The company said other blades had a “manufacturing deviation” similar to a blade that shattered in July off the coast of Nantucket.

Sona Comstar BLW – Direct EV Play (23-10-2024)

SonaCom posted fair set of numbers in Q2 FY25. Key takeaways from the numbers.

- Total revenue for Q2 FY25 was INR 9,251 million, a 17% increase compared to Q2 FY24

- The light vehicle sales trend in Sonacom’s key markets (North America, India, and Europe) decreased by 2% in the same period.

- BEV revenue in Q2 FY25 was INR 3,172 million, a 53% increase compared to Q2 FY24

- The BEV segment contributes 36% to Sonacom’s total revenue

- Adjusted EBITDA margin for Q2 FY25 was 28.5%, compared to 28.3% in Q2 FY24

- Adjusted PAT margin for Q2 FY25 was 17.1%, compared to 16.3% in Q2 FY24.

- Secured 1 new program in Europe, 1 in Asia, and 14 in India during Q2 FY25

Other highlights/extracts from Inv. Presentation.

Revenue Growth: Total revenue for Q2 FY25 reached INR 9,251 million, reflecting a significant 17% year-on-year increase. This growth outpaced the overall light vehicle sales trend in Sonacom’s key markets (North America, India, and Europe), which experienced a 2% decline. This suggests that Sonacom is effectively capturing market share and expanding its presence.

BEV Revenue Surge: Notably, Sonacom’s Battery Electric Vehicle (BEV) segment witnessed remarkable growth. BEV revenue in Q2 FY25 reached INR 3,172 million, a substantial 53% increase compared to the same period last year. This highlights Sonacom’s successful strategic focus on the rapidly expanding EV market. The BEV segment now contributes a significant 36% to Sonacom’s total revenue, demonstrating its growing importance to the company’s overall performance.

Profitability: Despite various challenges like the UAW strike, Sonacom managed to maintain stable EBITDA margins. The adjusted EBITDA margin for Q2 FY25 was 28.5%, slightly higher than the 28.3% recorded in Q2 FY24. This consistent profitability underscores Sonacom’s operational efficiency and ability to manage costs effectively, even amid a dynamic market environment.

PAT Margin: Sonacom’s adjusted PAT margin for Q2 FY25 was 17.1% compared to 16.3% in Q2 FY24. This growth in PAT margin indicates the company’s ability to translate its topline growth into even stronger bottom-line performance.

New Programs and Customers: Sonacom has secured new programs across various regions in Q2 FY25, demonstrating its continued success in acquiring new business. The company added 1 new program in Europe, 1 in Asia, and 14 in India, further expanding its global reach.

Key Takeaways about Sonacom’s Railway Equipment Division (RED)

-

Market Leader and Pioneer: RED is the market leader in railway brake systems in India. It introduced manufacturing compressed air brake systems for railway applications for the first time in India, making it a pioneer in the industry.

-

Diversified Portfolio: RED possesses a diversified portfolio of products, with brake systems being the largest segment. Other products include couplers, suspension systems, electrical panels, HVAC systems, automatic plug door systems, friction and rubber products, and brake cylinders.

-

Historical Growth and Profitability: RED boasts an attractive financial track record characterized by high growth, profitability, and return metrics. Its revenue grew consistently from FY21 to Q1FY25, with EBIT margins ranging from 13.8% to 20.5% and ROCE exceeding 38% in recent years.

-

High Growth Potential: RED is poised for high growth, driven by the introduction of new products and the overall expansion of the railway sector. The division is strategically positioned to capitalize on the increasing demand for railway equipment in India and potentially other regions.

Summary

Q2 FY25 performance underscores its resilience and strategic positioning within the evolving automotive landscape. The company’s focus on high-growth segments like BEVs, coupled with its operational excellence, positions it well for continued success.

Disclaimer: Invested and Biased. Less than 7% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions.

HUL Q2 profit down 2.33%; separates ice cream biz (23-10-2024)

FMCG major Hindustan Unilever Ltd (HUL) on Wednesday reported a 2.33 per cent decline in consolidated net profit at Rs 2,595 crore for the second quarter ended in September 30, 2024 impacted by moderation in demand from the urban market. The company had logged a net profit of Rs 2,657 crore in the July-September quarter a year ago, HUL said in a regulatory filing. However, revenue from product sales was up 2.36 per cent at Rs 15,703 crore in the September quarter, from Rs 15,340 crore in the year-ago period, HUL which owns power brands such as Surf, Rin, Lux, Pond’s, Lifebuoy, Lakmé, Brooke Bond, Lipton and Horlicks said.

India’s diesel consumption likely to surpass 93 mt in FY25 (23-10-2024)

Both August and September this year have witnessed a fall in diesel usage

Aditya Birla Fashion and Retail Ltd (23-10-2024)

Absolutely. Hopefully things should fall into place ![]() I’ve held a bias but looking at the recent thread will have relook

I’ve held a bias but looking at the recent thread will have relook ![]()

Oriana Power – SME play on Renewable Energy (23-10-2024)

Does anyone know what happens to the RESCO model after few years when the prices of solar panels reduces drastically? The investment made by Oriana might be under pressure. Ofcourse the clients are bound to pay higher fees but it will be injustice and a mockery .

Wonder what’s the terms and conditions of breaking the contract.

Anyone having any idea on this?

Also, lot of positive news created but the stock is still not moving. Looks like some big party is offloading shares.

Navin Flourine International (23-10-2024)

Overall, fair set of topline growth in Q2 FY25, driven by the HPP and CDMO segments. While consolidated profit after tax slightly declined, (lower other income, higher depreciation, tax) the company maintains a positive outlook, backed by a strong order book, ongoing capacity expansion projects, and a strategic focus on key growth drivers.

Posting the summary note from the investor presentation here.

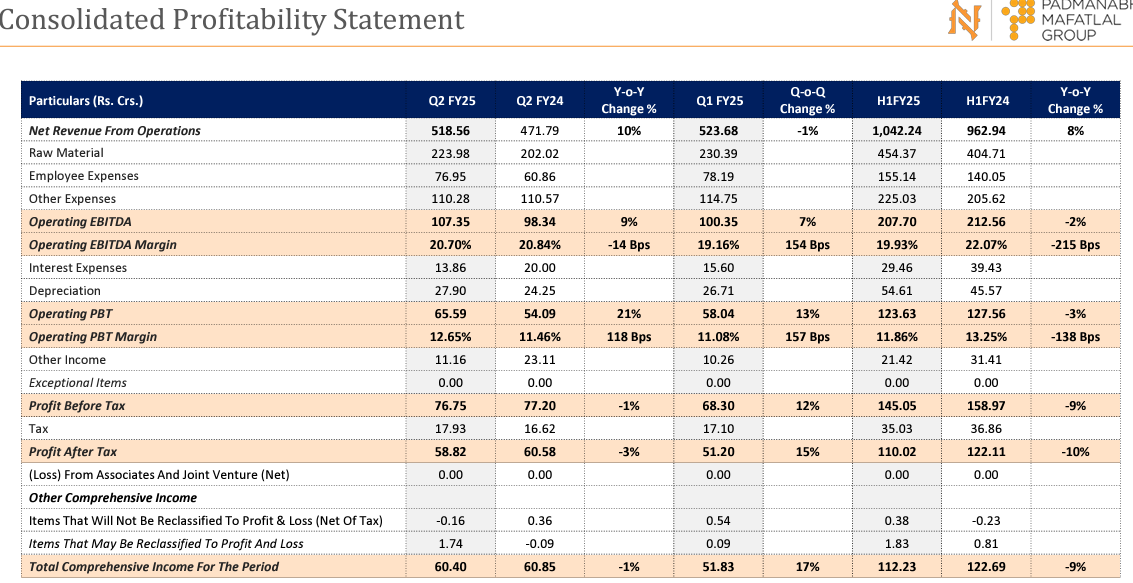

Navin Fluorine International Limited Q2 FY25 Performance Summary

Topline:

- Consolidated revenue from operations for Q2 FY25 was Rs. 518.56 crores, a 10% increase year-over-year (Y-o-Y).

- The Specialty CDMO segment saw a 10% Y-o-Y sales increase, reaching Rs. 518.6 crores.

- The HPP business vertical experienced a 23% Y-o-Y revenue growth, driven by increased R32 sales and better R22 realizations.

- Specialty Chemicals revenue decreased by 15% Y-o-Y due to cautious global demand and competitive pressure.

- The CDMO business vertical saw a 41% Y-o-Y revenue increase, driven by strategic actions including supplying a quantity for process performance qualification for a late-stage study for an EU major customer.5

Bottomline:

- Consolidated profit after tax for Q2 FY25 was Rs. 58.82 crores, representing a 3% decrease Y-o-Y.

- Operating EBITDA for Q2 FY25 was Rs. 107.35 crores, reflecting a 9% increase Y-o-Y.

- Operating EBITDA margin for Q2 FY25 was 20.70%, a decrease of 14 basis points (bps) Y-o-Y.

Other Trends:

- Strong order visibility for the Specialty Chemicals segment is expected for Q3 and Q4 FY25, extending into FY26, supported by the Surat and Dahej assets.

- The CDMO segment holds a strong order book position for H2 FY25.

- Navin Fluorine is making significant investments in capacity expansion projects

- AHF capex for Rs. 450 crore is on track for commissioning by the end of FY25 or early FY26.

- Additional R32 capacity with a capex of Rs. 84 crore is progressing as planned and should be operational by February 2025.

- cGMP4 capex of Rs. 288 crore is underway, with Phase 1 (Rs. 160 crore) expected to be commissioned by the end of Q3 FY26.

- The company maintains a consistent dividend performance history, with a focus on ESG targets.

- Navin Fluorine’s core business strategy emphasizes a high-demand product basket, strong customer partnerships, and being a dependable fluorochemical company.

- The company is focused on driving operational excellence, financial robustness, disciplined execution, revenue stream diversification, partnership strengthening, and the creation of scalable platforms.

Competitive edge stems from factors such as:

- A strong brand reputation, state-of-the-art facilities, and a focus on building scale.

- Backward integration, deep expertise in fluorine chemistry, and a comprehensive approach as an integrated fluorine provider.

- Credible certifications, a competent team, and a commitment to safety and sustainable practices.

- Proximity to logistical options and a long history of expertise in handling complex fluorine chemistries.

Disclaimer: Invested and Biased. Less than 3% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions.

Aditya Birla Fashion and Retail Ltd (23-10-2024)

Lets review it after 2 years, I was holding force motors for 5 years when all capex was done, year 2023 it turned to 10000 from 1200. It is undervalued as if now hence holding it.

Adani Power board to consider Rs 5,000 crore fundraising plan via NCDs on October 28 (23-10-2024)

Adani Power will consider raising funds worth Rs 5,000 crore by way of public issue and/or private placement of non-convertible debentures (NCDs) in one or more tranches, the company on Wednesday informed in a filing to the exchanges.