wow. end product has come out nice & thanks for sharing it so freely!

you make the boring subject of investing sound so interesting.

is this the culminating work of your year long hibernation or can we expect more interesting things

thanks, raghav

wow. end product has come out nice & thanks for sharing it so freely!

you make the boring subject of investing sound so interesting.

is this the culminating work of your year long hibernation or can we expect more interesting things

thanks, raghav

Relax,Any Equity Share transaction done through stock exchange will attract STT. So in LTCG no tax & in STCG 15 percent.

Repco, in total has 47 branches in tamilnadu out of which 8 are in chennai.

Interesting thing is that most of the cities that repco is present it has only 1 branch or max 2. With having 8 branches in chennai, I feel that it is a significant market for repco.

Also, it is the middle and lower income group which will feel the pain of floods to whom repco caters. So I think this quarter will be ok on npa front but, next quarter is going to have a significant spike.

I am expecting gnpa to go to 3.5-4% of fy16 loan book.

Disc- not invested but waiting on sidelines to enter

I think it is all about FII selling. Everyone knows that its NPA issues (if any) would prove to be temporary.

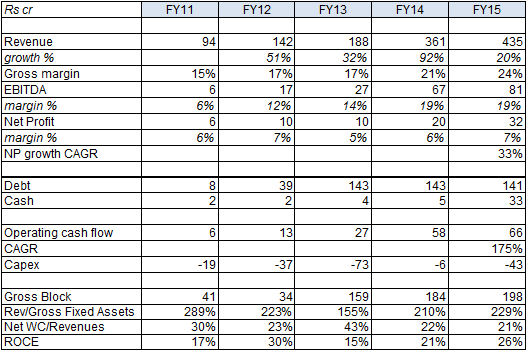

Bharat Rasayan Ltd

Disclosure: Not Invested

CMP Rs 987 (11 Dec 2015), MCap Rs 426 crore

FY15 Debt Rs 141 crore, of which 52% is working capital debt. Equity Rs 113 crore

Cash and bank balance Rs 33 crore.

Book Value Rs 266

Face value Rs 10

Promoter holding 75%, has been stable for past five quarters. Remaining held by retail and others. No shares are pledged.

Highlight of the company has been steadily improving financial performance. This has been driven by an increase in Gross Block as well as improving gross margins. The company has added significant economic value by growing while generating increasing ROCE.

About 25% of revenue comes from exports. The company has no forex debt. Raw material is the largest cost component comprising 69% of total costs. Thus fixed cost component is low at 10%.

Effective tax rate has been 33-34%. Dividend payout ratio used to be 10-15% but has dropped sharply to almost nil in last two years.

The company is rated AA-/A1+ by CARE Ratings. Market has rewarded the company by increasing both PBV and PE ratio, the latter increasing from 6.1 times in FY13. However, it seems the strong cash flows and future growth is still not priced in the stock (PE of 13 times), which trades cheap compared to its historical EBITDA growth.

Later posts will focus on company's products and quarterly analysis.

To be continued...

Another fear market has, is about the loss of income to lower-middle income group and hence rise of NPA's from that group. What do you think of that ? How is the un organised working class coping up with the situation ?

Seems like good time to enter in GOL and Castrol . My intention is to park my money here till I discover better opportunities

GOL

CMP- 480 approx

1. Has seen some correction and consolidation happening

2. Fast growing private player in lubricants industry with reasonable sales share

3. Improving margins scenarios because of fall in crude prices.

4.Dividend paying.

Cons -

2. INR devaluation and volatile exchange rates.

3.High Competition from PSU's and other private players like Castrol and Tide water

Factors that could add to improvement in margins and profitability further :-

1.Smart sourcing by company to decrease packaging costs.

2. Continued Growth in two wheelers and possible improvement in commercial vehicle segments

Discl - Looking to invest shortly. No holding as on date.

I live in Chennai and my feeling is Chennai flood would hardly have any impact on home loans.

We are good, the impact was no where close to what you felt watching on tv. I doubt my friends who are planning to buy homes soon would change their mind due to flood. The only thing I think can happen is the residential plots which got affected by flood may see a drop in price of houses for upcoming projects but that too is a very small number maybe around 10-15% of the overall construction work going on in the city. Unlike Eicher Motors where production was hampered here I don't think any permanent loss is incurred by home loan sector except for suspicion in the minds of buyers which all areas to avoid for buying homes.

I am not a CA so can not comment with authority, but I myself apply LTCG and STCG on shares purchased in rights and IPOs. In both the cases, we don't pay STT at the time of purchase. I hope, I have not been doing it wrongly till now.