Come to Bangalore, its so common here. ICICI Bank has a bigger one.

Posts tagged Value Pickr

Jagsonpal Pharmaceuticals – What is driving the price? (20-04-2024)

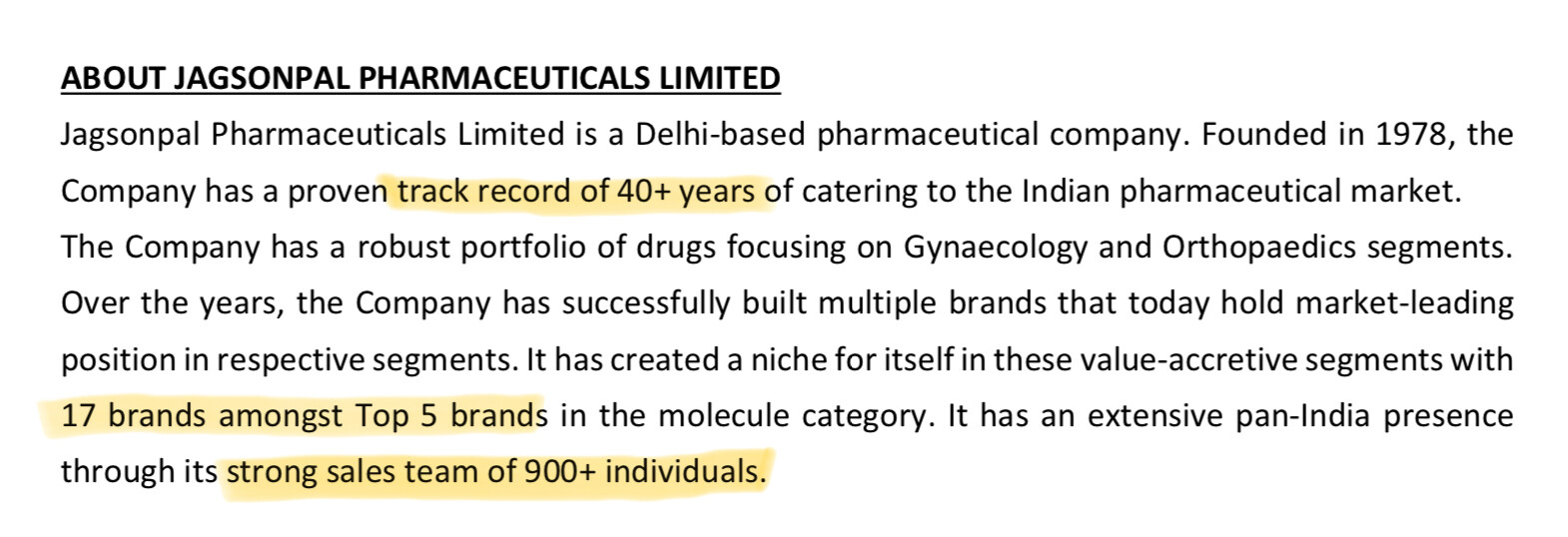

Sales team / Field force of 900 is a large team.

In Indian Pharma Industry, Average Yield per month is around ₹5Lakh => 60 Lakh per Year => potential of annual sales of 540cr.

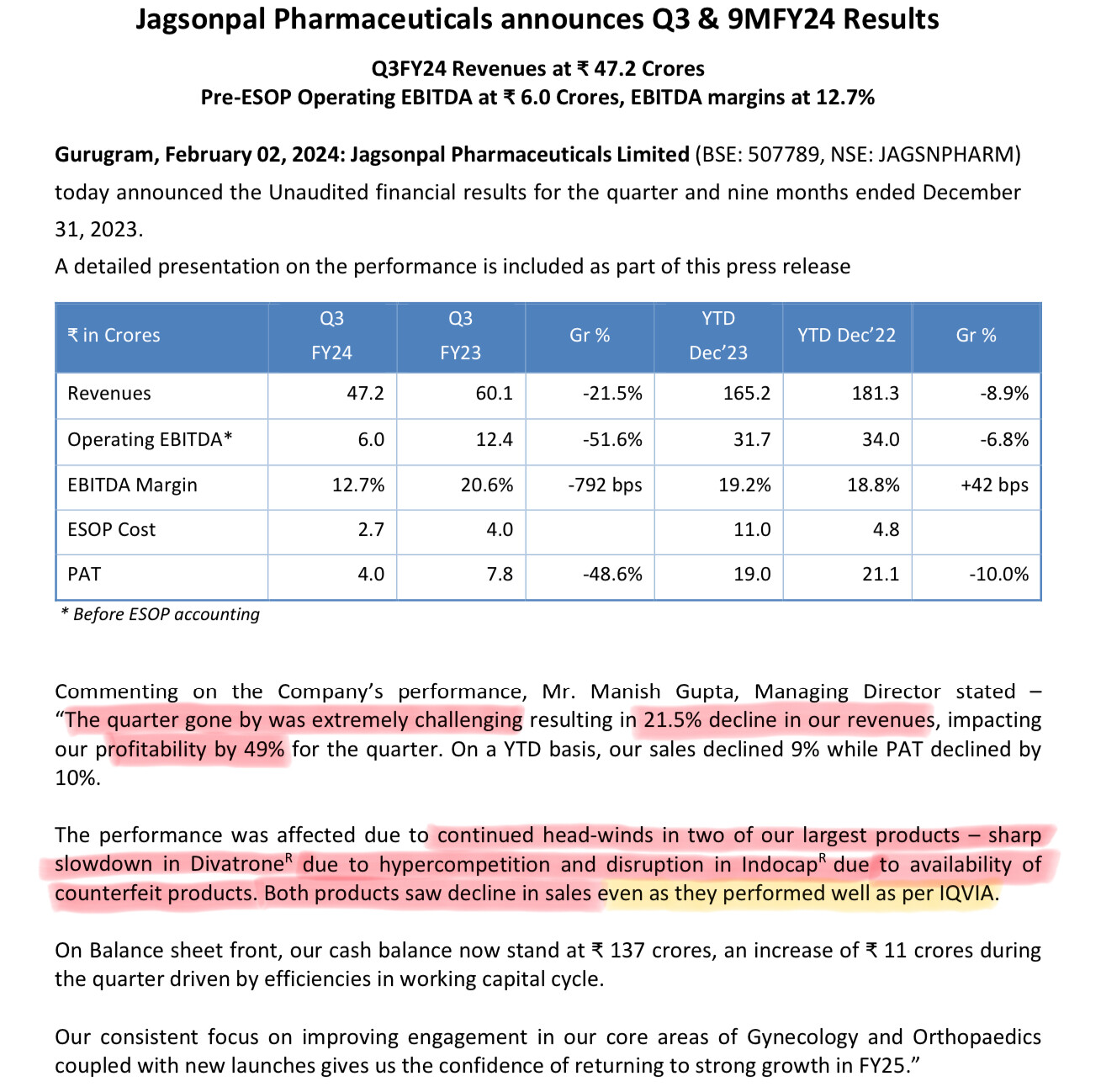

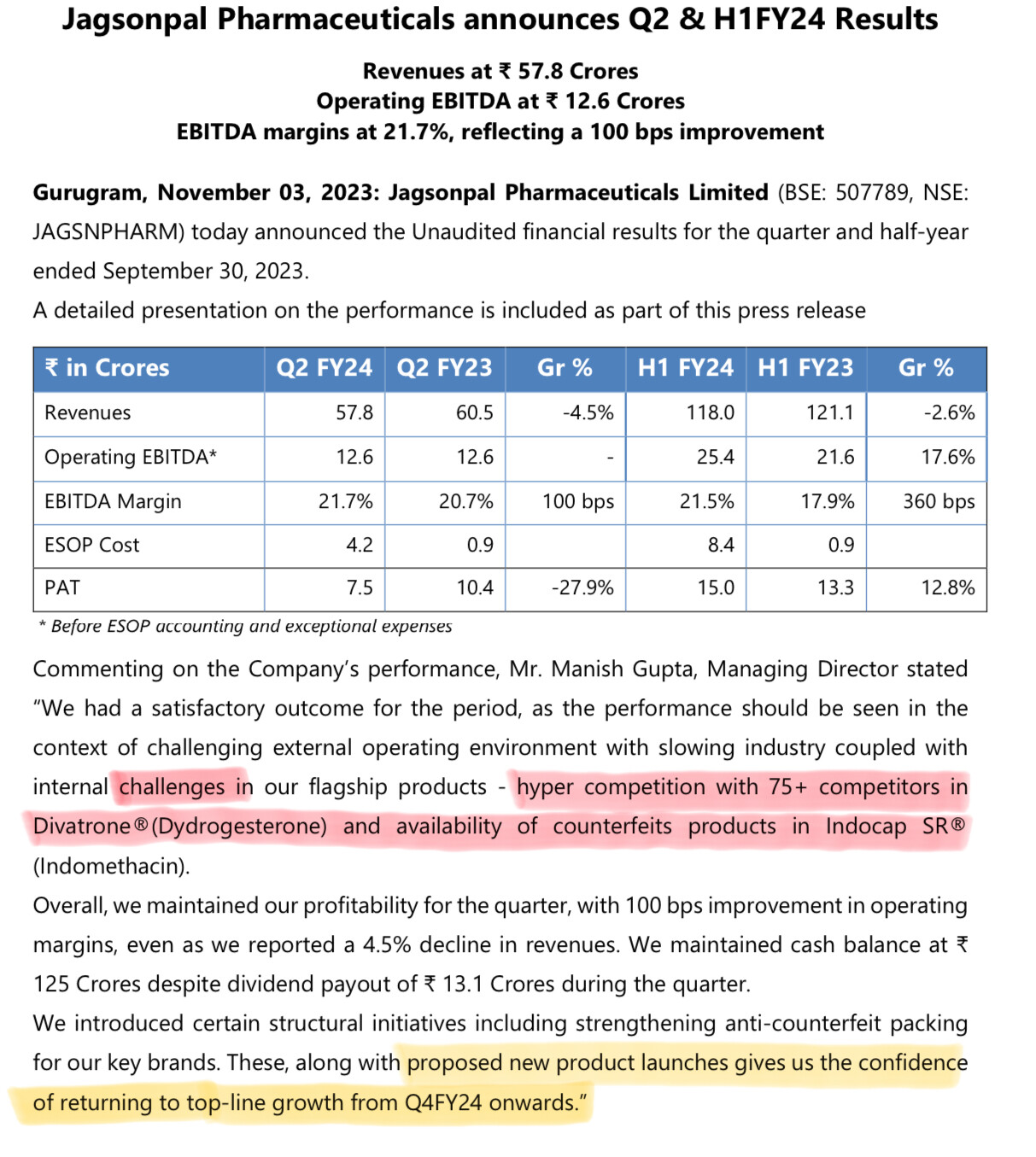

Mr. Manish Gupta has ability to improve the capabilities of his team, but since last 2-3 quarters, company is facing challenges in top 2 brands for which they increased the capacity (field force).

Therefore average capacity utilisation (of sales team) can generate more than 2xTTM sales. PAT would be much higher in that case.

New launches (as planned in Q4FY24) may improve the yield of sales team.

BKasal’s Portfolio (20-04-2024)

The Intelligent Investor’s Mistakes: Warren Buffett

38 Buffett’s Investment Stories, Gain Wisdom, Master Risk, and Maximize Profits to Build Enduring Wealth

“It’s good to learn from your mistakes. It’s better to learn from other people’s mistakes.” – Warren Buffett

One of its kind the author captured the investment mistakes of none other than a legend – Warren Buffett. It is an amazing one who started from scratch and became one of the richest men through investment. Buffett has the longest successful journey as an Investor and later as a businessman.

Along this decades-long journey, Buffett did many mistakes. It is an unusual paradox. These mistakes of both types of commission and omission.

Buffett acquired Berkshire Hathaway Inc. in 1965. It was a sick textile company. He turned it into a self-sustaining machine that generates massive returns for its Owners.

The book has 38 stories of companies. In them, Buffett made many types of mistakes that investors face. The book starts with the acquisition of Berkshire Hathaway. It goes up to recently in 2023, Taiwan Semiconductor Manufacturing Company Ltd. (TSMC).

The book is divided into three parts –

Part-A: Mistakes of Commission

The commission mistakes are typical to any investors, including Buffett. These are due to biases, evaluation of the company’s economic outcome, competitive strength, how to think about the market price movement, and much more.

Part-B: Failed to Capitalize in 2008 Crash

2008 US market scenario was comparable to the 1929 depression. This was the time the market was giving exceptional opportunities to invest. Buffett’s inappropriate capital allocation cost more to Berkshire.

Part-C: Error of Omissions: “Thumb Sucking”

The error of omission is not recorded in Berkshire’s net worth. Buffett and Munger both regret often the habit of thumb-sucking. These opportunities include companies like – Amazon, Google, and many more. The book presents you with what was going in Buffett’s mind when missed these opportunities and the lessons to be learned from them.

These stories help an investor to get exposure to different situations where mistakes are possible. Also, these companies are from various industries and operate in the global market.

The author has presented the lessons based on the Buffett’s story and own experience as an investor. The lessons are touching many aspects of investments like –

1) Investment Framework and Processes

2) Investment Strategies

3) Risk Management

4) Capital Allocation

5) Valuation

6) Smart Diversification

7) Decision Making

The book is a collection of 38 companies or industries written in crisp and to the point. The author avoided jargon and wrote to give maximum value to the investors. The author himself in the stock market for the last 20 years. Hence he understands the problems faced by investors. Hence he focused on lessons and solutions for investors.

These lessons would help investors to guard against their own emotional biases. These are common challenges faced during investment journey. However, the important aspect is to recognize and act upon is what counts.

So, the investors who want to leverage on legend’s mistakes and take lean in their own journey through the book.

Get Here: https://relinks.me/B0CW1CKX8H

Force Motors – racing ahead! (20-04-2024)

They have announced their results date for the year ended a month earlier than all the time they have done before. 26 Apr 24 it is. Last year it was on 29th May 23, and before that 27th May 22.

Hindustan Unilever (HUL) (20-04-2024)

The value investors have been telling this since 2017 and not for decades. They are right. Since then for 6 years, CAGR has been 6%. HUL need to continue to underperform for atleast 2 years in this price so as to reach 40 PE which is the right entry point to makes 12% CAGR in the next decade or stock need to correct another 20% for a value investor to buy in this year.

HDFC Bank- we understand your world (20-04-2024)

No fireworks, profit slightly below expectations. Don’t think markets will be distributing sweets unless the management has a palatable explanation for the floating provision it has made.

c519bb2e-9c54-4d27-a1eb-dc2dd9c09be6 (1).pdf (901.5 KB)

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (20-04-2024)

OM, Good Analysis. Have been invested in GAIL from far lower levels and some months now, I understand the company in detail. Actually growth propects here will be the Piped Natural Gas scheme if Modi 3.0 comes to power. You will see transmission volumes and import volumes skyrocket.

Howver this was more about Green Hydrogen or derivates calculations. Not about Gail. Here I feel we are ahead of the curve. There will be smarter options than investing in large chemical/ power companies with small Green Hydrogen business.

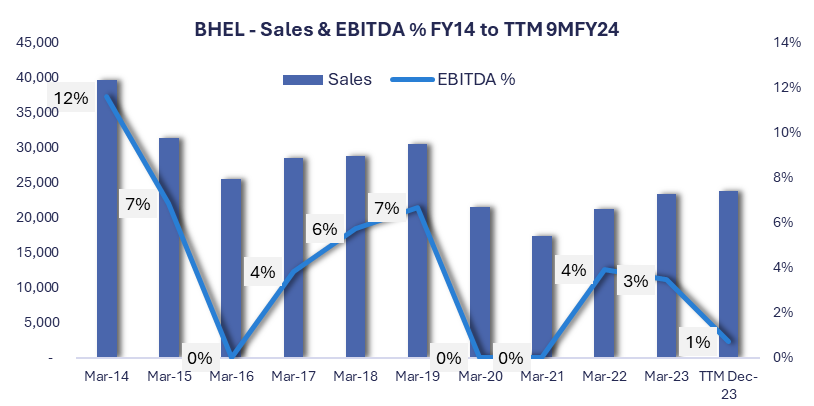

Bhel (20-04-2024)

BHEL – Investment case

- Company Overview – BHEL

- BHEL – PSU is India’s dominant producer of power & industrial machinery since 1964

- 200 GW+ installed capacity (70% power generation in India from BHEL Installed capacity in India)

- Key beneficiary – Aim to achieve 50% market share from non power segment (30% presently)

- Attractively placed for capacity addition of high growth sectors – Decarbonization, Green Hydrogen, Transportation, Aerospace & Defense with impetus on “Make in India” & “Atmanirbhar Bharat”

- Market Cap – INR 88k Crs, Revenue INR 24K Crs, P/B – 3.4x

- Order book – 1.2 lac Crs

- 503 patents filed in FY23 – Total IP – 5,443

- Selling shovels during a gold rush

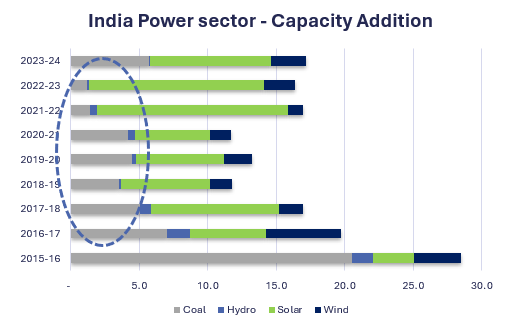

- Minimal Thermal capex investment for during 2017-24 period (<5 GW pa)

- Leading to deficit in 2024-27 period

- Focus on capacity addition – Thermal, Solar, Wind

- At the bottom cycle from financials, upward cycle has begun

- Investment case

Good

- Uptick in thermal capacity addition due to strong electricity demand, uptick in spot market prices and no major capacity addition in next 3 years

- No major presence of Chinese / International BTG supplier – major beneficiary last time

- Strong order inflow from Central, State & Private sector utilities

- Improvement in order terms – commodity cost pass-through – learning from last upcycle

- Reduction in manpower – 50k to 30k

- 30% order book in non power sector & management focus on developing non power sector order book – Target 50%

- Decrease in competitive intensity will lead to better margins

Better

- Decarbonization opportunities – FGD, Green Hydrogen, Renewable generation

- Defense & Aerospace opportunities – Cryogenic component, Batteries and other components for Chandrayan -3, indigenization of imported parts

- Transport opportunities – Railways & Urban Transportation – 80 Vande Bharat trains Kavach etc.

Best

- Efficient capital management from shareholder perspective

- Improvement in efficiency at part with best global OEMs

- Improvement in execution capabilities

- Recovery and resolution of sticky receivables through mutual agreement, arbitration & other mechanisms

- Ability to make significant break-through in decarbonization and green hydrogen sectors

- Technical analysis

Price uptrend continuation with all time high volumes

- Risk

- Being an PSU, majority shareholder may influence business decision, capital allocation strategy

- Historically faced with sub par execution skills and delay in delivery, may not scale up due to such issues

- Profitability may be impacted, or receivables may not come through due to any reasons, as seen in last cycle

Disclaimer: Education purpose only, Not an Investment advice or recommendation.

Force Motors – racing ahead! (20-04-2024)

Quarterly updates

Driving_Force_Apr_2024.pdf (3.2 MB)

I G Petrochemicals Ltd (20-04-2024)

So just trying summarize the the current developments.

IG happens to the largest player in the industry (275l Mt pa) close to 50% of total domestic capacity. One of their key customers has actually backward integrated into PAN production for DEP. Meanwhile imports have sharply fallen by more than 50%. It is simply not possible to compete with cost of production of IG and all (economies of scale and cheapest producer). A substantial quantum of PAN is consumed by the paints sector which should sustain, but there is nothing which can change exponentially either on demand/supply side (as far as I understand) however, Indian players are benefitted by imposition of ADDs, some of which shall expire by CY26 I think, unless this factor opens up something.

Asset Turns are around 1-1.2x overall, erratic PAT/OPM keep the RoE/RoCE readings very volatile as well as PAN-Ox spread is the key to track which is directly related to crude and global demand function. So factors which are within control of IG happens to be lesser.

Maybe why in FY18 when RoCE was 35%+ P/BV was 3.5, but currently oscillating between 1-1.25x. Uncertainty maybe is the reason.

Probably why they’re now diversifying into downstream plasticizers (PVC led consumption) which is more stable margins and much higher Asset turns of 5x (mgmt guidance). Full scale productions to happen by FY26 end and should be interesting.

LT Borrowings have gone up, interest cost jumped up as well, which shall add another volatile reading to track: Int coverage ratio.

All said, may not be very comfortable for many right now, but key to watch how the industry dynamics change post the ADDs expire, and if the plasticizers make the business more stable. Both factors shall play out around the same time between CY26-27.