My best guess is that they need to provided for 1000 crs (from CARE rating report) for AIF as per RBI notification and if you consider 50 INR payment on application it comes around 1200 crs. Thanks!

Posts tagged Value Pickr

Tata Technologies (30-01-2024)

Some other highlights from the concalls apart from the ones stated in recent posts.

- Attrition further lowered to 15.4% Vs 23.5% YoY

- Head count addition of ~1600 over last year. It is ~14.5% growth

- Although Q3 is seasonally soft due to holiday season, it seems the revenue growth rate is tapering off. FY22 sales growth: 45%

FY23 sales growth: 25%

Q3 FY24 growth: ~14%

Considering sky-high valuations, not sure if price would sustain 1100 levels.

Not invested, not a recommendation.

Micro Cap Portfolio (30-01-2024)

Hi Malolan. All these Companies are below 1000 cr Market Cap.Let me know which Companies will Not be under Micro Cap?Some Companies are less than 100 Cr Mcap. What is your definition of MicroCap?These can also be called Nano Cap according to me

1.Avanmore Capital: Financial Advisory Company with decent track record and was trading at Low Valuations in November.Stock Has Moved up more than 40% since Nov,23

2.BA Packaging: Paper Sack Packaging Company.No debt, decent sales growth and High Promoter Holding.Stock Has Moved up more than 30% since Nov,23

3.BN Rathi Securities: Brokerage and Investment Management Company with decent sales growth, no debt and decent margins.Stock Has Moved up more than 30% since Nov,23

4.Beardsell:Makes Prefabricated buildings.Decent sales growth.Low debt and growing Margins.Stock Has Moved up more than 10% since Nov,23

5.CG Vak Software:Low Debt, Decent sales growth IT Company with decent valuations and Closely Held.Stock Has Moved up more than 15% since Nov,23

6.Control Print:Manufacturers Printing Machines.Company has low debt,decent sales growth.Closely Held.Stock Has Moved up more than 25% since Nov,23

7.Creative Casting: Makes Iron and Steel Casting.Has export Sales.No debt,high promoter holding and Decent sales growth.Stock Has Moved up more than 10% since Nov,23

8.DHP India:Manufactures and Exports LPG Gas Cylinders:No Debt.Sales have gone down in the recent quarters due to Europe Slowdown.Closely Held ,High Promoter Holding.Stock Has Moved down more than 5% since Nov,23

9.Diamines: Sole Manufacturer of Ethyl Amines with No debt and Decent Growth.Stock Has Moved up more than 10% since Nov,23

I wil update about the other Companies in a few days. Let me know if you would like to discuss about these companies in Detail.Would love to have a conversation.

It is also difficult to do a deep dive in these companies as there is No research Report or Mention of these Companies in the News.Looking at basically Financials and Industry to Buy these Companies.

See the bright Sun: Aditya Vision (30-01-2024)

This is big. Entry of a leading FII like Capital in a small cap like AVL shud rerate the stock further.

discl invested since long

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (30-01-2024)

You are right but I have often seen market ready to pay the premium till the company has tailwinds and performs good. KPIT has been delivering consistently good results which is why it still remains expensive.

SJVN Ltd – Hydroelectric power (30-01-2024)

Latest Order Win, for 100 MW Solar Power

The Company successfully bagged 100 MW Solar Project @ ₹2.54/Unit on Build Own and

Operate basis through a tariff based competitive bidding process of GUVNL Phase XXISJVN Green Energy Limited (“SGEL”) at a tentative cost of ₹550 crores.

Current Hydro + Solar Capacity: 59,87 MW.

Anticipated 12,000 MW by 2026 and company wants to acheive 25,000 MW by 2030 & 50,000 MW installed capacity by 2040 as per management. (Take it with large pinch of Himalyan Salt ![]()

Most of new capacity is solar. They are not into EPC or Solar Manufacturing.

Company is developer and operator of Solar Power Plant selling energy thorugh PPA and direct contracts.

Currently over-extended i beleive but long term should compound well.

Disclosure: Invested at much lower price.

Amara Raja Energy & Mobility Limited: Powering Ahead (30-01-2024)

Kind of a overhang apart from the BAU at Amara raja. Might help Mcap for Amara raja

See the bright Sun: Aditya Vision (30-01-2024)

AVL_1.pdf (443.6 KB)

The company aims to raise funds by issuing up to 7,90,405 equity shares to selected buyers at a price of ₹3,573.17 per share, totaling approximately ₹282.42 crore. Name if investers are

(a)SMALLCAP World Fund, INC

(b)American Funds Insurance Series Global Small Capitalization Fund

MPS Ltd (30-01-2024)

Two soft instances from Q2Fy24 call:

-

The way Rahul flaunted that he became CEO at a young age of 31 and then followed this by over-emphasis on this pedigree, being a alumni from Wharton & Harvard. It sounded un-necessary to talk about this to answer the point around evolution of the mgmt, company.

-

The way he flaunted that their PAT target of 130 cr in FY24 is a done deal (& it was supposedly a extremely conservative guidance, which now they may even miss) & how they have over-delivered wrt guidance in the past. Also, he went on to entice the investor to extrapolate the guidance based on their past. Mgmt needs to be humble in my view. In a business, nothing is certain given so many known, unknown variables to be managed. To me it was a sign of over-confidence, arrogance.

Note: This is my own personal way of assessing leadership both within my organization as an employee and as an investor. Hence others may have completely contrary reading of such instances.

Usha Martin- Coming out of Chaos (30-01-2024)

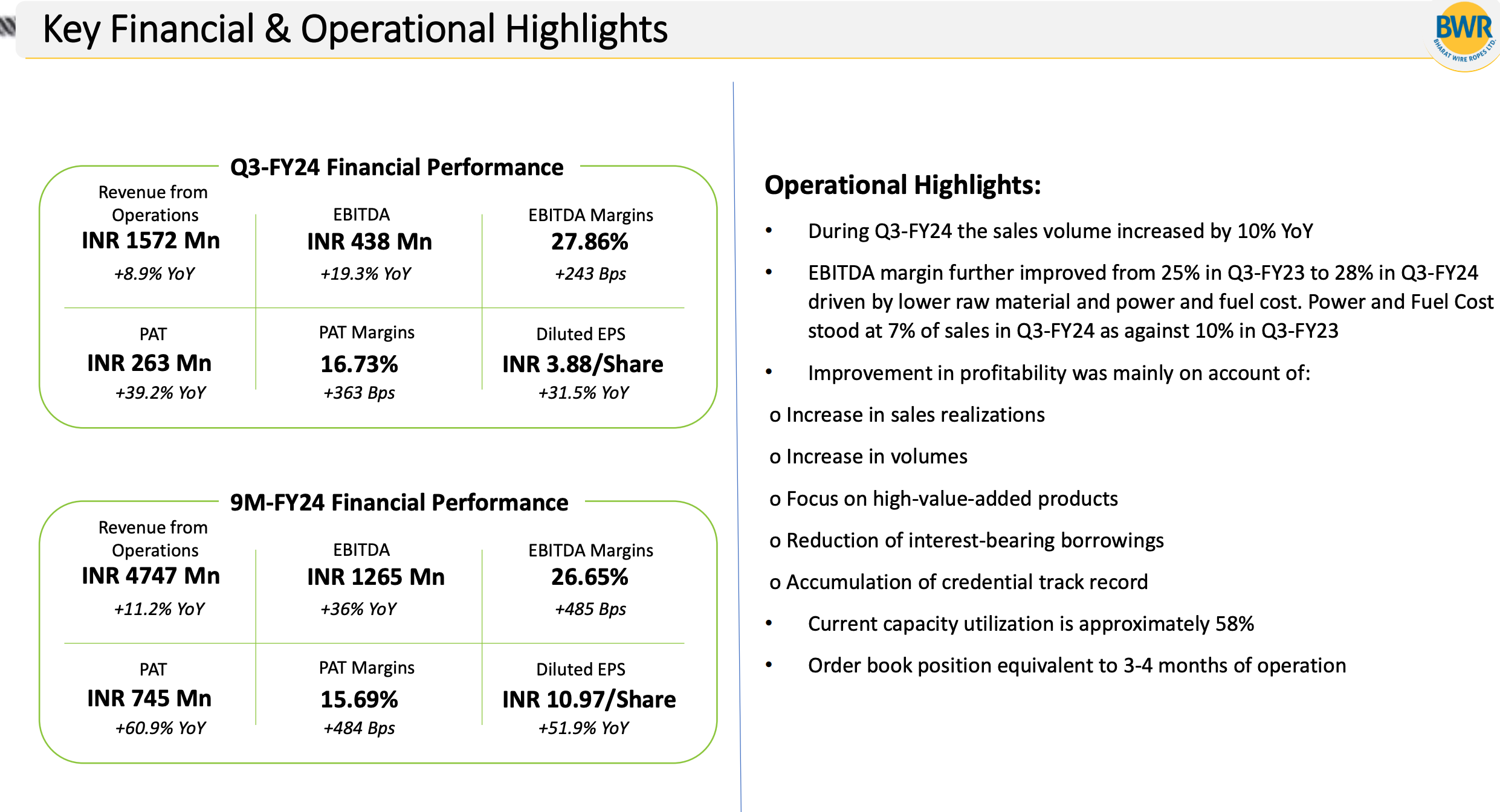

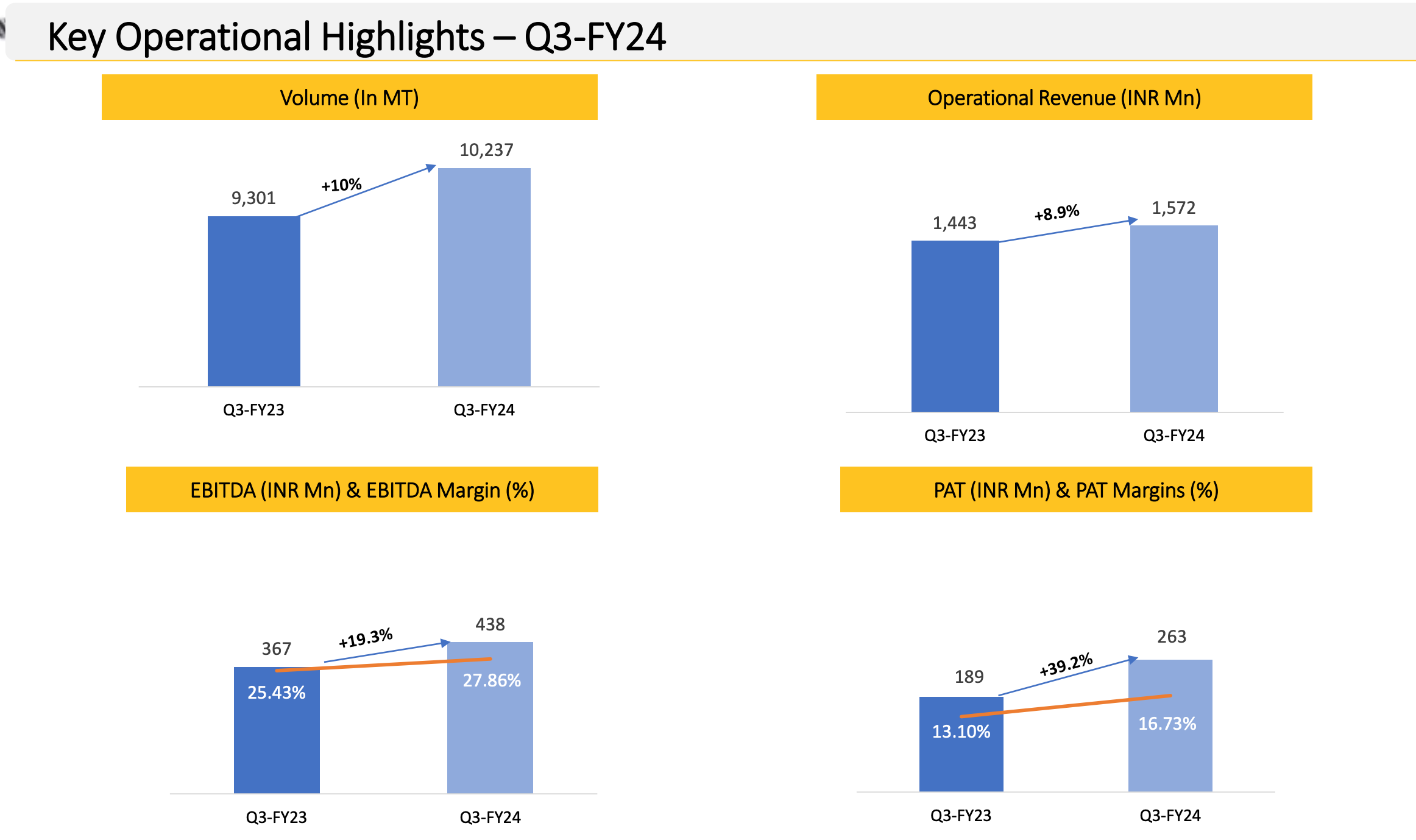

Some insights from Bharat Wire Ropes Q3FY24.

Organized scrappily to save time. Source: [Concall Q3FY24]

Sales mix and customer insights

80% of revenues from exports. Most of the products are sold through distributors. Management could not ascertain which sectors were driving the demand. The commentary was generic – “getting good traction from all sectors”. Mgmt indicated they don’t have unique SKUs for different applications such as O&G and Marine.

Growth: Steel and product prices declining over the last few qtrs. Volumes have gone up. The company is increasing its global footprint, distribution, and working on new product lines. Expects 20% of revenues from special ropes in the next 2-3 years.

Cap utilization

- The strategy is to increase cap utilization from 60-65% to 80+% by de-bottlenecking.

- This will cost 25-30 Cr over the next 18-24 months.

- ROCE/Asset turns on capex: No clue.

- Capex: Only on the drawing board.

Competition: No clear answers on competition and the supply scenario.

Current order book: 150 cr, 2-3 months

EBITDA margin expansion over the last 2-3 years: We’ve achieved these numbers by putting numerous efforts – sales efficiency, product mix, cost controls. This business is asset heavy and asset turnover is low.

Q: Why are you being conservative?

A: Wire rope is a conservative product. Buyers don’t switch brands easily. We’re continuously adding new customers and products. We’re participating in conferences and exhibitions at global level.

Disclaimer: Invested