely say that within 6 months of submissions R&D center, we are hand full with several projects And as you were aware that the new R&D center, which has come up, we are almost doubling

down our efforts on CDMO component of the business, which lead us to believe that we would

like to work on 20%, 30% growth at least year-on-year on the CDMO side of the business

=Some of these products have gone from the development piloting to commercial, which has

added to the revenue. But in other cases, we have also built the newer pipeline under the new

R&D center now, we are in a very good situation to double down or triple down on those pipelines.

=This cycle for CDMO, as you know, right from development or scale up to commercial take 3 to 4 years. So there has been a lot of activities that has been done over the

last couple of years to build this pipeline. And with the new R&D center coming up, this will only expedite that entire pipeline generation process. And we expect to reap benefits as we move forward in the coming years.

= On a small base, initially, we may double it once or twice. But on a steady state basis, we are looking at, when steady state is FY 25 onwards. We are looking at the 20% to 25%

increase in CDMO business because that will be our focus.

=And not only the focus on sales, but also focus on investments. Because whatever comes out of

our R&D center in terms of co-creation or working with some partners, it would require us to

put production infrastructure also in time to come. So we have a very aggressive plan.

=And I’m very sure that we are likely to make CDMO a significant part of Astec business in time to come.

Q: We have time let say in the next couple of 3-4 years. So in the

Astec LifeSciences, CDMO business will be bigger than the enterprise business?

Management : So that is our plan and hope, but I cannot say what will happen in future, like we could not

predict for the last 3-4 quarters, what has happened in the pesticides market across the world. So

I think that said that on a long-term basis, the answer is a very big yes.

3…ENTERPRISE BUSINESS

=Astec along with other companies in the market are facing similar headwinds of high inventory, there’s been destocking, which is

happening at the customer level.

=For some of the enterprise products, we believe that the bottom has already reached. We still see some muted prices on to enterprise products. On the others, we are still seeing that the

liquidation in the inventories and the market might take a few more months. And then the market

from the supply demand side could balance out.

=So overall, I would say that things have improved from the last few quarters. It might take you a few more months to achieve normalcy

we see it currently.

=Obviously, we were thinking of the downtrend, but the extent of this huge downtrend was unexpected. We have taken few steps to prevent further down trend

A…We have planned for diversifying our product portfolio with the new R&D center coming in, it has offered us enough flexibility now to experiment and put some of the new product at a much profitable.

B…We are heavily focusing on building sustainable margins from CDMO business and also trying to push some of the new products as soon as what

to mitigate this downtrend from our existing portfolio

C…While our focus primarily on the CDMO business, on the enterprise business, since we have a

very strong triazole platform, technology platform, and we are also investing heavily on some

of the other adjacent platform with the new R&D center. We’ll be strategically looking at molecules within that segment as well to work on and launch in the coming years. While the

focus is more on building the pipeline on CDMO, we’ll also take strategic bets within the enterprise segment.

4…HERBICIDE PLANT

=We will utilize this plant within 3 years and ramp up accordingly and with an asset turn generating 1.6 to 1.8 roughly in that range. We are very much on target or exceeding those targets on the herbicide plant.

5…CAPEX

A=The herbicides Phase I

Phase 1@INR 120 – 130 crores is what we are estimating. And we expect that to be commercialized by end of this year.

There’ll be 2 more capex.

B…Mahad

= We have some more ability to expand in Mahad. So we will set up another facility in Mahad, which will be very similar in size in capex as the one which we have already established.

C… But the big capex will

come – which will drive our CDMO, that will take a long time.

=I think we are still working out

what kind of multipurpose plant we have. But I think that should be finalized in 3 to 4 months’

time.

Disc…invested

Astec Lifesciences (22-08-2023)

Q1-2024(aug 2023) con call on astec life

(from godrej agrovet)

1…PERFORMANCE

There are 2 segments of the business.

A…Enterprise business

B…CDMO segment

A…Enterprise business

Poor performance was due to

A1 -Demand-supply imbalance and depressed realizations

in enterprise products portfolio in both domestic as well as global markets

=Topline and profitability were severely impacted due to sluggish demand, lower realizations and high-cost inventories of

enterprise products

A2 -High-cost inventories further impacted profitability

B…CDMO business

=Revenues grew 3.0x y-o-y led by new product development while profitability also improved

2…CDMO BUSINESS

=CDMO business in Astec LifeSciences expected to see 20-30% growth YoY.

=Capex plans include expansion in Mahad and new multipurpose plant.

=If you look historically for the CDMO business, we have been doubling our revenue, obviously from a smaller base, but we have been doubling our revenue year-on-year. So our revenue was close to INR 84 crores a couple of years back, last year we closed at INR 162 crores. And coming year,

we would like to maintain almost similar or closer to that run rate. So that is our guidance on

how it looks like.

= I think one of the key requirements for a successful CDMO portfolio is R&D, and I can definitely say that within 6 months of submissions R&D center, we are hand full with several projects And as you were aware that the new R&D center, which has come up, we are almost doubling

down our efforts on CDMO component of the business, which lead us to believe that we would

like to work on 20%, 30% growth at least year-on-year on the CDMO side of the business

=Some of these products have gone from the development piloting to commercial, which has

added to the revenue. But in other cases, we have also built the newer pipeline under the new

R&D center now, we are in a very good situation to double down or triple down on those pipelines.

=This cycle for CDMO, as you know, right from development or scale up to commercial take 3 to 4 years. So there has been a lot of activities that has been done over the

last couple of years to build this pipeline. And with the new R&D center coming up, this will only expedite that entire pipeline generation process. And we expect to reap benefits as we move forward in the coming years.

= On a small base, initially, we may double it once or twice. But on a steady state basis, we are looking at, when steady state is FY 25 onwards. We are looking at the 20% to 25%

increase in CDMO business because that will be our focus.

=And not only the focus on sales, but also focus on investments. Because whatever comes out of

our R&D center in terms of co-creation or working with some partners, it would require us to

put production infrastructure also in time to come. So we have a very aggressive plan.

=And I’m very sure that we are likely to make CDMO a significant part of Astec business in time to come.

Q: We have time let say in the next couple of 3-4 years. So in the

Astec LifeSciences, CDMO business will be bigger than the enterprise business?

Management : So that is our plan and hope, but I cannot say what will happen in future, like we could not

predict for the last 3-4 quarters, what has happened in the pesticides market across the world. So

I think that said that on a long-term basis, the answer is a very big yes.

3…ENTERPRISE BUSINESS

=Astec along with other companies in the market are facing similar headwinds of high inventory, there’s been destocking, which is

happening at the customer level.

=For some of the enterprise products, we believe that the bottom has already reached. We still see some muted prices on to enterprise products. On the others, we are still seeing that the

liquidation in the inventories and the market might take a few more months. And then the market

from the supply demand side could balance out.

=So overall, I would say that things have improved from the last few quarters. It might take you a few more months to achieve normalcy

we see it currently.

=Obviously, we were thinking of the downtrend, but the extent of this huge downtrend was unexpected. We have taken few steps to prevent further down trend

A…We have planned for diversifying our product portfolio with the new R&D center coming in, it has offered us enough flexibility now to experiment and put some of the new product at a much profitable.

B…We are heavily focusing on building sustainable margins from CDMO business and also trying to push some of the new products as soon as what

to mitigate this downtrend from our existing portfolio

C…While our focus primarily on the CDMO business, on the enterprise business, since we have a

very strong triazole platform, technology platform, and we are also investing heavily on some

of the other adjacent platform with the new R&D center. We’ll be strategically looking at molecules within that segment as well to work on and launch in the coming years. While the

focus is more on building the pipeline on CDMO, we’ll also take strategic bets within the enterprise segment.

4…HERBICIDE PLANT

=We will utilize this plant within 3 years and ramp up accordingly and with an asset turn generating 1.6 to 1.8 roughly in that range. We are very much on target or exceeding those targets on the herbicide plant.

5…CAPEX

A=The herbicides Phase I

Phase 1@INR 120 – 130 crores is what we are estimating. And we expect that to be commercialized by end of this year.

There’ll be 2 more capex.

B…Mahad

= We have some more ability to expand in Mahad. So we will set up another facility in Mahad, which will be very similar in size in capex as the one which we have already established.

C… But the big capex will

come – which will drive our CDMO, that will take a long time.

=I think we are still working out

what kind of multipurpose plant we have. But I think that should be finalized in 3 to 4 months’

time.

Disc…invested