Per the Founder/Directors, they will not be spending anything additional to boost their airline business as they believe they are already well placed there. Any tailwinds in the air travel sector will also help them. All their future spends/investments/in-organic growth will be focused towards Bus/Hotels/Travel business as that is where they see they have a huge market to address and with higher margins.

Posts in category Value Pickr

Rossell India Ltd (01-09-2022)

I had looked at Rossell few weeks back and in the couple of hours I spent, I came away with so many questions and doubts. I see that this company has piqued the interest of the investing community due to this Techsys division’s foray into aviation/defense manufacturing. It does sound exciting but this did not pass some of my basic filters and smell tests.

- We would assume this is high-tech vertical in the defence space but looking at the margins doesn’t seem to say so.

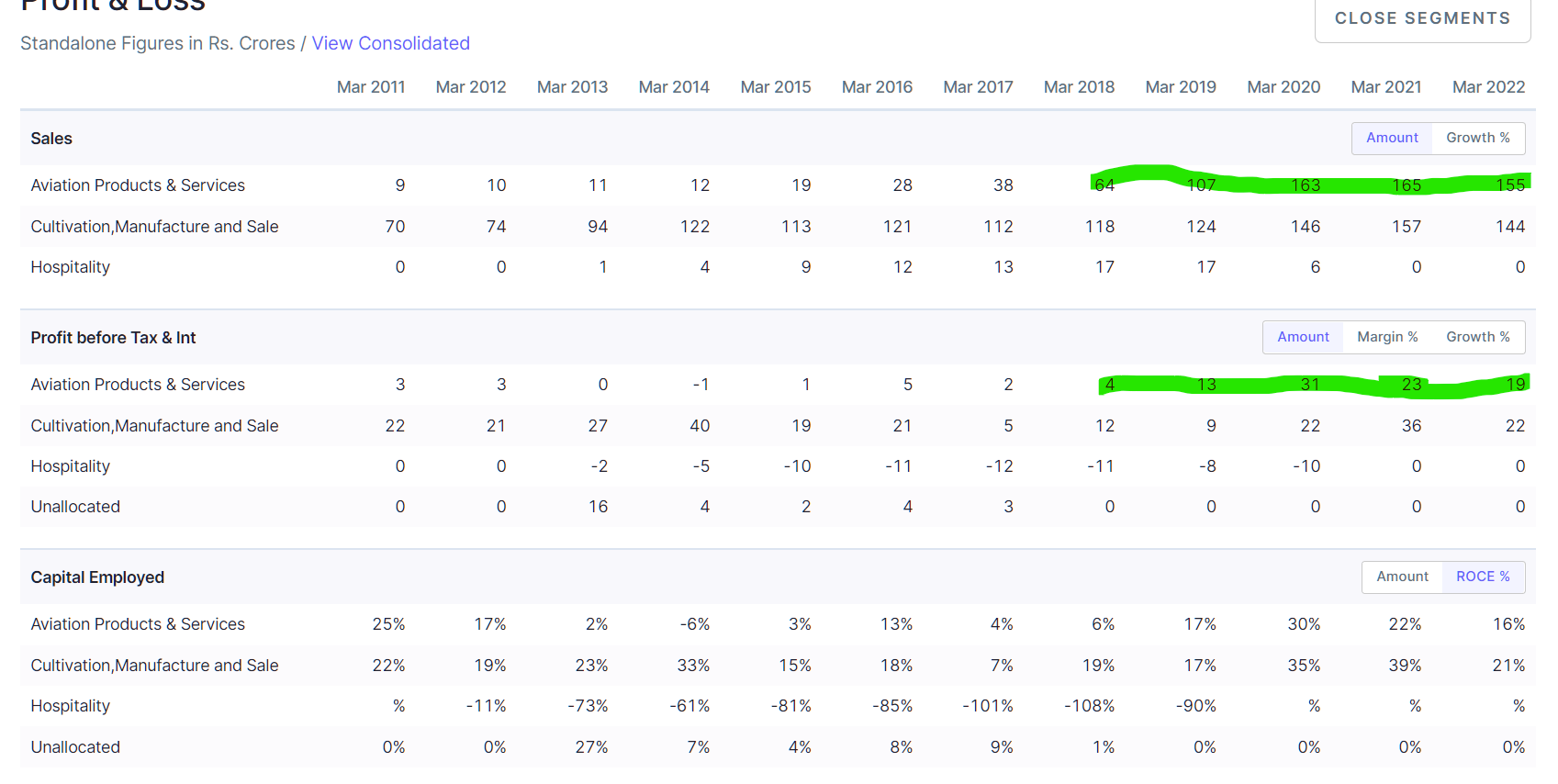

Although the topline has grown consistently, the margins between FY18-FY22 has gone like this 6% → 12% → 19% → 14% → 12%. That’s a wide range and a lot of variation. This does not give the impression of a business doing a lot of value-add. It means that the value-add is minimal/marginal and is being drowned out by the variation in gross margins?

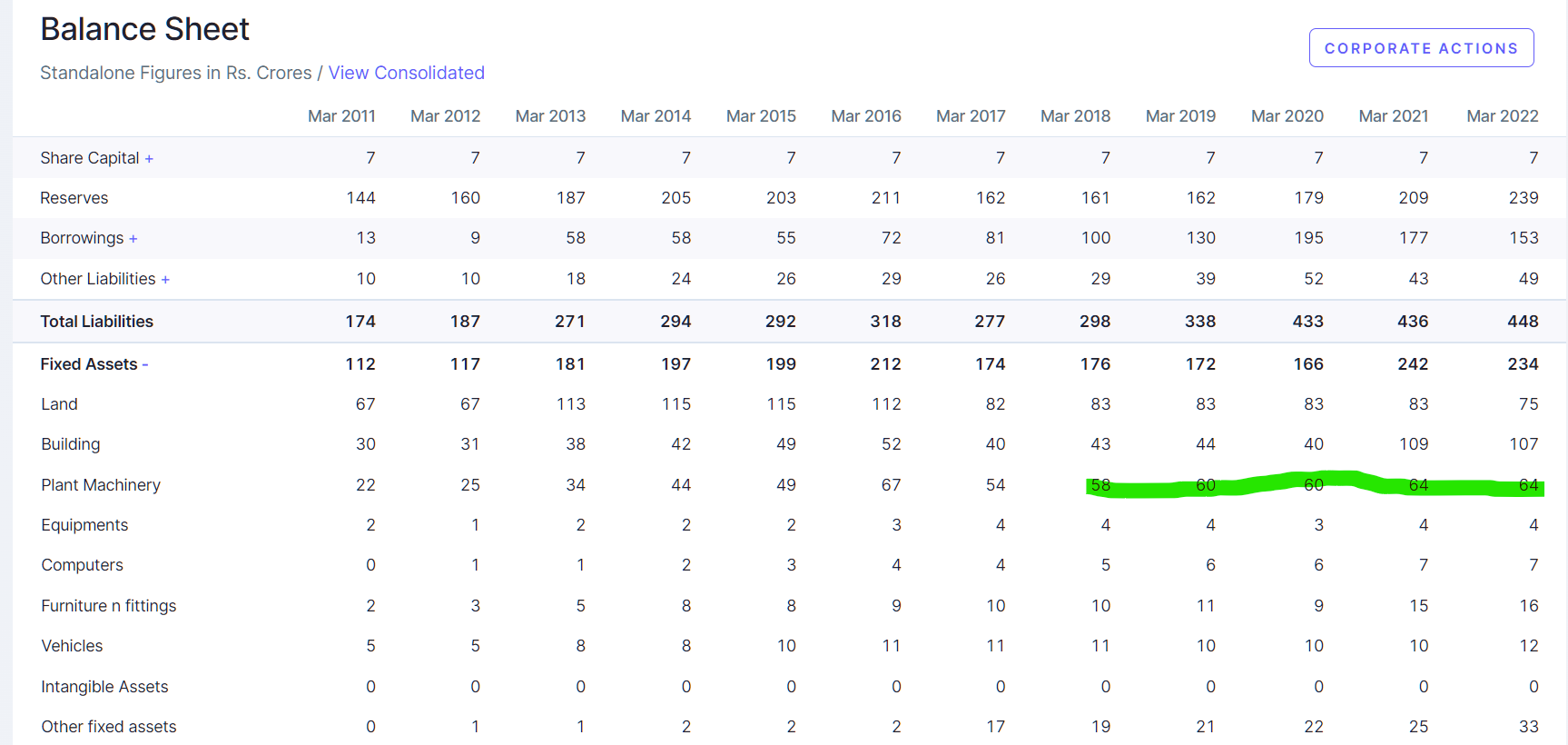

- While the topline has grown from 64 Cr to 155 Cr. Has the company put up any capex in plant and machinery to handle these new orders?

Clearly, this business doesn’t need a lot of investment in plant & machinery, so the possibility is that this is a very labour intensive business and probably the value-add in this business is purely labour? That might also explain the good RoCE (Tea is a labour intensive industry - so this business is more close to Tea business than a pure-play defense business like HAL with 24% OPM and ~55% GM?) So does it mean that when this business get a 2000 Cr order, they will have to hire a lot of labour to scale?

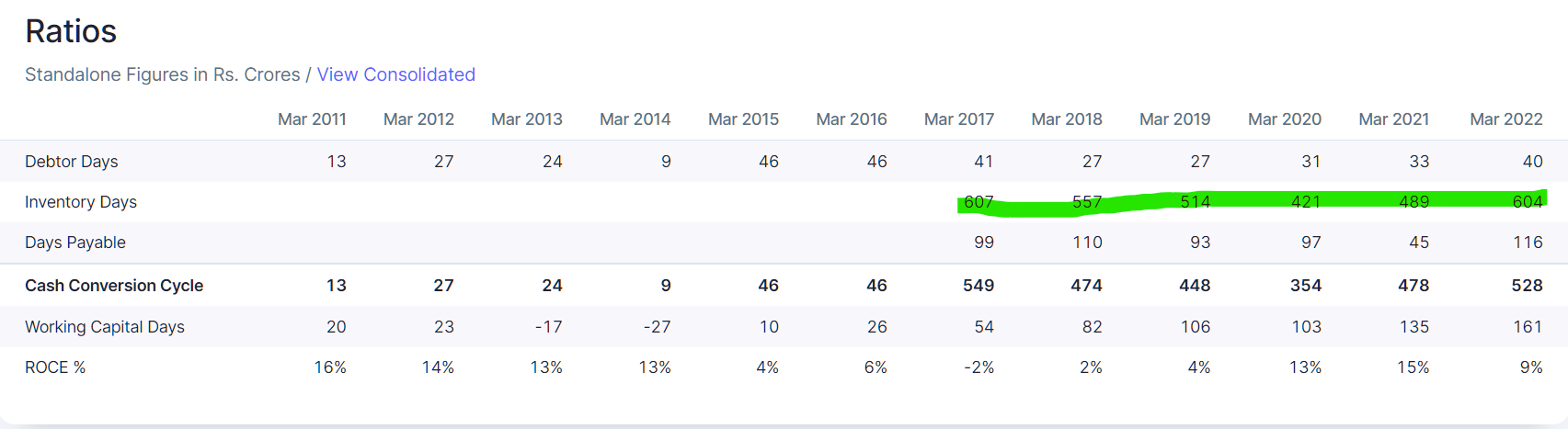

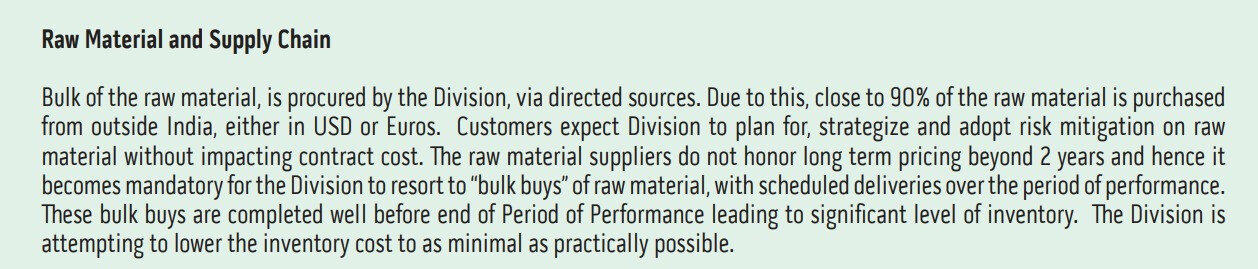

- Another line of thought, that jumps up when looking at Inventory days.

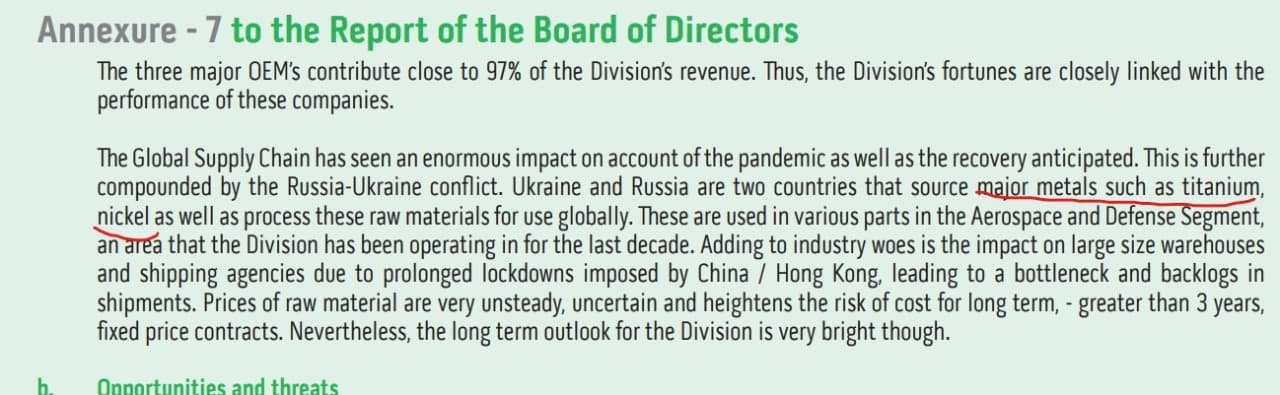

The inventory days are awfully high. That’s like a 1.5 years or so! No other tea business has such poor cash conversion cycle. So clearly this has something to do with Techsys division. They have to procure RM and perform labour-intensive tasks on it for a year or more before they can ship? Does the vendor cover forex fluctuations? The management seems to think that Rupee depreciation is a natual hedge. What happens when Rupee appreciates instead?

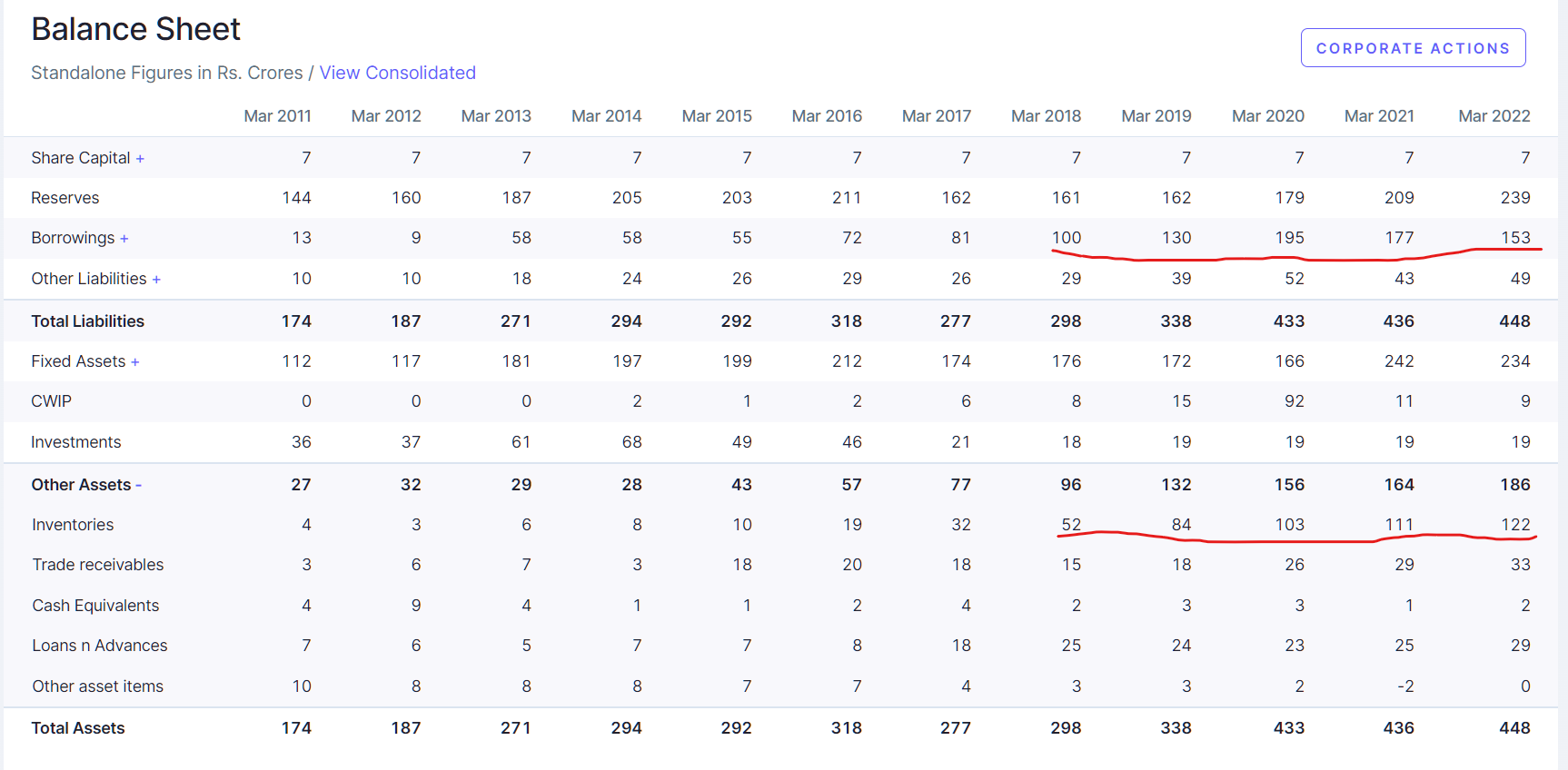

- So who funds this inventory? Do they have a relationship with Boeing or whoever to fund this liability? Looking the balance sheet sheds some light

So these guys have to borrow to buy whatever this commodity is on their own for orders to be delivered 1.5-2 years later. So a 2000 Cr order might mean they may have to borrow 1200-1500 Cr and trust the Rupee to be a natural hedge? (90% of RM is imported)

If you see the above two, the RM price fluctuates over the long-term a fair bit and going by back of the envelope calculations, the Gross Margins here may not be more than 20% and the labour value-add perhaps around 5% (Am assuming this is unskilled labour with a low-wage)

The worst case for this company is when they win a 2000 Cr order, raise debt and buy inventory and RM price crashes over the next year and Rupee appreciates. It can essentially wipe-out everything.

Again, I am making a lot of guesswork here because the AR or AGM transcript is so opaque. So many good questions asked by participants and the answers by the management are outright comical (in my opinion)

Whenever I see stuff like this, I run away.

Disc: Just a customary glance and not invested due to lack of clarity and what I consider are red flags. Posting here because I might be missing something.

Easy Trip Planners (Easemytrip) – An outlier in OTA (01-09-2022)

Here is why:)

where will the company get the growth from and for how long the company will show YOY growth

domestic air passenger count will go down in Q2 as compared to Q1, so will be the margin + compettitve intensity is back (corporate travel is back and EMT is not a player there)

now they will raise the money to put where? acquire something in non air space like some bus oerator or invest in discouting to build hotel business:)

coming soon-- another share split to give some lollypoop to investors

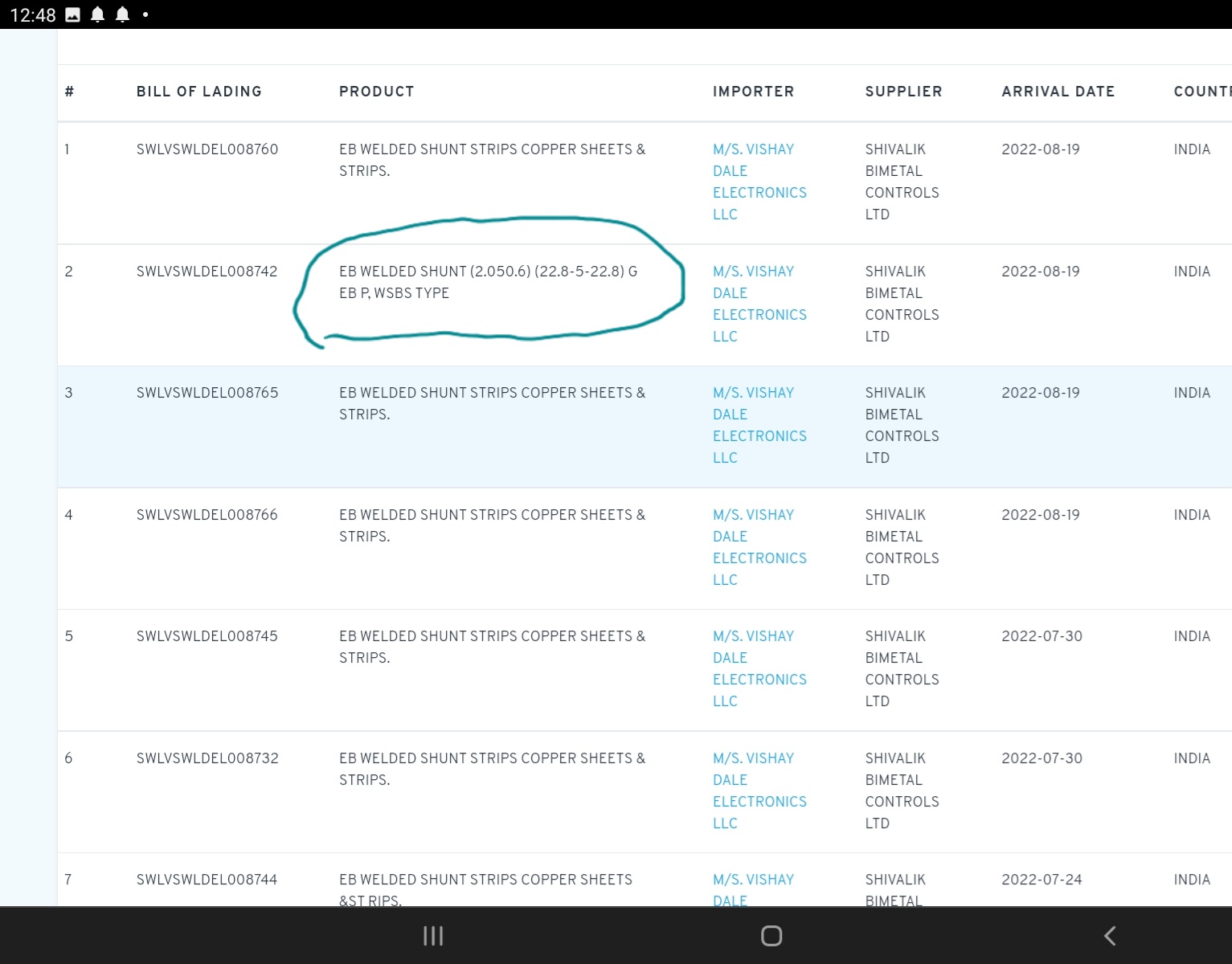

Shivalik Bimetal Controls Ltd (SBCL) (01-09-2022)

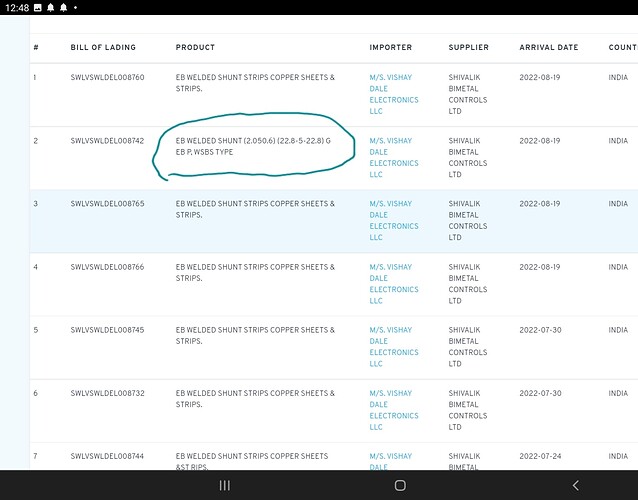

A logical question to ask is what are the possibilities for Shivalik shunts - here is a clue

- Shivalik sells in India for INR 15+ for 10K+ order.

Vishay sells for $12-$15 per peice for WSBS type shunts ( type ties to shivalik in points below) - though smaller quantities possible. This is a multfold markup, even after considering various overheads involved and sales infra reqd.

If one were to look at how much of Vishay shunt offerings are covered by Shivalik - my sense is a sizable - infact nomenclature may offer a clue Now one can imagine critical supplier status Shivalik holds for Vishay - if shivalik were to raise prices - will there be lot of resistance? Anybody’s guess!!!

- To further tie shivalik shipment to above nomenclature- here is a latest shipment data. Looks dor WSBS type - usually it hasnt been disclosed earlier.

It would be interesting to understand Shivalik strategy/Aspirations of direct supply in shunts( they already are doing bimetals), constraints per Vishay contracts.

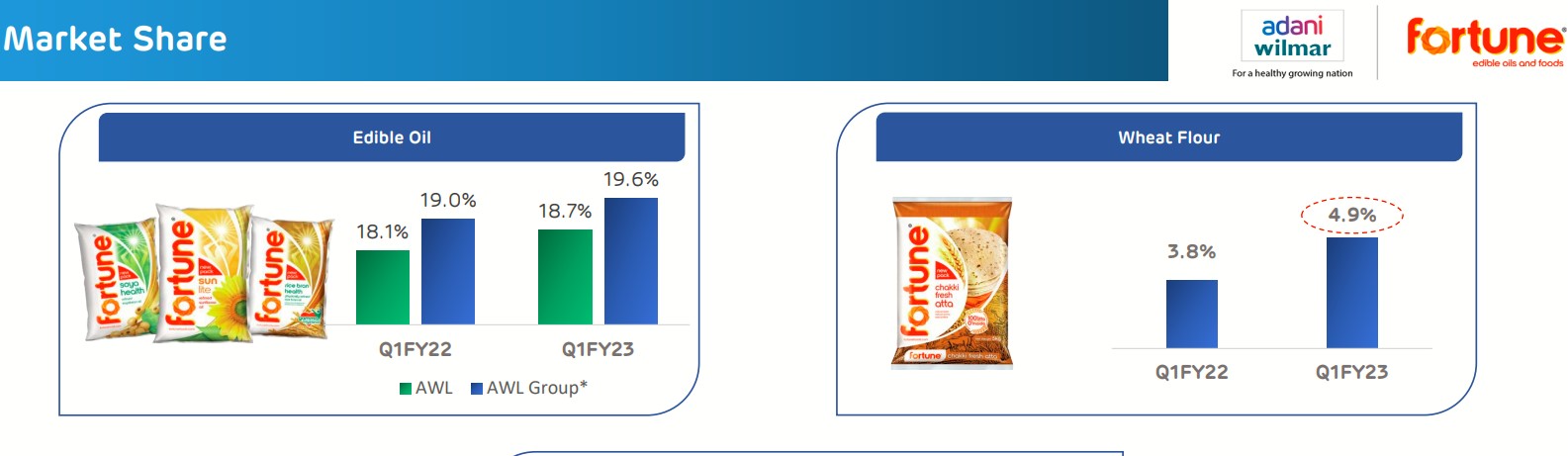

Patanjali Foods – may be a big winner in the long term (01-09-2022)

Adani Wilmar has a 19% market share in Edible Oils.

They have posted 30% revenue growth and 10% pat growth which is quite similar to Patanjali

AWL is sitting on 2200 cr of growth capital which they raised from IPO, this can help them propel the business further

Inflame Appliances (01-09-2022)

Big breakout today on the price front. Trade volume data shows high delivery percentage. Is this real or the hanky panky of operators is very difficult to know (at least for me). As @gaurav_vimal Gaurav_vimal mentioned, the report from credit rating agency on “company not cooperating” is a dampener.

Company only publishes results twice a year. I think this might be true for most micro caps. Might take a small tracking position to learn more about micro cap investing, purely for learning ropes. No recommendations - investing in such companies is extremely risky!!!

Best Agrolife – Think Big, Think Best! (01-09-2022)

Thankyou @Tanay_Malpani for the research. Would be thankful if you can tell how did you identified this company? This doesn’t show in any of my screeners because of less number of years but still it would be interesting to know how did you found Best Agrolife.

Chemicals/pharmaceuticals has remained my Achilles Heel. What I understand is that agro chemicals are now commoditized. In such a scenario how does Best Agrolife command such high ROEs? How are their products different from already existing agro chemicals? From their growth it looks like these products work like magic.

FAZE THREE LTD. –A Textile co. Rising From ASHES to GLORY (01-09-2022)

HDFC Securities have come out with a report on the company:

Zomato – Should you order? (01-09-2022)

In my view, there are a few big fundamental issues with the business.

-

Peak Margins - The company may struggle for many years to increase its margins. the commission they charge to the restaurants is already very high and the possibility to increase it is very very slim. Restaurants are not happy with the % delivery apps are charging them and some of them are already looking for alternatives to delivery apps.

-

Restaurant listing and placement on the app - The mobile screen is small and at a time only listed numbers of restaurants can be shown on the app. the restaurants which have paid promotions show up top, this means that there may be restaurants with better food out there but u might end buying from the restaurant with the top 5/10 in the search option. This is a disadvantage to the restaurants listed on the app and slowly they will realize this.

-

The restaurant business may have gone higher however that has been offset by the commissions they pay to delivery apps and the upfront fees to list themselves. my friend used to run a cloud kitchen in Bandra and i have the costs of delivery apps on the margins. they had to shut down eventually because they were tired of all the discounting happening during that time. this was in 2018-2019.

now that they are listed they will be answerable to analysts and institutions and their cards are in the open. Capital Markets are about efficient use of capital and those who so over manage to do that get the vote of the investors.

All those huge cash burns ideas are not going to fly now. it can be a good buy at its price to book value of 21 rs.