Where do you get this MDF export import numbers from

Posts in category Value Pickr

Rushil Decor – Real Estate revival + MDF Adoption Play (12-09-2022)

Maybe yes… but i have learnt the hard way… trying to find next asian paints, hdfc bank, pidilite :)…

Valuation for greenpanel is anyways better hence not sure about scope for rerating… could go wrong…

Dish TV 10 bagger stock (12-09-2022)

Dish TV is good candidate for being acquired. Even goels will want to get best price for dish tv. as they are on path of reconciliation. apart from stepping down as md they have agreed to appoint yes bank nominees on the board. this is heading in right direction for all shareholders… and also employees.

Kalpesh’s Portfolio (12-09-2022)

@kalpesh4430 Dont you consider mgmt of Satia not doing Q1Fy23 concall or press media as a major red flag. Considering the volatile environment and company feeling the pressure on margins mgmt should have at least published some media statement detailing out the dynamics that are played out in Q1Fy23 and future path. I want to increase my allocations but not getting any visibility from mgmt via concalls is stopping me to increase further. Whats your view on this ?

Disc : Invested

Rushil Decor – Real Estate revival + MDF Adoption Play (12-09-2022)

Investors make the most money when bad/worse numbers become good/better numbers. You need to study the 2 companies to understand in the near term, whose financial are going from not-so-good to good and whose are remaining stable.

Rushil Decor – Real Estate revival + MDF Adoption Play (12-09-2022)

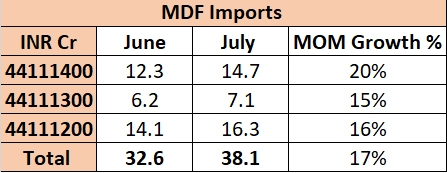

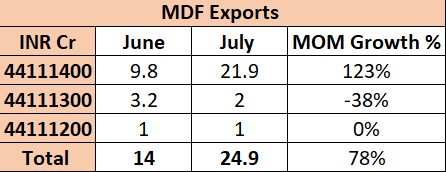

July import-export values are out.

MDF imports have grown by 17% MoM but exports have increased by a whopping 78% MoM. June export numbers were low, so this MoM export growth is a little misleading. However, average monthly exports in Q1 FY23 were 25.5Cr, so the July numbers of 25Cr remain on trend and strong.

My interpretation : Freights are cooling off slowly but are still much higher than they were 2 years ago when imports were really strong. Export market remains healthy going by export revenues in July (Export realization data is needed to confirm this but that will only be available in Oct when Greenpanel releases its data).

Of course this data is with a lag of 1.5 months, so intervening changes in freights and import/export will affect real time data. Global freights seem to have come down by ~7% MoM from July to Aug, so this will have some incremental impact in Aug and Sep numbers.

Tracking freight remains a key for this stock. Going by the trend so far I am not expecting any significant dent in realizations in Q2. If freights keep coming down secularly in Q3 and Q4 then we might start seeing some moderation in realizations in late Q3-Q4. Shall wait for Q2 results to evaluate further.

My portfolio-Nibin (12-09-2022)

Sold off gravita (entry 250)

Any specific reason for you to exit Gravita?

Investing Basics – Feel free to ask the most basic questions (12-09-2022)

Sir,

Shareholders transacting more than 5 lac shares are eligible for block deal window. Block deals happen on exchanges in specific times, usually at pre negotiated prices. Dealers of institutions call other institutions if they have a chunk of shares and are willing to sell. There are many investment bankers offering this service. They have an informal network of who wants to buy and sell. The deal takes few days to complete and is formalised at exchange.

Gujarat Fluorochemicals: A hidden fluorine story (12-09-2022)

One of the questions that were asked to GFL’s management, on one of the last 2-3 concalls was pertaining to a Chinese LiPF6 manufacturer called Tinci Materials.

And here’s a press release on LipF6 by the same co. The original content is in Chinese but I have translated it using Chrome.

Tianci Materials: Quantitative increase, growth and realization, and profitability stability is highlighted

Release time: 2022-09-02

Source: Changjiang Securities | Researchers: Ma Jun, Wu Bohua, Si Hongli

Event description

The company released the 2022 interim report. In the first half of the year, it achieved revenue of 10.4 billion yuan, a year-on-year increase of 180%; net profit attributable to shareholders of the parent company was 2.91 billion yuan, a year-on-year increase of 271%. It fell within the range of the previous performance forecast.

event comment

The company achieved high growth in both revenue and profit in the first half of the year, mainly benefiting from the lithium battery material sector: 1) The revenue of lithium battery materials in the first half of the year was 9.6 billion yuan, a year-on-year increase of 206%. With the rapid price increase in the electrolyte industry chain since last year, it is expected that the average price of electrolyte in the first half of the year will increase significantly year-on-year, contributing to a high growth in revenue. At the same time, benefiting from the price increase in the industrial chain, the company’s gross profit margin of lithium battery materials reached 44% in the first half of the year, an increase of about 8pct year-on-year, helping to further accelerate profit growth. 2) The daily chemical business achieved revenue of 540 million yuan in the first half of the year, a year-on-year increase of 18%, and the overall growth rate remained stable; the daily chemical business gross profit margin in the first half of the year was 28%, a year-on-year decrease of 7.5pct.

From the perspective of the second quarter alone, the company achieved revenue of 5.2 billion yuan in 2022Q2, maintaining a high growth rate of more than doubling year-on-year, and basically flat month-on-month. It is expected that the main reason is that the electric vehicle industry chain, especially the downstream terminals, was affected by the epidemic in the second quarter. The goods were generally flat Q1, and due to the impact of the epidemic on demand, the price of the electrolyte industry chain (such as the price of 6F calculated by third-party platforms) has declined. Specifically, in 2022Q2, the company achieved a gross profit margin of 42%, a significant year-on-year increase, and a decrease of about 2pct from Q1. The overall decline was relatively limited and significantly lower than the 6F price drop reported by third-party platforms. We believe that to a certain extent, 6F bulk orders have been verified. Lower prices have less impact on the company’s actual profitability.

In other financial aspects, the company’s net operating cash flow in 2022Q2 was 1.86 billion yuan, a significant increase from the previous month, and the overall operating quality was relatively high; the company’s capital expenditure in 2022Q2 was about 870 million yuan, a significant increase year-on-year and month-on-month, reflecting the company’s accelerated production capacity construction. Specifically, the company currently owns Guangzhou, Jiujiang, Ningde, Yichun, Chizhou, Taizhou, Liyang, Quzhou, Fuding (under construction), Fogang (under construction), Yichang (under construction), Sichuan Meishan (under construction), Jiangmen (under construction), Nantong (under construction), Europe (under construction) and other supply bases, a national and key international regional strategic supply system has been established. The electrolyte production capacity, 6F production capacity, and LiFSI production capacity related to the electrolyte industry chain are all planned to be relatively large, and new production capacity will continue to be released this year and in the future, and the company also plans a large production capacity in terms of the cathode material iron phosphate precursor, which is expected to support in the future. The high growth of the company’s cathode material shipments.

Looking forward to the follow-up, the prosperity of the electric vehicle industry chain has continued to rise since Q3.

In the second half of the year, with the release of the company’s 6F and LiFSI technological transformation and new production capacity, it is expected that shipments are expected to grow faster than the previous month.

At the same time, the company continues to strengthen the vertical and horizontal layout of the industry chain, strengthen the cost advantage of the electrolyte industry chain, and develop new growth points (iron phosphate, battery recycling, binders and other new materials).