TORNTPHARM - Torrent Pharma’s new Plant at Dahej Commences operations https://t.co/9R64kDb0Gs

Posts in category Value Pickr

Shah portfolio check (05-11-2015)

Sorry for the delayed response.

Based on my assumption of 12-14% growth over the next 10 years the value may lie somewhere between 300 ~ 325. But I may completely off on my calculations since I haven't tracked this in depth.

Good luck on your future investments.

Kolte Patil Developers (05-11-2015)

one thing that caught my attention is that the Mcap of 1300 cr is less than the inventory cost of 1467 cr on books ( which accounts for ~70% of total assets) .

Automated Stock Analyzer (05-11-2015)

The latest version now computes Piotroski score for last 9 FY.

Automated Stock Analysis with the Piotroski Score

MPS Ltd (05-11-2015)

Thanks for the detailed explanation. Definitely it helps me to understand MPS deeper. You and your team is doing a great job.

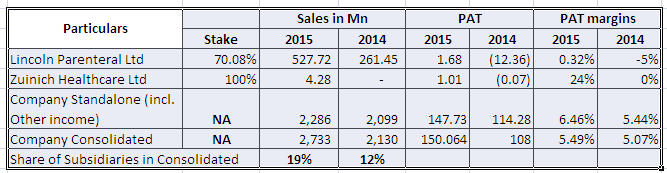

Lincoln Pharma … the next mid-cap pharma in the making …? (05-11-2015)

Company has two subsidiaries - Lincoln Parenteral Limited and Zuinich Healthcare Ltd. .

After analyzing the Financial Statements, I noted the following:-

Almost, 20% of sales has contributed nothing to the PAT margin. So, the subsidiary business is margin dilutive in nature.

Also, its hard to believe that a company generates 16 lacs of PAT on 68 crores of sales (it includes 16 crores to holding). I feel if that's a way of taking out cash from the business.

Lincoln pharma has given 4 crores as a deposit to Lincoln Parental Limited.

I observed 5 directors out of 7 from the promoter group.

None of them has a degree or mentioned experience in pharma field.

I've certain doubts on governance  .

.

Thanks.

Disc : Not invested. Under Radar.

MPS Ltd (05-11-2015)

I think I could not explain properly.

The Moolah lies in servicing the needs of the Academic/Educational STM (Science Technology Medical) Journal & Books Publishers.

I would think catering to Digital Publishing requirements of these customers is profitable - as The Digitally transformed product is only (one of) the Outputs. The main technology service that MPS like providers provides is what is called pre-publishing processes & workflows. From the Time an author submits a manuscript or file to the publisher to proof-read to editing to cross-referencing author reference for scholarly articles referred, to integrating bibliography to design to content rendering/transformation or print. The technology service provider game is to provide quick turnaround from author file to reader consumed final product - to be available for the Publisher's platform.

Catering to digital publishing requirements of non-STM segment like say an Amazon.com self publishing platform cannot be that profitable or for that matter say fiction or business or fashion books/magazines and the like.

Hope this time I could explain better

Manali Petro- Capacity Expansion (05-11-2015)

Only thing I will be concerned about it is - "This huge stockpile of cash is utilized properly and for the interest of all shareholder"

Any pointer towards promoter's background?

Manali Petro- Capacity Expansion (05-11-2015)

I have a query on their announcement dt Aug'15 "Pending receipt of approval of TNPCB for consent to operate at higher capacity, utilization of the plants has been restricted."

If their current capacity is under question for Pollution board how come a big capacity planned by the company will not face such risk in future?

Second in their May press release they had plan to invest Rs 100cr for capacity expansion

But in Sep they signed MOU of Rs 500cr investment which includes power plant as well

Discl - Exited fully in 2 phases...want to buy again post some clarity on capex