krishnendu,

Please put up a disclosure on whether you hold shares in the company or not as is the normal practice at VP.

rgds

hitesh.

krishnendu,

Please put up a disclosure on whether you hold shares in the company or not as is the normal practice at VP.

rgds

hitesh.

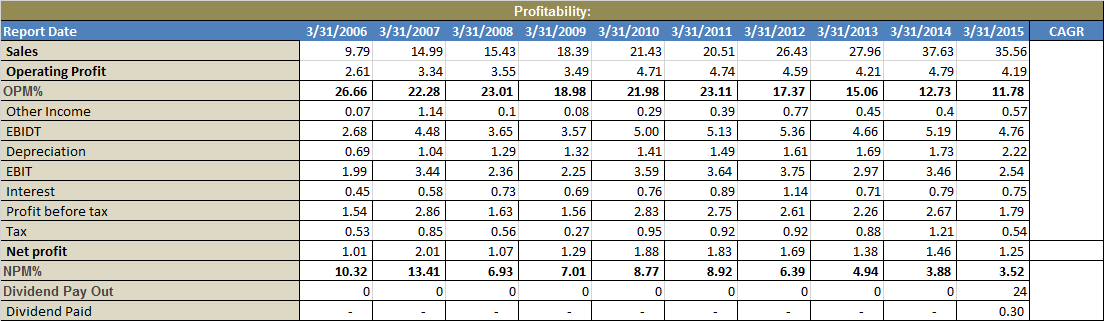

I have recently come accross a stock named Spenta International which is a textile stock operating on a relatively niche area like Socks. Below are the analysis I have made.

Sales Growth :-

As we can see the company is

making a sales growth CAGR of 16% over last 10 years hence this is a

commendable job and mostly inline with management expectation of making 20% CAGR

for coming 2-3 years but the considering individual years the growth they are

mostly fluctuating which is a cause of concern from strategic point of view of

the management.

Profit Margin :-

The profit margin both OPM and NPM

is not very satisfactory and mainly on the decreasing side hence it will

clearly show they do not have a bargaining power over it's consumer. Though

they have recently felt the urgency to create their own brand and increasing

export hence this might be a good step in increasing the Profit Margin but only

time will tell.

Value Creation :-

Over the years it is not well

known for creating any value for the share holder but this year it really does

it also from above you can see they have started to giving dividend so the

focus has changed and could have been a very good value investment opportunity.

Tax Payment :-

Tax payment is at per with corporate

tax [30-34%]rate hence not a problem with that but there is a ongoing dispute

with the IT of 48Laks.

Interest Coverage :-

Interest coverage is 5-6% always

hence a very good cover they have on their debt.

Debt :-

Debt is mostly very low and they

have have significantly reduce it in last three years also DE ration is under

control of 0.14-0.16 level.

Current Ratio :-

Current ratio is good hence we can

conclude there is ample amount of liquidity in the business.

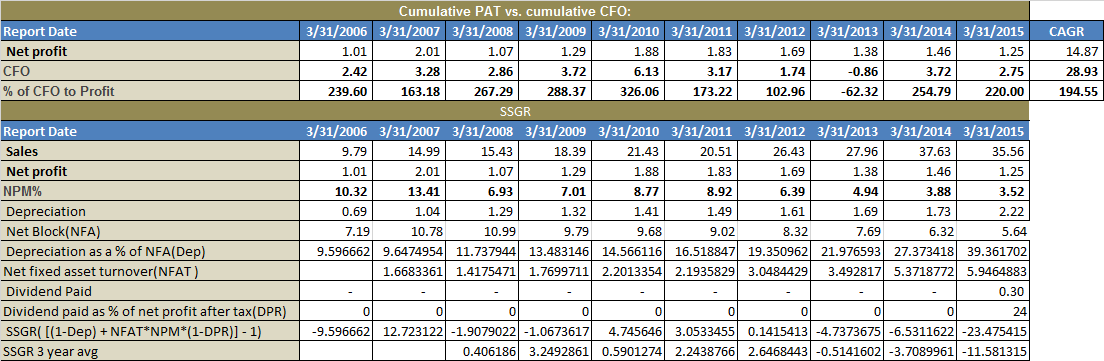

Cash Flow :-

Cash flow is really good which is a

commendable job by the management and show there conservative mentality also

collection of cash remain stable and consistent.

Self Sustainable Growth Rate :-

This is the parameter by which we

can judge weather a company is able to survive in future from it's internal

operation without a much requirement of cash inflow into the business.

Generally an average of 30-40% SSGR is good and stable.

The company does not have a good

track record of SSGR and mostly on the -ve side hence the future capital

requirement for the company is on the card if they will plan for expansion. As

we have earlier discussed that margin has suffered for the company so this is a

prime reason for -ve SSGR coupled with high depreciation rate of it's asset

which means they are in a requirement of continuous replacement of their

asset and also they have started paying dividend from this year which is

a good sign for the shareholder but will cost the business. So if the company

wants expand capacity or global footprint they will be requiring cash inflow

outside of their internal business operation though the CFO and free cash flow

is good and the company have ample cash in hand but this will again affect the

Dividend payout plan of the company. So the way I see it if they will be able

to increase Profit Margin this ratio will automatically improve and might not

be a cause of concern.

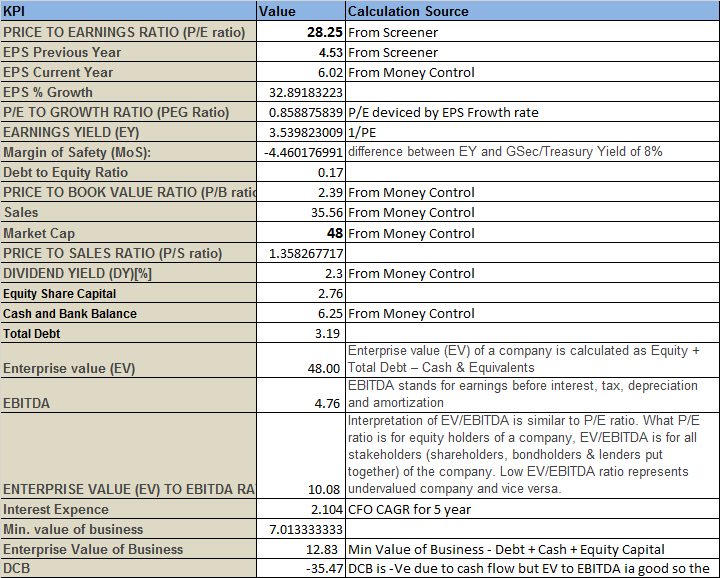

Valuation :-

Before taking an investment decision

we have to check couple of point :-

PE is at 28 hence on the higher

side and we have no margin of safety.

PEG stands at 0.9 i.e. under one

which shows there is a ample amount of growth left as the market cap is only

48Cr.

PB ratio is at 2.8 and PS ratio

is at 1.3 which are really good investment rationale.

EV to EBITDA ratio is at 10.8

hence a good bargain.

DCB is -ve and mainly due to same

reason for SSGR though here we are interested in CFO instead of PAT but as the

company is good at collecting cash so both are having the same explanation. We

have to have a Hawk eye on NPM and Sales CAGR.

Any help in this stock will be very helpful for me as I am relatively new in this domain. So if anybody has any information please share your view in this stock.

many thanks,

Krishnendu

Dear Sandeep,

Thanks for your views. I had a talk on this with Mr. Govind Sharda. He told this pledge was made when company had corporate loan in its books. Now the loan is paid off this year. Company will very soon be releasing the pledged shares.

Dear Ragunathan,

Thanks for your views. Arvind and Nandan are totally different - in terms of their market and style.

Nandan is a mass market player - increasing its sales through market penetration whereas Arvind plays globally through differentiating its products. Indian domestic industry has bee growing at CAGR of 15-18% over several years. Global markets have been increasing at 3-5% CAGR only. Arvind is going to obviously face growth problems since the industry growth rate is in single digits. Moreover, Arvind has been from the very beginning concentrating on more than one items like knitting and has now entered into cosmetics also. Nandan is focussed purely into denim over years.

I am a CA and my firm had Arvind as its client. There is a huge difference between the mgmt of both the companies.

According to me lack of concentration on denim business, mgmt (weak corp governance) and overall global denim market impacted Arvind. Nandan seems to be far far better than Arvind. I might be wrong, and I respect your views. Just keeping my views on the table for a healthy discussion.

Hi Nikhil,

Thanks for your valuable comment. You are correct - company with a Mcap of 650cr and debt of 600Cr. But, what if we see this as a positive factor. Stock is undervalued and debt has been received at cheap levels. Nandan has never faced any problem from TUFS/Guj Govt. Lets forget the word debt here !!

Unfortunately, couldn't find any reasons why the stock has touched upper circuit today! Any pointers here?

I looked at this but look at this

http://hypebeast.com/2015/10/jeans-sales-declining-report-bloomberg

http://www.nbcnews.com/business/consumer/denim-real-danger-going-out-fashion-n176211

Denim is slowing and arvind has been indicating so in its conference calls. Anyone old enough will remember how arvind went bankrupt because of a denim crash in 2000. I am not so sure of a debt fuelled expansion right now.

As for polus global fund, can someone clarify which fund house it belongs to and whos' the fund manager - I searched on linkedin and google but cou;d not find - they have invested into ansal properties in india but that's all. I can't imagine that a fund would risk capital into warrants and risk the loss of a complete write-off without any shareholder rights. In an institution, it would be frowned upon.

And if the share market crashes, they can't even get out - there's no liquidity, no shareholding either.

Yes vivekbothra,

Your calculation is correct. Suven has raised these 200 crores last year thru QIP route only for this purpose. And most probably, considering the accounting policy they follow, they will charge it in PandL only in next two years. Say 100 crores per year. And surely profit will go down to that extent. That's how it normally works. If successful, it will give multifold gains, else again at normal profit of 125-150 crores from years thereafter.

But the best and most important part, which I liked the most is they raised capital for it and didn't go for debt route. They diluted some 10% capital for raising 200 crore, so effectively if the project fails, we all shareholders will lose 10% of our value. Had they taken debt, there would have been burden repay the same with interest and that could have spoilt balance sheet structure. In event of success, it will be multi fold profits and again we will be parting 10% of that profit to QIP shareholders. But that's ok. Right??

Happy investing.

Disclosure - Invested from level of Rs. 30 and with price appreciation, its nearly 30% of my portfolio.

Wont sell single share till final outcome of SUVN-502.

Suven begins phase-2 trials for Alzheimer’s in US, See management interview here

Also, listening to last concall - Picked up something interesting.

About 6 months back, Suven created a subsidiary in US by funding it with USD $25mn. The objective of subsidiary is to take their in house molecules through advanced phases and work on out licensing opportunities.In the last call the mangement clarified that the whole USD $ 25 mn would be used for Suvn 502 their lead molecule and this $25 mn would be spent in next two FY (16 and 17)

Interesting bit is whatever they are spending in US out of this USD 25 mn, is currently not charged to PL as Suven is reporting standalone results.

What does that mean ?

When FY16 consolidated results are reported approximately USD $12.5 mn would come as charge in PL from US subsidiary, as management is expecting about USD $15 - 16 mn from standalone numbers there final net figure could go down to as low as USD $1 - 2 mn.

How will stock market react ? Only time will tell

PS - I could be completely wrong, if Suven’s capitalises this cost

Disc - I remain invested, About 5% of Current Portfolio no transaction in last 30 days

In my opinion its a bit expensive on valuation. Listed player like Apollo Hospitals is available at cheaper valuation IMHO.