Quaterly Results mostly flatish.

Huge increase in employee expenses Y-o-Y.

Lets wait and see their presentation

Posts in category Value Pickr

Manappuram Finance (04-08-2022)

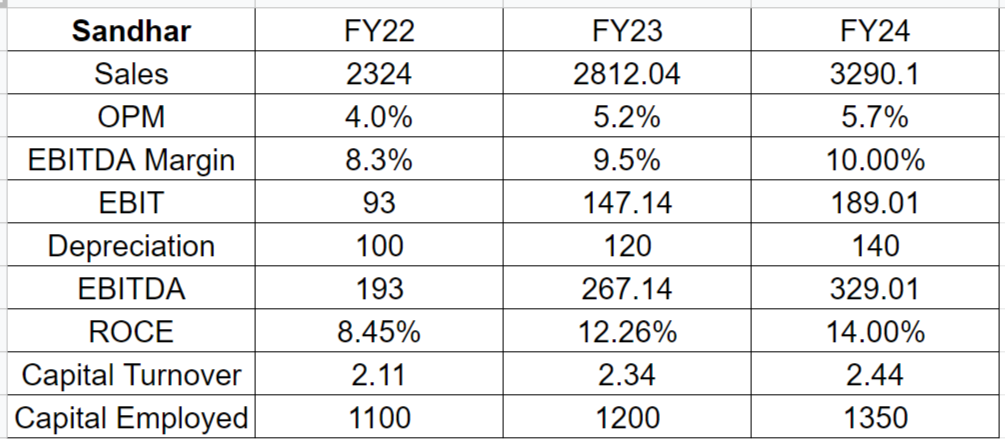

Sandhar Technologies – An emerging market leader (04-08-2022)

Below average results by Sandhar.

-

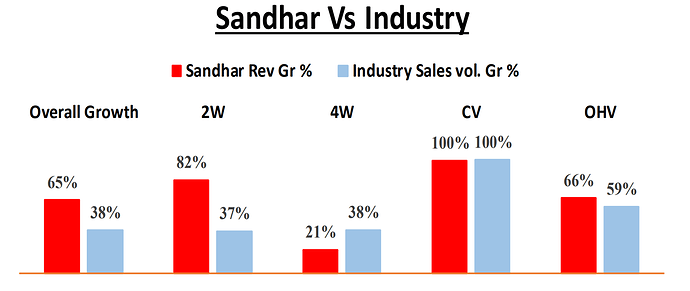

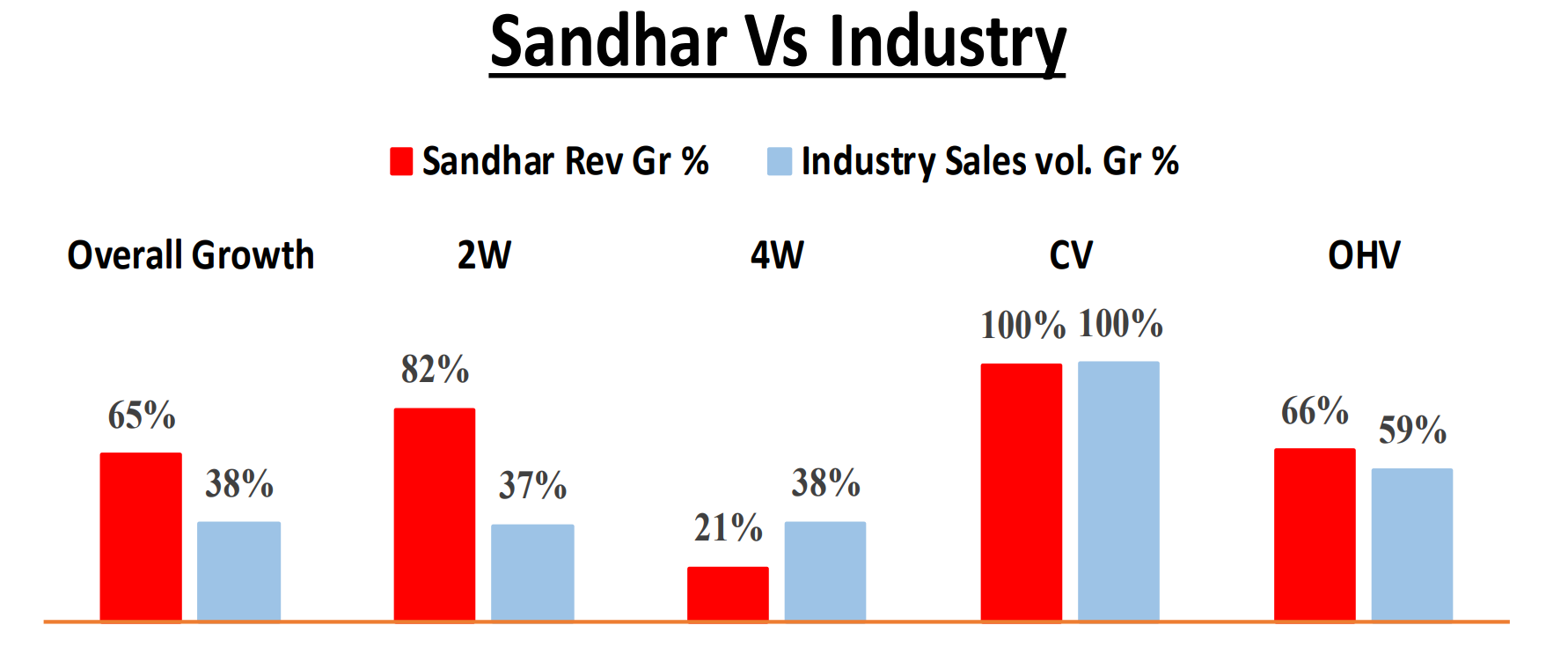

On revenues. Flattish Q-on-Q. Aggresive guidance by mgmt hasnt yet played out. Although they have continued to do better than their industry overall.

-

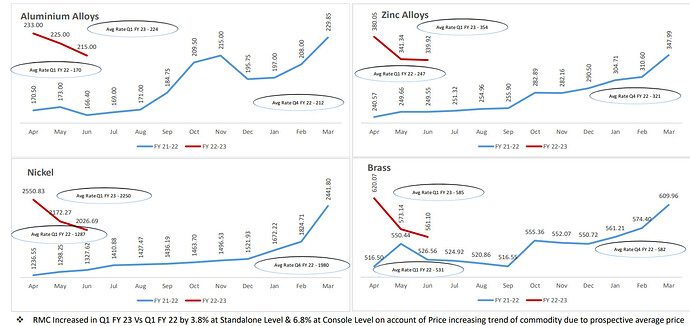

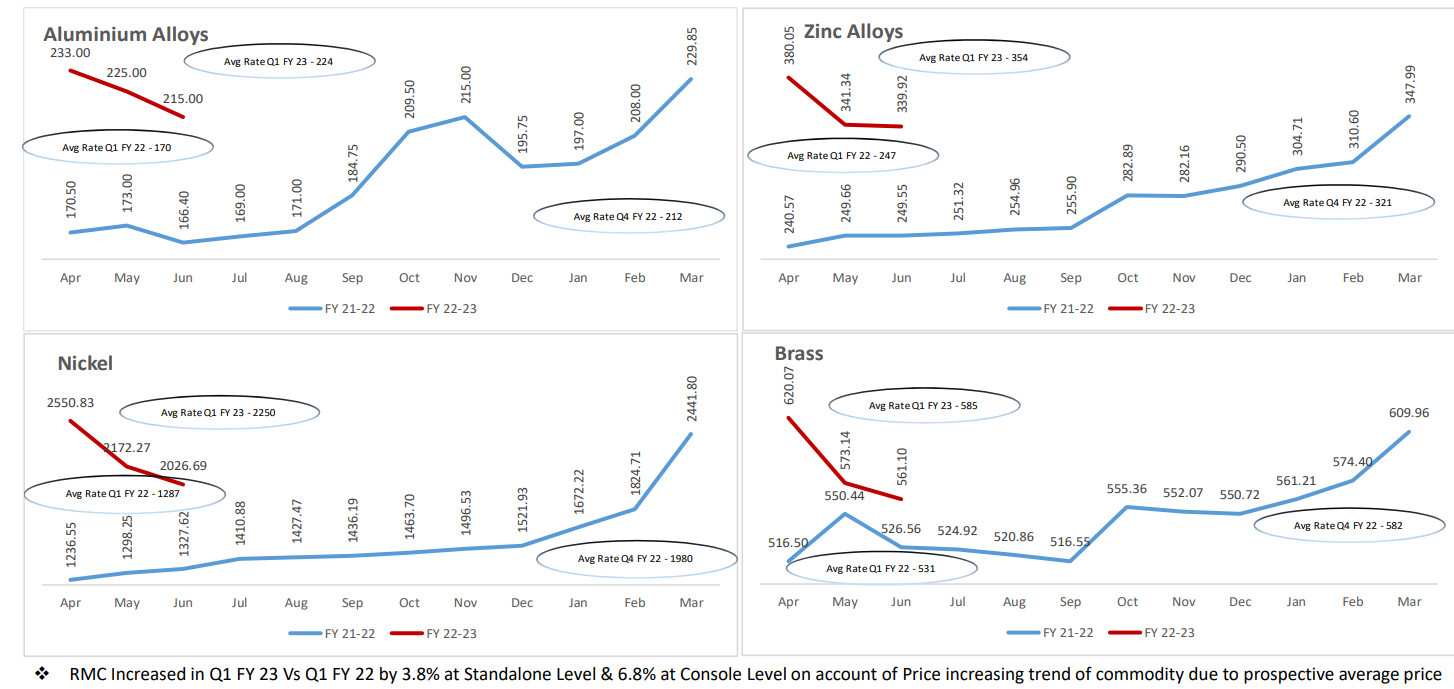

On margin front. A central part of my thesis is RM cooling off which has also continued to rise(not under managements control). Costs continue to be a drag.

Auto sector volumes look promising, in Sandhar’s case, 2W industry has not come back to its 2019 numbers yet. We might be poised for a cyclical upturn.

Over the next 2 years, RM prices should ideally cool off and margins can surpass 10% mark easily. IMO, if company can register a sales growth of 20-25% or higher for the year with 9.5%+ margins for FY23 with an auto upcycle, it could trade 1x price to sales.

Another thing to monitor is cost of debt. Sandhar has a levered b/s with 0.7x D/E(high considering ROEs here are sub 10%). Higher interest rates could visibly dent Sandhars P/L. Already interest costs have risen from 4 crores to 7 crores. For a not very profitable biz like Sandhar these costs will affect earnings by a lot. Will be interesting to see interest costs for Q2.

They have also depreciated 29 crores(I assume this would increase over the year) as against ~25 crores.

As against what I projected, depreciation qrtrly run rate is already up there, so looks like it would increase.

Key things to monitor here on IMO would be RM prices + mgmt execution on increasing wallet share. As mentioned, Hero isnt doing as well as TVS and M&M.

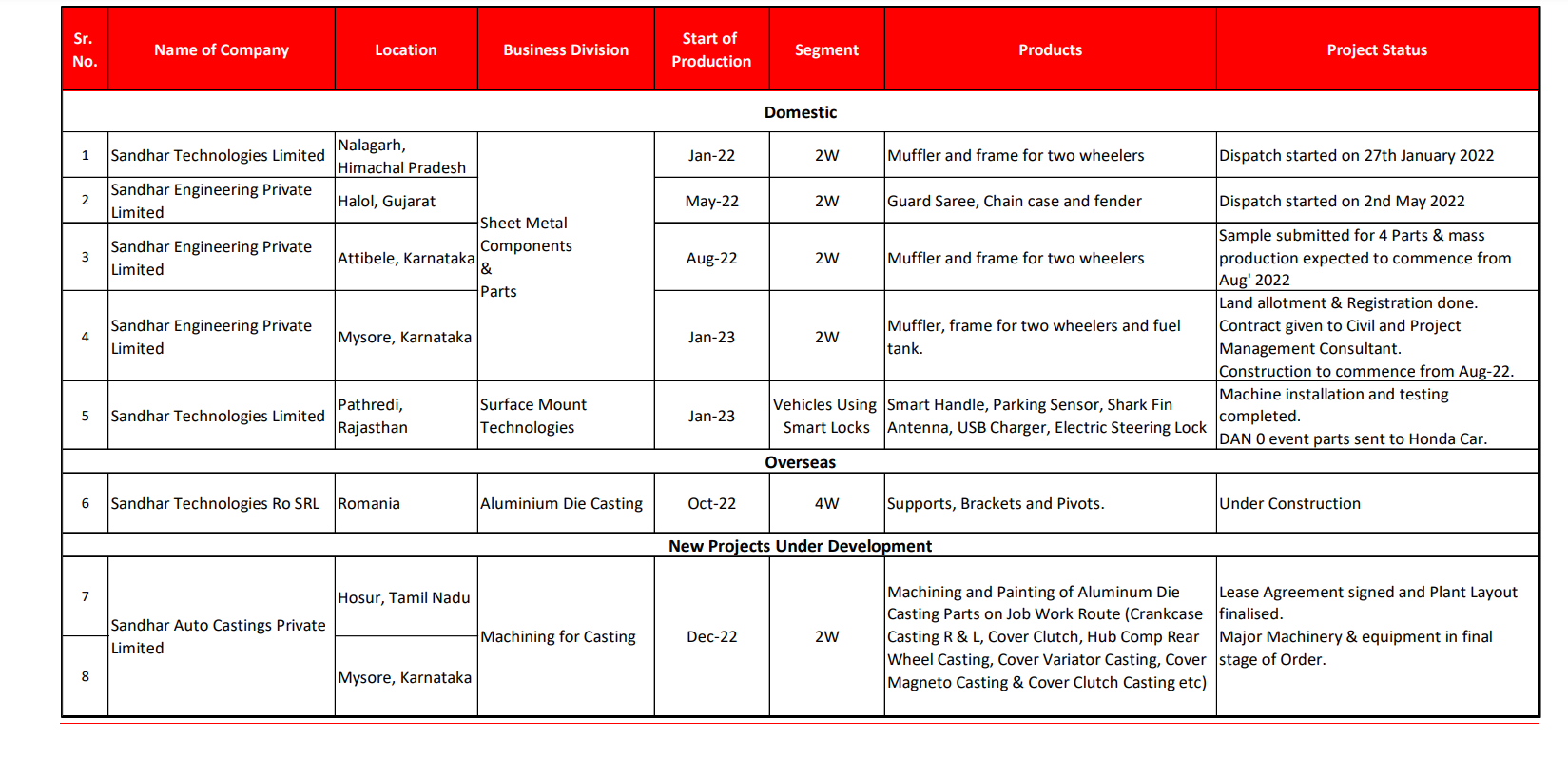

A few projects have been postponed. Prev qrtr vs Q1 FY23.

Overall still bullish over 2 years but RM continues to drag Sandhar. Waiting for mgmt commentary.

Disc - invested. Position sizing here.

Technically setting up decently, relative underperformance to auto index is shown. Important resistance at 265 or so. Higher low has been taken which is good.

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (04-08-2022)

Thank you @kalpesh4430 for introducing us to Satia and doing a lot of leg work. I bought around the 85-90 mark last year over a period of time. I was blown away by

- The management guidance about EBITDA last year

- Their projections from capacity expansion (esp their new premium copy paper)

- What I saw was their uniqueness about Zume/paper cutlery and premium positioning and their plan to add new cutlery machines as demand starts to explode

- This almost waste (wheat straw) raw material which farmers were burning, the mgmt view atleast what I understood was that the farmers were happy not to burn their husk as Satia was taking it away for them.

- Their positioning as though atleast a major portion of their raw material is cheap and a given.

When (3) above failed I started to question my thesis as this is a cyclical (whatever said, we should not confuse it with a more durable longer cycle business like HUL or Marico). I sold everything gradually between 110-120 after Q4 results. No holding now.

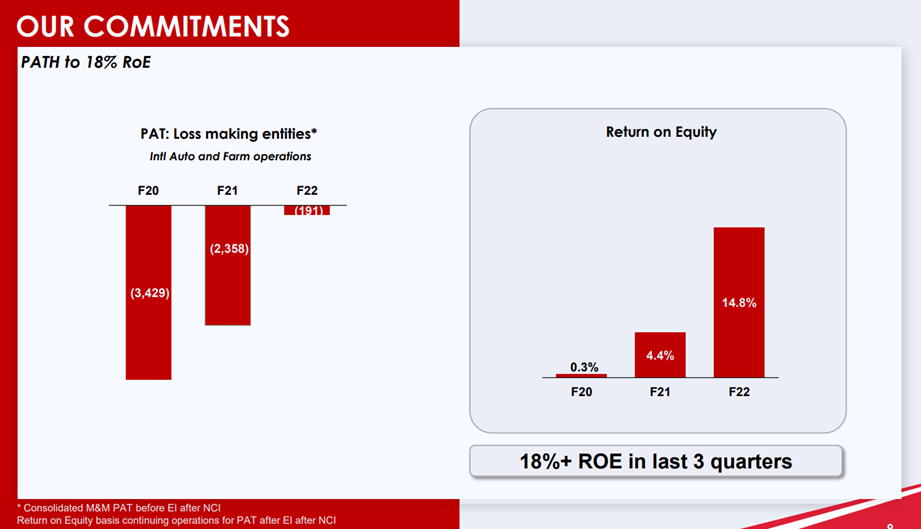

Mahindra & Mahindra Ltd. – a federation! (04-08-2022)

Sowing Seeds For Success Bears Fruit for Future

Recently Mahindra & Mahindra has rallied quite a bit due to its recent successful launches such as Scorpio- N and XUV 700.But apart from these successful launches there were few steps taken by the company in 2020

The company in 2020 had record losses from its subsidiaries due to which the company’s profits were deteriorating such that it almost fell by 97%. In order to solve these issues the company decided to reallocate its capital in 2020.The company set target of generating Return On Equity (ROE) of about 18% from 0.5% in FY20. The company took the following decision to achieve the targets

· Subsidiaries which will generate return on equity of 18% .M&M will stay invested in these subsidiaries.

· Subsidiaries with unclear path to profitability but are strategic. M&M will continue investments in such subsidiaries

· But Subsidiaries with unclear path to profitability. M&M will liquidate its investments.

As you can see in the image due to these decisions the losses from subsidiaries decreased and Return on equity kept increasing .

The Next target which the company is set is to achieve EPS growth of 15-20%

PDS Limited – A platform for entrepreneurs (04-08-2022)

78 bps improvement in gross margin

73cr EBITDA, 113% improvement, 102 bps improvement

ESOP charge 7 cr vs 2 cr y-o-y

12 crore investment in new business – expensed from P&L

Sourcing clocked 42% growth, 60cr EBIT, RoCE 42%

Manufacturing continues to be profitable (1.6% PAT margin)

Net Debt 77 crore, NWC increased from 2 days to 3 days

Will continue to focus on monetising non-core assets

Continue to focus on increasing US focus

China + 1 helping as people looking beyond China/Vietnam-Hong Kong relationship. Movement to sourcing from Bangladesh/Sri Lanka is helping PDS (one of the biggest reason is governance standard trust in PDS) fill up this vacuum. Vietnam also we are trying, we are late to the party, but doing not bad.

Whenever recession happens, we double in size as we help both retailers (one stop shop design free delivery) and factories (working capital + orders).

We have business, now with softening cotton and freight as well as currency depreciation, will see margin improvement.

80-90% budget is booked – strong orderbook – confident to meet guidance – cautious because of geopolitical issues

Seasonality of Q4 strongest – so QoQ not relevant

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (04-08-2022)

why would someone continue holding satia compared to a company like JK paper? - My thesis for the same was that Satia is 1/6th the size of JK - thus has a headroom for growth as well as the fact that Satia was getting into the cutlery segment in which the company had initially guided that EBITDA would be 40% ++. However now it seems that the cutlery business is on an idefinite hold and Satia is not able to maintain margins like JK.

Another thing to take into account is the boom in paper prices which is cyclical and currently, we are pretty much in the uptrend of the cycle. If Satia is not able to maintain margins right now - how will it do well when paper prices eventually come down

Even interms of valuation JK is cheaper than satia still.

Praj Industries (04-08-2022)

Average to poor results by Praj. 200bps decline in EBITDA QoQ due to gross margin slippage. Praj continues to be overvalued in my opinion. Narrative stronger than execution.

Tanla Platforms ~ Leading player in the fast-growing CPaaS market (04-08-2022)

New dividend policy and insider trading policies announced - https://www.bseindia.com/xml-data/corpfiling/AttachLive/05e8a194-0ea5-44fa-8aa6-abd10ee36c18.pdf

Dividend policy - https://www.tanla.com/media/images/Policies/DividendDistributionPolicy.pdf

Around 30% of consolidated net profit to be distributed each year as dividend. This is a good move, there was a concern regarding cash accumulating on the b/s without any acquisition plans. Returning the cash to shareholders according to this policy is a progressive move.

Insider Trading - https://www.tanla.com/media/images/Policies/Code_for_Insider_Trading_and_Fair_Disclosure.pdf

Praj Industries (04-08-2022)

Of course it will help Praj. Adani & RIL will setup plants with the help of Praj.