This is because Peak XV Partners sold 22% stake in a bulk deal in September. FIIs and DIIs picked up most of that stake. Peak XV Partners is classified under “Public” shareholders.

Posts in category All News

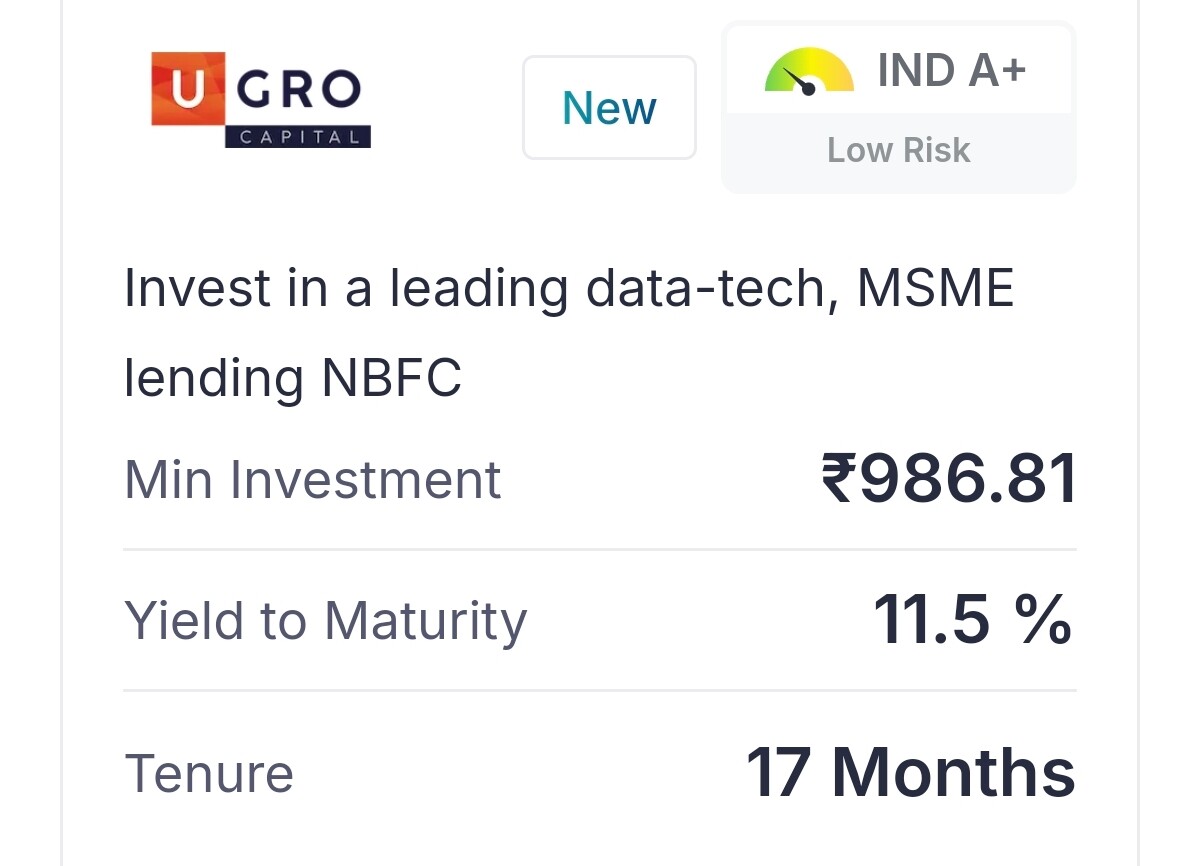

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (12-11-2024)

From a shareholder’s perspective, the significant increase in yield to 11.5% for this investment in U Gro Capital could indicate rising borrowing costs for the company. While this higher rate may help attract more retail investors in the short term, it raises questions about U Gro’s financial strategy and cost structure.

For shareholders, such high yields could mean either a squeeze on profit margins or a potential increase in the risk profile of the company’s lending book, especially if they pass on these costs to MSME borrowers who may already be under financial pressure. In the long term, sustained high yields might impact profitability, dividend payouts, or even share value if U Gro faces challenges in maintaining healthy growth without compromising asset quality.

Could anyone explain the reasons behind such a steep increase? It would be helpful to understand if this is specific to U Gro or an industry-wide phenomenon for MSME lenders. Knowing this could provide insights into the future trajectory and risks associated with investments in this sector.

Beta Drugs Limited (12-11-2024)

Some points from concall :

- company expects to grow overall at 25-30 percent for many years to come (over 3 yrs) and

CDMO will have a much bigger growth and expects exports to grow around ~50% YoY with

EBIDTA margin ~25% - operating profit margins back to 22% compared to 18% last time (last time platin prices were

high which caused margin impact) - Currently focus is on EU and in 2-3 yrs to expand in USA as well

Disc : Not invested , tracking.

**Any views on price range to enter supporting the valuations? **

Ahead of IPO, Zinka Logistics collects Rs 501 cr from anchor investors (12-11-2024)

Zinka Logistics Solutions Ltd, a digital platform for truck operators, on Tuesday mobilised over Rs 501 crore from anchor investors, a day before its initial share-sale opening for public subscription.

SBI Mutual Fund (MF), Bandhan MF, Invesco MF, ICICI Prudential Life Insurance Company, Nomura, Steadview Capital Mauritius, TIMF Holdings and Hornbill Orchid India Fund are among the anchor investors, according to a circular uploaded on BSE’s website.

As per the circular, Zinka Logistics allotted 1.84 crore equity shares to 26 funds at Rs 273 a piece, which is also the upper end of the price band. This aggregates the transaction size to Rs 501.33 crore.

The Rs 1,115 crore-IPO, will be available at a price range of Rs 259-273 apiece, for public subscription during November 13 to 18.

The IPO is a combination of a fresh issue of shares worth Rs 550 crore and an offer of sale (OFS) of up to 2.06 crore shares. The OFS by promoters and investor selling shareholders is valued at Rs 565 cr

KPI Green- Turning Sunshine Into Cashflows (12-11-2024)

But KPI Green also has EPC. Infact half of their order book is EPC (which is CPP) and the rest is IPP. You could say that KPI is more diversified but it definitely does EPC as well.

Zydus Lifesciences (Erstwhile: Cadila healthcare) (12-11-2024)

Zydus Lifesciences –

Q2 FY 25 results and concall highlights –

Revenues – 5237 vs 4368 cr, up 20 pc

EBITDA – 1461 vs 1146 cr, up 27 pc ( margins @ 27.9 vs 26.2 pc )

PAT – 911 vs 800 cr, up 14 pc ( due increased tax rate )

Geography wise sales breakup –

India formulations – 1456 cr, up 9 pc

India consumer wellness – 487 cr, up 12 pc

US formulations – 2416 vs 1864 cr, up 29 pc

International formulations – 538 vs 450 cr, up 19 pc

APIs – 119 vs 140 cr, down 15 pc

Others – 94 vs 34 cr, up 177 pc

Launched 12 new products in India in Q2. Out of these, 4 were first to mkt products

Share of chronic sales @ 42 pc vs 38 pc in FY 21

Consumer wellness business registered 8 pc volume growth

Zydus Wellness ( company’s subsidiary ) acquired – Naturell Pvt Ltd in Q2 ( for 390 cr ). It manufactures and sells Nutrition bars, protein cookies, protein chips and other health foods

Q2 capex @ 301 cr. Q1 capex spends were @ 302 cr

Cash on books @ 2590 cr

In India, 10 of company’s brands have sales > 100 cr. Another 21 brands have sales between 50-100 cr

Launched 4 new products in US in Q2. Filed 8 ANDAs and received 9 approvals ( including 3 tentative approvals )

Share of chronic sales @ 42 pc vs 38 pc in FY 21

Consumer wellness business registered 8 pc volume growth

Company acquired – Naturell Pvt Ltd in Q2. It manufactures and sells Nutrition bars, protein cookies, protein chips and other health foods

Q2 capex @ 301 cr. Q1 capex spends were @ 302 cr

Cash on books @ 2590 cr

In India, 10 of company’s brands have sales > 100 cr. Another 21 brands have sales between 50-100 cr

Launched 4 new products in US in Q2. Filed 8 ANDAs and received 9 approvals ( including 3 tentative approvals )

Entered into an exclusive licensing and supply agreement with Viwit Pharma for 02 – Gadolinium based MRI – contrast agents – to be supplied in the US mkts. These are injectables – used to increase the visibility of organs during MRI procedures. This is a niche but valuable drug. There r no generics for this drug currently in the mkt

Updates on Innovation –

Saroglitazar Magnesium – Recruited patients for phase 3 trials for the indication – Primary biliary cholangitis

Unsoflast – Completed phase 2 trials in India for the Indication – ALS ( Amyotrophic Lateral Sclerosis )

Desidustat – Initiated phase 2 trials in US for Sickle cell disease

Received WHO approval for their TCV vaccine – ZYVAC ( to prevent Typhoid )

Company has acquired 50 pc stake in Sterling Biotech for 550 cr. Currently setting up state of the art manufacturing facility to produce fermented animal free proteins. Also acquired sterling Bio’s API business that manufactures fermentation based APIs like – Lovastatin, Daunorubicin, Doxorubicin and Epirubicin

During the Qtr, 02 of company’s facilities were inspected by US FDA – Injectables facility at Jarod received a warning letter ( a key negative ), Ahmedabad SEZ facility successfully completed the inspection and received an EIR with a VAI status

Guiding for an R&D expense of 8 pc of topline for full FY 25 – a key positive ( IMO )

Maintaining high teens topline growth guidance with EBITDA margins > FY 24 margins for FY 25 ( likely to exceed their guidance )

Naturell Pvt ltd currently does an annual sales of 130 cr

Mirabegron sales in US continue to remain strong – which is why the gross margins are holding up > 70 pc despite Revlimid not contributing in Q2 ( Revlimid sales happen only in Q1 and Q4 )

Sales and pricing of Asacol are likely to get adversly affected wef Q3 { as the competitor (Teva) ramps up their product }. Zydus was the only generic for Asacol in the US mkt for quite some time now

Opportunities like – Palbociclib ( breast cancer drug ) and Riociguat ( for treatment of pulmonary arterial hypertension ) and Cabizantinib ( used to treat thyroid cancer ) generics should help them offset the loss of exclusivity on Revlimid ( to a large extent ) wef Jan 26. Company is also looking to file and launch a few more 505(b)(2) opportunities immediately. On both – Palbociclib and Riociguat – company is expected to get exclusivity for meaningful time period

Hopeful of getting a WHO approval for their MR ( measles and rubella ) Vaccine as well. Both these vaccines ( MR + TCV ) should bring in sizeable business for the company as UNICEF buys them in bulk every year ( to the tune of 8-10 cr doses ). Scale up should begin sometime in FY 26. Even if they get a fraction of this business – it can be very significant business for the company

Despite loss of exclusivity on Asacol, company is confident of growing their US business in FY 26 over FY 25

Company has won a US govt tender for supply of Sitagliptin for a 3 yr period starting next FY. This should be valuable business for the company. Company will also sell Sitagliptin in US through the 505(b)(2) route for FY 26 before it goes generic in FY 27

Company has a healthy pipeline of Transdermal and complex Injectable products to be launched in US – these should help them sustain the business momentum in the US mkt

Key things to watch out for in the Indian innovative portfolio of the company for the near future should be their mkt share in products like – Saroglitazar, Desidustat and the Biologics that the company is launching. Company’s mkt share – both in volumes and value for Ujvira ( Trastuzunab – for treatment of breast cancer ) is now higher than the innovator

Company aspires to take Saroglitazar and Desidustat to among top 50 products in IPM

If Saroglitazar is approved in US as per the expected timelines, company should be launching it in Q1 FY 28 or so

Disc: holding, biased, inclined to add more, not SEBI registered, not a buy/sell recommendation

Ranvir’s Portfolio (12-11-2024)

Zydus Lifesciences –

Q2 FY 25 results and concall highlights –

Revenues – 5237 vs 4368 cr, up 20 pc

EBITDA – 1461 vs 1146 cr, up 27 pc ( margins @ 27.9 vs 26.2 pc )

PAT – 911 vs 800 cr, up 14 pc ( due increased tax rate )

Geography wise sales breakup –

India formulations – 1456 cr, up 9 pc

India consumer wellness – 487 cr, up 12 pc

US formulations – 2416 vs 1864 cr, up 29 pc

International formulations – 538 vs 450 cr, up 19 pc

APIs – 119 vs 140 cr, down 15 pc

Others – 94 vs 34 cr, up 177 pc

Launched 12 new products in India in Q2. Out of these, 4 were first to mkt products

Share of chronic sales @ 42 pc vs 38 pc in FY 21

Consumer wellness business registered 8 pc volume growth

Zydus Wellness ( company’s subsidiary ) acquired – Naturell Pvt Ltd in Q2 ( for 390 cr ). It manufactures and sells Nutrition bars, protein cookies, protein chips and other health foods

Q2 capex @ 301 cr. Q1 capex spends were @ 302 cr

Cash on books @ 2590 cr

In India, 10 of company’s brands have sales > 100 cr. Another 21 brands have sales between 50-100 cr

Launched 4 new products in US in Q2. Filed 8 ANDAs and received 9 approvals ( including 3 tentative approvals )

Share of chronic sales @ 42 pc vs 38 pc in FY 21

Consumer wellness business registered 8 pc volume growth

Company acquired – Naturell Pvt Ltd in Q2. It manufactures and sells Nutrition bars, protein cookies, protein chips and other health foods

Q2 capex @ 301 cr. Q1 capex spends were @ 302 cr

Cash on books @ 2590 cr

In India, 10 of company’s brands have sales > 100 cr. Another 21 brands have sales between 50-100 cr

Launched 4 new products in US in Q2. Filed 8 ANDAs and received 9 approvals ( including 3 tentative approvals )

Entered into an exclusive licensing and supply agreement with Viwit Pharma for 02 – Gadolinium based MRI – contrast agents – to be supplied in the US mkts. These are injectables – used to increase the visibility of organs during MRI procedures. This is a niche but valuable drug. There r no generics for this drug currently in the mkt

Updates on Innovation –

Saroglitazar Magnesium – Recruited patients for phase 3 trials for the indication – Primary biliary cholangitis

Unsoflast – Completed phase 2 trials in India for the Indication – ALS ( Amyotrophic Lateral Sclerosis )

Desidustat – Initiated phase 2 trials in US for Sickle cell disease

Received WHO approval for their TCV vaccine – ZYVAC ( to prevent Typhoid )

Company has acquired 50 pc stake in Sterling Biotech for 550 cr. Currently setting up state of the art manufacturing facility to produce fermented animal free proteins. Also acquired sterling Bio’s API business that manufactures fermentation based APIs like – Lovastatin, Daunorubicin, Doxorubicin and Epirubicin

During the Qtr, 02 of company’s facilities were inspected by US FDA – Injectables facility at Jarod received a warning letter ( a key negative ), Ahmedabad SEZ facility successfully completed the inspection and received an EIR with a VAI status

Guiding for an R&D expense of 8 pc of topline for full FY 25 – a key positive ( IMO )

Maintaining high teens topline growth guidance with EBITDA margins > FY 24 margins for FY 25 ( likely to exceed their guidance )

Naturell Pvt ltd currently does an annual sales of 130 cr

Mirabegron sales in US continue to remain strong – which is why the gross margins are holding up > 70 pc despite Revlimid not contributing in Q2 ( Revlimid sales happen only in Q1 and Q4 )

Sales and pricing of Asacol are likely to get adversly affected wef Q3 { as the competitor (Teva) ramps up their product }. Zydus was the only generic for Asacol in the US mkt for quite some time now

Opportunities like – Palbociclib ( breast cancer drug ) and Riociguat ( for treatment of pulmonary arterial hypertension ) and Cabizantinib ( used to treat thyroid cancer ) generics should help them offset the loss of exclusivity on Revlimid ( to a large extent ) wef Jan 26. Company is also looking to file and launch a few more 505(b)(2) opportunities immediately. On both – Palbociclib and Riociguat – company is expected to get exclusivity for meaningful time period

Hopeful of getting a WHO approval for their MR ( measles and rubella ) Vaccine as well. Both these vaccines ( MR + TCV ) should bring in sizeable business for the company as UNICEF buys them in bulk every year ( to the tune of 8-10 cr doses ). Scale up should begin sometime in FY 26. Even if they get a fraction of this business – it can be very significant business for the company

Despite loss of exclusivity on Asacol, company is confident of growing their US business in FY 26 over FY 25

Company has won a US govt tender for supply of Sitagliptin for a 3 yr period starting next FY. This should be valuable business for the company. Company will also sell Sitagliptin in US through the 505(b)(2) route for FY 26 before it goes generic in FY 27

Company has a healthy pipeline of Transdermal and complex Injectable products to be launched in US – these should help them sustain the business momentum in the US mkt

Key things to watch out for in the Indian innovative portfolio of the company for the near future should be their mkt share in products like – Saroglitazar, Desidustat and the Biologics that the company is launching. Company’s mkt share – both in volumes and value for Ujvira ( Trastuzunab – for treatment of breast cancer ) is now higher than the innovator

Company aspires to take Saroglitazar and Desidustat to among top 50 products in IPM

If Saroglitazar is approved in US as per the expected timelines, company should be launching it in Q1 FY 28 or so

Disc: holding, biased, inclined to add more, not SEBI registered, not a buy/sell recommendation

Investors poorer by Rs 5.29 lakh cr as markets slump (12-11-2024)

A sharp fall in the equity market made investors poorer by Rs 5.29 lakh crore on Tuesday when the BSE benchmark Sensex tumbled over 800 points. A host of negative triggers — muted quarterly earnings, continuous foreign fund outflows and weak trends in Asian and European markets — dragged the benchmark indices lower. The BSE benchmark gauge tumbled 820.97 points or 1.03 per cent to settle at 78,675.18.