(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Posts in category Value Pickr

Torrent Pharma Ltd (20-11-2015)

Rudra,

Its difficult to gauge what markets think in such a range bound markets. But usually once a price threshold is crossed, most of the concerns are forgotten and the mood and appetite for the stock suddenly changes.

Regarding acquisition, it might take a while for the company to narrow down a company which suits its purpose.

I feel even without acquisition, co seems on track.

MPS Ltd (20-11-2015)

Names masked as I am not sure if those ppl will like it . these are running notes - the reason why I keep it that way is to avoid my own biases - if I get the stock cal wrong, I can go back and interprept them another way and figure out what went wrong with my hypothesis.

I have some interpretations but will wait for inputs from everyone first. None of these guys have biases against or towards MPS and consequently treat these as facts to a large extent.

Inputs from a VP - biz development of a much smaller PBO (publishign services BPO)

Positioning as a full service content solutions provider is

key rather than an outsourced vendor. MPS scores well there.

Aptara – focussing on other industries such as BFSI, Pharma,

HItech and so on – BFSI – for eg., xbrl filing

Spi global is one of the larger players and they hvae the best platform and sales team

Pricing has been slashed –per page over the last few years. so key is to achieve efficiencies through volumes by doing more work processes with the same client.

MPS has strong focus on cost optimization with low value

added work being outsourced to smaller vendors. Also they had acquired a full

service company in the US

A large publisher typically works with multiple vendors like

MPS, aptara

Most of revenues comes from existing customers or large

publishers – slow cycle to get a new customer.

Publisher’s market is quite challenged – not easy to get

traction – companies look at every cost saved.

Only certain companies have scrapped projects and focusing

on optimizing their digital strategy. Challlenges like open source content,

funding and book rentals are putting pressure on these publishers Companies

have stopped producing content itself as things like book rentals, crowdsourced

content are hanging industry dynamics quite a bit

I was referring to this initiative

Market size is about $ 1 Bn –not growing - may be 2-3 %; 60% - of the work

comes to india – Philippines is next; then you have third world European

countries – like Romania, bosnia – India is the largest and won't go away for a long tme

e-learning is challenged in terms of profitability as publishers themselves are struggling to make money there.

Inputs from an ex-employee of MPS

Publishers are very conservative –

Marketing in these organizations are not very strong – very

technocrat driven.

Want to push down prices ever year;

Very labour intensive/skill intensive environment

Manual intervention needs to be brought down – figuring out

a way to take care of the changes in work flow can be an efficiency driver. its purely a function of how you can increaes billing per resource through intelligent technology intervention - so its a good CTO who differentiates one guy from another. MPS is improving but still behind SPI

Inputs from a senior guy in a large competitor

MPS Platform – overhyped - too little too late

Services – content – reinvent the content

Tap the content earlier to increase deal size form a client

For eg:

-

Author handling

Editor services

Pre-press

Post press:

Conversion

Re-purposing

Database enrichment

Content enrichment – adding photos

without these squeeze-ins, additional revenue growth is going to be difficult.

Historical P/E ratios (20-11-2015)

Equitymaster has a graph that does this for the last three years at least.

My two cents - those graphs don't mean much to find whether it is worth investing. Discounting all future cash flows to today and comparing with price - that's the real value identifier.

Duke Offshore – Hidden Gem? (20-11-2015)

I am not sure about monsoon story. Monsoon was week this year. So, why this affected more this year. As soon as qtr ended, they got the job in Oct!

How, do you feel about 6 cr reserve? Is that enough for new vessal! How much debt it need to take if not?

Thanks.

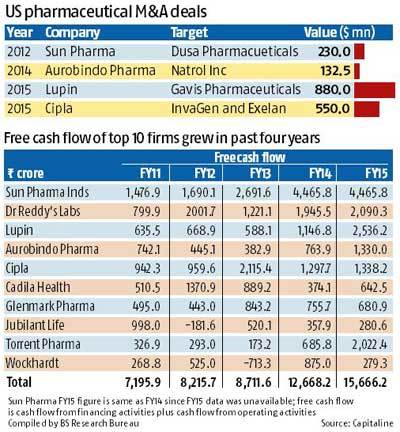

Torrent Pharma Ltd (20-11-2015)

Thanks Hitesh bhai.

I think the key trigger market is waiting for is some US based acquisition from Torrent. Given that they did not repatriate any cash from bumper US sales, and maintaining standalone debt indicates that management is keen on acquisitions.

Also, any inorganic growth would fill up the void from one off abilify sales in FY16. After Cipla and Lupin, Torrent might be next in line.

Historical P/E ratios (20-11-2015)

I am also interested to know this

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (20-11-2015)

According to Assocham study sugar prices in india is likely to firm up from summer of 2016.

Assocham press release about sugar study. Also as per recent concall of EID Parry, bounce in sugar prices from recent low of around 11 cent / lb to 15 cent / lb is technical in nature as most global projections estimates deficit of around 2-3 million tonne for consumption of around 182 million tonne for year 2016. However projection for 2017 is more supportive of global sugar prices. Also US FAO project that sugar prices can touch 18-19 cent / lb based on fundamental factor by 2017 which can be fair value of sugar considering expected demand supply scenarios. However from 2018 again some surplus is possible. All bounce back in commodity prices start with bit skepticism but gain ground based on future events playing out. However with severe deficit of monsoon in 2015 usually shock in sugar cane supply mostly surprises in downside and expectation of sugar prices touching 40-45 range sometimes in next 2 years in indian market cannot be rules out as agricultural product prices in india moves up very sharply in short duration. Also logically it does not make sense that in a country where hardly any vegetables or food staples available below Rs 40 only sugar is available below Rs 30 which is more difficult to produce and consumes more time , money and efforts in producing 1 kg of sugar than any other crop based food items.

Forensics and the art of triangulation (20-11-2015)

Have been on and off on value pickr. Find attached a report by ambit - which I think is quite good on forensic accounting.

I will also share a report by ACFE in the next post as the file size is too big to be posted in one post.

Avanti Feeds (20-11-2015)

Will these series of cyclones on the east coast impact production ? @hitesh2710 - if you could ask your contact on it pls and about general trends in shrimp pricing and volumes.