I am not sure about the private letter signed by the promoters with Multiples PE firm . At the outset I feel its not a great thing from a Corporate Governance view point. If members can throw some light will be great.

Posts in category Value Pickr

Motherson sumi : Recent opportunity to buy (02-11-2015)

I compared last five year margin with Amara Raja.

Motherson sumi:

9.30 5.49 5.83 7.88 7.49

Amara Raja:

14.62 14.36 13.84 16.19 16.66

Could someone help me in understanding why there is a huge difference ?

Eros international (02-11-2015)

Lets assume the company has done accounting mispracticed.

Lets for a minute think rationally. This year we had Bajrangi Bhaijaan accounting for 500 CR + business. Last year we had PK.

As per capita incomes rise from $1500 to about $2500, entertainement spends do increase. Look at indonesia and phillipines. India is not unique. Indians love entertainment. We love bollywood, cricket and weddings.

2011 Disney offered $454 Million for 49.56 % stake in UTV. So value the company at about $ 900 Million.

2011 the highest grossing movie was Ra One and Don 2 about 200+ CR each.

The absolute size of the market is going to grow exponentially with higher spendings.

Eros has some sort of a business model which allows it to be market leader in distribution and co-production.

Creating a brand name in entertainment world is not easy otherwise Ambanis, Birlas and Tatas would be the market leaders.

Yes the company is not a FCF generatring. Distribution companies have to advance acquire content and keep their content library fresh everytime to attract the viewers. Sometime down the line we will see EROS FCF generating but it might take some time.

With todays closing price you are getting the market leader in india movie industry for less than $500 Million.

Be fearfull when other are greedy and be greedy when others are fearfull!!!

Disclosure - Invested

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (02-11-2015)

Hi Thanveer,

Pls read the above thread carefully. If I were to summarize, Lactose India is largely a 3 part story (as of now)...

1) Significant capex for Kerry for Lactose (from 3500tpa to 11000tpa)..Demand is quite clear here as Kerry intends to put up even more capacity but Lactose India wants to stabilise the existing capex first.

2) Contract Manufacturer for Sanofi...small but stable cashflow business.

3) Lactulose capacity of 2400MT/Annum. Lactose India has done 30cr capex for putting up Lactulose. This is better margin business as it is 3rd derivation of Lactose. This business is very interesting (pls try reading up more on this). Impact of Lactulose will largely come in FY17/FY18. Current numbers are largely reflection of stabilization of Lactose for Kerry.

According to me...1&3 points are big game changer for the company. (Pls refer above thread for more)

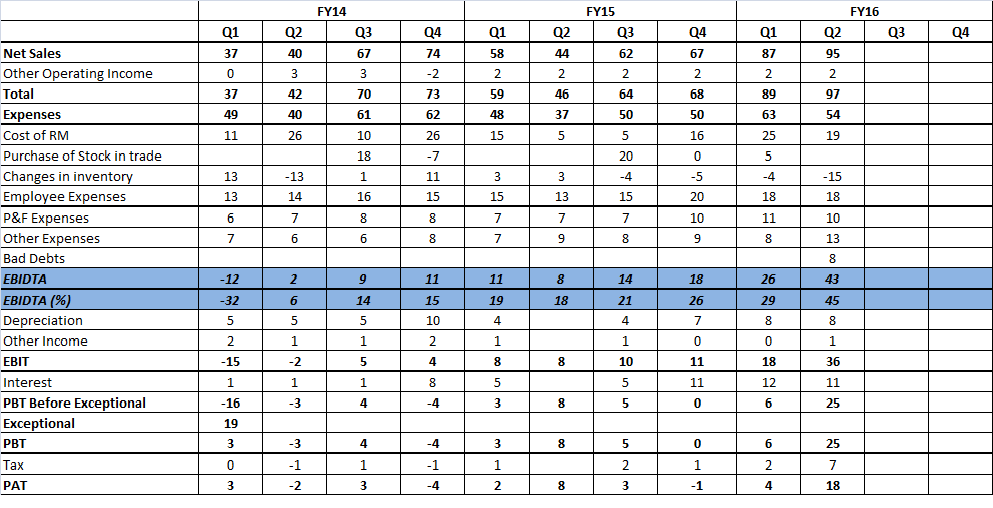

Yesterday's quarterly numbers were excellent and showing where company is headed.

1) Margins continue to expand very smartly (EBIDTA Margins at 45% compared to 29% in previous quarter and 18% same quarter last year). This is big improvement. Even after adjusting for inventory gains & bad debts. Margins are 37% odd.

2) I believe lactose will be very high ROE, ROCE story. Company's networth stands at Rs 19cr and if i were to annualise quarterly PAT...ROE can be as high as 38-40%. This is largely because of client funding the capex

3) Reduction in Long Term Debt by Rs 3cr was another pleasant surprise. LT now stands at Rs 26cr and ST at Rs 3.7cr.

Lactose India is a very unique play on Lactose/Lactulose with company at inflection point. Delta in numbers should continue to be big and provides extremely lucrative risk/reward. Potential upside can be really big.

Disc - Invested.

Hope that helps.

Thanks.

Tanla Solutions – a niche player in m-commerce space and a turn around story? (02-11-2015)

promoter holding has always been low in 35-36 region even 9 years ago. It has come down by 3 % over past 2 years which is definitely a red flag.

AIA Engineering Ltd (02-11-2015)

http://www.bseindia.com/xml-data/corpfiling/AttachLive/E8A9FE34_619E_4B15_8212_E68DE71236C8_132722.pdf

Q2 results just came out

Top line degrowth and disappointing netprofit as well

PS - fearful since I have a decent %

Shalibhadra Finance – Steady Growth NBFC (02-11-2015)

Gurjot

In this day and age, I do not think the BSE will sit and scan the annual report themselves. This must be a requirement upon the company to send a soft copy to the exchange. Either I am wrong or the MD does not know of this requirement. I still think these days all filings are generally electronic, sending the exchange a physical copy probably means it's still lying around somewhere unclaimed.

Regards

Tushaar

Tanla Solutions – a niche player in m-commerce space and a turn around story? (02-11-2015)

Any insights on why the promoter holding has been coming down?

Thanks.

Shalibhadra Finance – Steady Growth NBFC (02-11-2015)

Agreed.

But then the Annual Report was made well before the AGM on 29th Sept and it still hasn't been uploaded on the BSE website a month later.

So I don't know who is at fault here?

One thing is for sure - with each passing day the dividend payment issue might suddenly drag the CMP down. The only saving grace is there are very few individual minority shareholders.

Shalibhadra Finance – Steady Growth NBFC (02-11-2015)

Agreed.

But then the Annual Report was made well before the AGM on 29th Sept and it still hasn't been uploaded on the BSE website a month later.

So I don't know who is at fault here?

One thing is for sure - with each passing day the dividend payment issue might suddenly drag the CMP down. The only saving grace is there are very few individual minority shareholders.