Artemis extended the healthcare services to New Delhi now. Artemis Lite, a multi-speciality hospital, offering high-end and personalized multi-specialty care. The hospital has 40+ beds including two operation theatres, 9-bed ICU, 5-bed day-care chemo suite, 4-bed NICU, labour delivery rooms and multi-specialty wards.

Posts in category Value Pickr

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (03-08-2022)

Exactly! For all the spiel around backward integration and captive power and proximity to raw material, the PAT margin disappointed me. I was expecting it to be ~10%.

Disc.: invested

CDSL – Stock for our children (03-08-2022)

Management was not able to properly answer 10 crore surprise bonus to employees. This could have been better handled. My personal opinion.

CDSL – Stock for our children (03-08-2022)

One more business income:

Q: So other than GIFT city so any update on other newer businesses what we are working on.

Nehal Vora: There is a gold spot exchange in the local market also which the circular has been issued so CDSL is very much a part of that entire ecosystem

IDFC First Bank Limited (03-08-2022)

Agree, that’s where every bank would want to be over time. Which is why cross selling payments, cards, wealth management and other services come handy, these lock in customers into regular usage and build in switching costs that prevent customers from moving to another bank.

All this takes time, normally takes 2-3 years for a branch to turn in operating profits and around 5+ years for the book to start contributing meaningfully to profits. But once a threshold is reached, profitability is non linear due to a confluence of factors since cost escalation does not keep pace.

Which is why comparing per branch revenue, CASA and profitability with a leading bank is not fair. Even within these large banks, their seasoned branches subsidize the lower throughput from semi urban and upcoming branches. A bank with 50% of the branches opened in the past 3 years will have high operating cost until it hits a threshold size on assets and fee income. But once it hits, operating leverage kicks and spikes the return efficiency rather quickly so long as provisions don’t spike too.

The key is to survive for a long period without credit events that can damage the asset quality significantly.

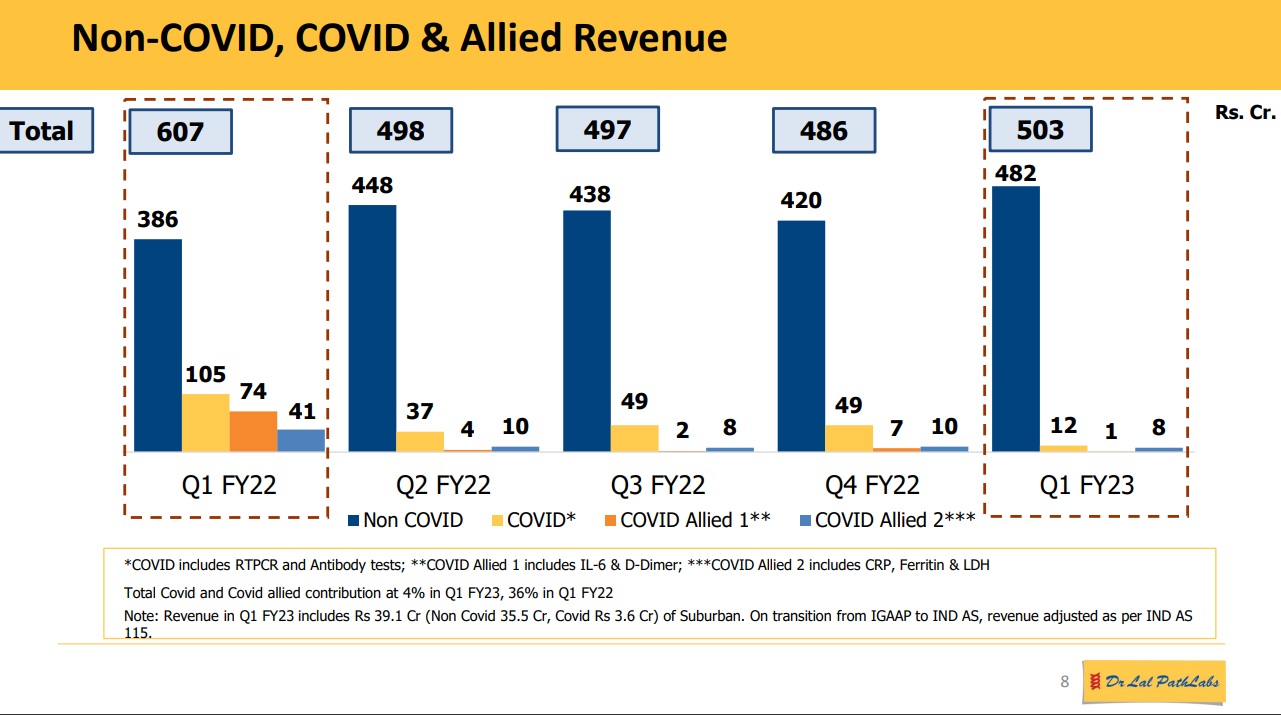

Thyrocare : Debt free Asset Light Healthcare Play (03-08-2022)

Non covid revenues increased both QoQ and YoY for both Lalpath and Thyrocare

Redington India : Strong Performance history, re-rating candidate (03-08-2022)

Q1FY23 Result - Highlights

- To integrate all logistics entities as One ProConnect, the Automated Distribution

Centres in Chennai and Kolkata will be transferred to ProConnect Supply Chain

Solutions Limited for 90 Crs. This business unit generated 4.25 Crs in income during FY22. - Even though on a standalone basis, the finance costs went up substantially, on a consolidated basis it has only increased slightly. Similar to the standalone entity, the group’s employee benefit expenses have gone up but other expenses have come down.

- SISA segment is more efficient (better ROA, ROCE -50% and ROE - 24%) than ROW (ROCE - 36% and ROE -19%).

- During the quarter, Redserv Global Solutions Limited (“RGS”) acquired Redserv Business Solutions Private Limited (“RBS”). Prior to this transaction, RBS was a wholly owned subsidiary of Redington Gulf FZE (“RGF”).

- Due to high WC utilisation, FCF for Q1FY23 stood at -2316.7 Crs (-13.79 % FCF margin)

- Mobility segment’s share in the revenue pie grew YoY.

- WC days (YoY), SISA - from 19 to 20, ROW - from 18 to 36 and Global - from 18 to 28.

- Apple’s share in revenues grew from 28% in Q1FY22 to 31% in Q2FY23

Disclosure - Invested

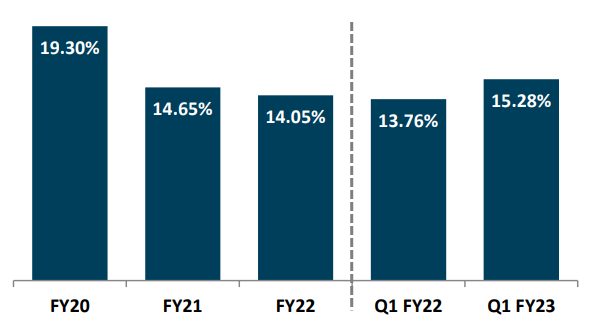

MAS Financial Services – High RoEs, Decent Growth (03-08-2022)

Q1FY23 Result:

Positives: Very big jump on PAT on QOQ as well as YOY basis, along with AUM growth.

QOQ ROE improvement to 15.28 vs 14.47 previous quarter vs 13.76 in Q1FY22. Co used to do 19% ROE precovid

Negatives: Though GNPA & NNPA ratios improved QOQ but absolute numbers have jumped at a faster rate than AUM growth. Total provisions more or less same.

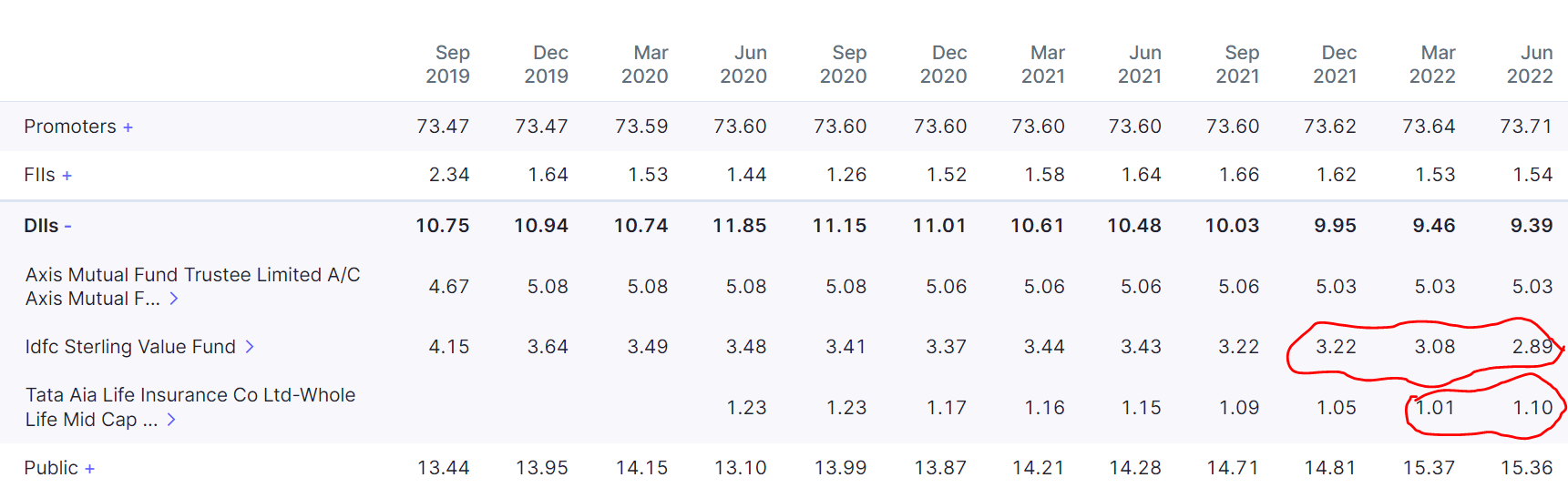

Valuation wise company is at PB ratio of 2.35 used to be available at PB ratio of 4 pre-covid. So the question boils down to can it touch pre-covid ROE while maintaining the asset quality? What gives comfort is when DIIs and retail fellows sold in recent correction the Promoter bought from open market.

Looks like once IDFC Sterling Value Fund stops selling the stock will go up. Till then it’ll consolidate maybe.

Disclosure: Invested and biased.

Inox Leisure- A faster running horse? (03-08-2022)

Satisfactory results by Inox.

-

Revenus at 589 this quarter vs 496 in Q1FY20.

-

OPM is 36% vs 30% Q1FY20. Largely due to lower employee cost. Employee cost is 20% lower than pre covid levels.

-

F&B revenue share is back to pre covid level.

-

Advertisement revenue did not. Advertisement share in revenue was 5% this quarter vs 9% in Q1FY20.

This should IMO increase as advertisers realise that the footfall is back to pre covid levels. This should further increase the OPM.

Anyone who has done valuations for Inox?

investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/038a72b1-0dfa-44c3-9cf7-4a385bcf61a7.pdf

disc: invested

Gujarat Themis Biosyn Ltd – Bulk Drugs growth momentum (03-08-2022)

It’s not a new discovery or a new trend. Only the modality of antibiotic resistance development is explained. Of how the bacteria adapts to memorise and subsequently kill rifamycin. That too a particular strain of bacteria.

Bacterial resistance is pretty common and it doesn’t put a drug out of use.