Torrent is gaining significant market share in Detrol. According to bloomberg data, market share of torrent in detrol has reached 7% for the week ending Oct 10.

Torrent has maintained 10% market share in Abilify. Alembic has lost market share after entry of Apotex. alembic mkt share now stands at 4%.

Posts in category Value Pickr

Torrent Pharma Ltd (28-10-2015)

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (28-10-2015)

The market was fretting about weak domestic agri sales but as per mgmt. CSM revenue have been weak or postponed to H2. I have felt that they have certain level of discretion in recognizing CSM revenue. Overall a good show expected in H2.

Shalibhadra Finance – Steady Growth NBFC (28-10-2015)

Can anybody share when the Q2 results are out ??

My richdreamz portfolio – visit my portfolio to learn together! (28-10-2015)

Can you just share your views on PI industries.

Can one enter now around 645 - 670 will long term horizon ( 5 years )

Just asking for your views, nothing more than that.

Disc : not invested but planning to intiate the position

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (28-10-2015)

Hi @Nirav8,

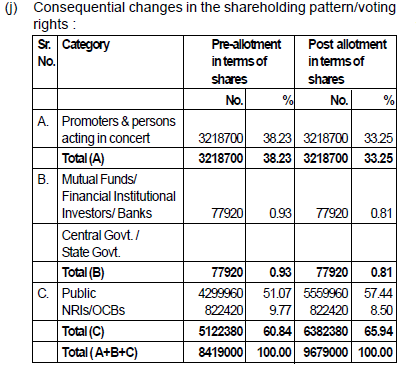

The allotment of 1260000 @27.50 is to non-promoters "Gyaneshwar Multitrade Private Limited", right ?

At least that's what companies share holding pattern seem to suggest. Would you know what could be rationale to allot shares to non-promoters with only 25% of 3.46 cr. payable at time of allotment and rest at time of conversion (within 18 months) ?

This dilution doesn't seem to have helped the promoters anyways (cash or increase in promoter holding), unless Gyaneshwar is also part of promoter group and company is giving wrong shareholding pattern.

My richdreamz portfolio – visit my portfolio to learn together! (28-10-2015)

Your clarity of thoughts on each business you own is wonderful. Love reading your updates in your portfolio thread. Can you briefly put your thoughts on Gruh results. Thanks

My richdreamz portfolio – visit my portfolio to learn together! (28-10-2015)

Your clarity of thoughts on each business you own is wonderful. Love reading your updates in your portfolio thread. Can you briefly put your thoughts on Gruh results. Thanks

Lincoln Pharma … the next mid-cap pharma in the making …? (28-10-2015)

Lincoln Pharmaceuticals Limited is an India-based holding company, which is engaged in the business of manufacturing, marketing and distribution of pharmaceutical products. The Company offers tablets, capsules, liquid injection, cream in tubes and dry power injection, among others. Its portfolio of products by segment name includes Aldase, Alphaline, Anzyme, Azilin, Ceftalin, Cepy, Dermolin, Pentalink, Progut, Protosol, Robilink, Soludine, Trixon and Vivian. The Company's plant is located at Trimul Estate, Khatraj, Tal Kalol, Gandhinagar, Gujarat. The Company has two subsidiaries, including Zullinc Healthcare Limited and Lincoln Parenteral Limited, which are engaged in the business of pharmaceutical products. The Company has presence in Bhutan, Bolivia, Botswana, Cameroon, Chile, Cambodia, Congo, Costa Rica, Ethiopia, Ghana, Hong Kong, Jamaica, Kenya, Malawi, Myanmar, Nepal, Nigeria, Panama, Peru, Philippines, Senegal, Sri Lanka, Thailand, Uganda, Vietnam and Zimbabwe

Last 10 years performance:

From Annual Report,

Industry Structure and Developments:

The Company is primarily engaged in the business of manufacturing, marketing and Exports of Pharmaceutical products. In India Pharmaceutical Industry’s continuously showing the growth rate of 20% to 22% as a industry as a whole. Looking to the Indian population, there are lot of opportunities for fast development of industries in the upcoming year also. In regulatory market the opportunities are quite open in generic products in the developing countries and lease developed country. There is lots of awareness in the R&D centres in the country’s and many new molecules as well as process are developed in the countries. Inspite of the stiff competition in the country and parallel marketing of generic products, growth of sales and turn over is assured. The financial year 2014 - 2015 has remained very excellent in terms of sales and growth of the company.

Opportunities:

There are number of opportunities available before the company in terms of products as well as sales territories in India where the growth rates are very potential. The Company is focusing on the brand image of the product as well as corporate branding in the markets. There are numbers of Pharma segments available before the company, for chronic medicines as well as non covered segments as present before the company. The company has wide opportunities for trading of products for developed countries and lease developed countires, business association in the field of manufacturing as well as marketing. The company is focusing on the new market area and other many countries by way of restructuring in the existing organization. The future of the Company and its products seems to be excellent in the coming year.

Outlook:

Company expects to increase the market shares in the exiting markets. The company expects to increase volume in the product portfolio. The company is also expects to introduce new products launched by the efforts of R&D centre. The company is expanding its marketing structure covering all geographical area. The company is focusing on the various divisions like Pharma, Teresa and Lord’s for the category of the product segment and concentrating on focused marketing by dedicated marketing teams. The Company continues to work on innovative strategies to broaden access to its medicines and strives to identify new growth opportunities to deliver strong performance.

Any views ?

Screener.in: The destination for Intelligent Screening & Reporting in India (28-10-2015)

Hi Ayush

Unable to log in Screener.in, the log in window pop up and will disappear, I am using Internet Explorer 9.

Regards

Alembic & Alembic Pharma (28-10-2015)

Yes I was surprised to get the first question. I thought everyone would anyway ask about Abilify, so asked some other questions.

Thanks for the comprehensive notes. I have few points to add

- Commercial prodn in Sikkim partially started. Full production in December15

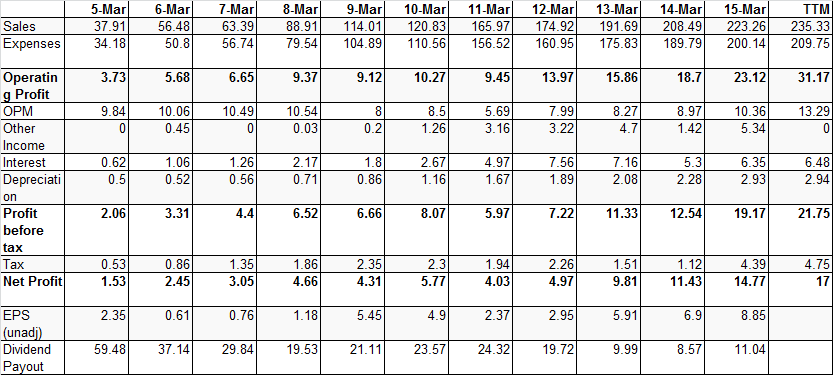

- Q2 results capture the Abilify sales and profits of May and June. So the actual full quarter numbers will come in Q3 but as pointed out, the company has lost almost half of its share and some price erosion has happened.

- Of the approved ANDAs, company is in process of launching some products. Some may not be launched because their market doesnt look good.

- Abilify ODT has a small market size of 15-20mn, but Alembic is the only player.

- Pristiq is under settlement. Management declined to comment on the launch or partner.

- Management clearly said that for R&D spend they dont have a percentage of sales number in mind. they invest based on the requirements. The absolute spend on R&D will continue to grow.

- Celebrex has been launched with a partner. Sales havent reflected in Q2

- API numbers show a good growth but at plant level, activities are flat. In some quarters, captive use is more. In this quarter they clubbed some external orders so the recognized sales for APIs show an increase.

- Long term guidance remains 30-35% growth in international generics sales, 15% growth in domestic sales and margin expansion from 20% to 23%.

I am happy to see the management walking the talk.

Discl. Invested