Some very interesting data here.

Hope it adds value.

Some very interesting data here.

Hope it adds value.

Concall Recording:

Important points from the ConCall:

Please consider some points I might have misunderstood or missed add if any.

Comments: Market reaction is obviously based on their past, surely over reacting, Industry itself growing by 25-30%, massive disruption, unless management goof up, massive opportunity lies a head, with nearly 1000 cr cash on Balance sheet, EV value @ Billion dollar now, let’s c how route mobile results will be, bullish on Cpaas industry.

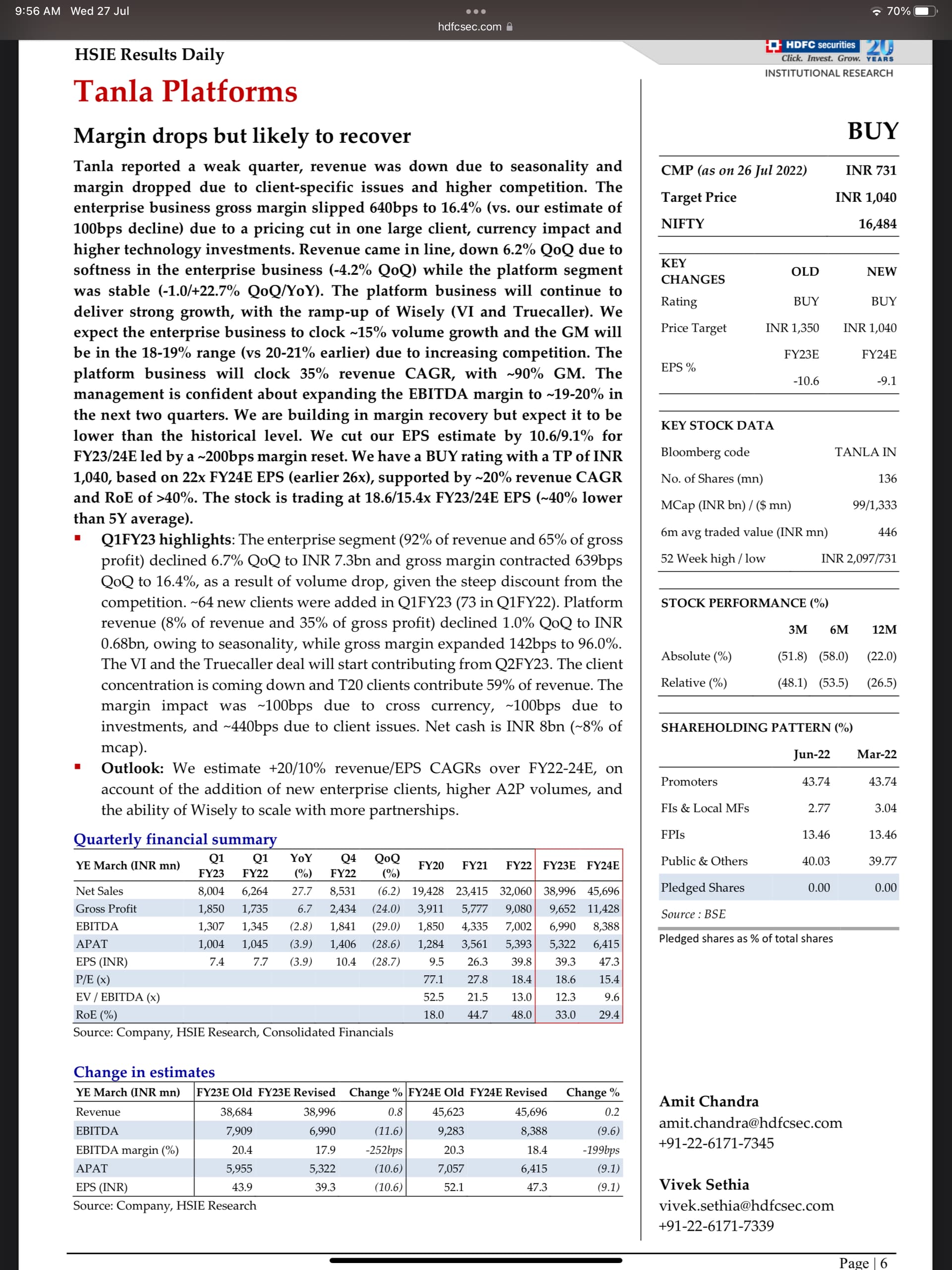

HDFC sec q1 update:

Disclosure: Invested.

If any member attended the AGM of Elantas Beck, kindly share notes. Thanks in advance.

Faze Three transactions (exports) from Mumbai port (data upto 3 July 2022). Looks like Q2 will be flattish to slight degrowth.

The headwinds due to inflation will be offset by revival of hospitality and hotel sector which is evident by record flight travel. Faze three supplies high end/luxury products- sheets, pillowcases, blankets, carpets, curtains, dining room tablecloths, cloth napkins to top hotels in US.

All thanks to @Chandragupta for gently nudging into asking difficult questions!

Apart from their core business, their entire communciation is something I would want to see last in any company. On one hand there is slower but more holistic growth that they could have targeted with their MCC and CCS market. There are exciting opportunities in the food industry for which they have communicated in the past and that it will grow faster than other verticals. But looks like they’re getting trapped by the short term or they are looking at some competition headwinds that we fail to realise.

The 1% royalty bit is something which makes the company a no go if they don’t back track and rectify it. Because of a lack of focus, the capital allocation can go for a toss. I wouldn’t want to buy an ethanol business via Sigachi. Nor would I want to buy a generic marketing one (can suck working capital, increase opex and takes a different kind of accumen to succeed). Topline isn’t that hard to increase per se. But will be difficult to do along with better or stable RoCE’s. That’s what their responsibility is but the soft signs are not very good.

I am trying to search the applications of Structure Directing Agents. As per company they are saying it is mainly used in vehicles and as Euro5/6 norms are effective and emissions need to be controlled.

a. Will this be used as a quoting material in Engine- If this is the case then it will be required in each and every vehicle which will have Euro5/6/7

b. Will this be used as agent in gasoline- If this is the case then it will need to be mixed in gasoline and will be in continuous demand

Can anybody throw some light on the applications?

Recent results

Hope it helps

dr.vikas

it was discussed in last concall I think. they have long term contracts, so they covered till sep.

Thanks for sharing the order. Nearly 2 years since this small, straightforward merger started. It’s worth reading the order to understand how death by compliance happens via Indian regulators / courts. When an inefficient system meets an inefficient management, shareholders are bound to get screwed.