CEO of Choice International in recent interview with Zee Buisness,

Exclusive Interview with Arun Poddar, CEO of Choice International | Q3 Results and Sector Outlook

CEO of Choice International in recent interview with Zee Buisness,

Exclusive Interview with Arun Poddar, CEO of Choice International | Q3 Results and Sector Outlook

Thanks for the response Sanjeev

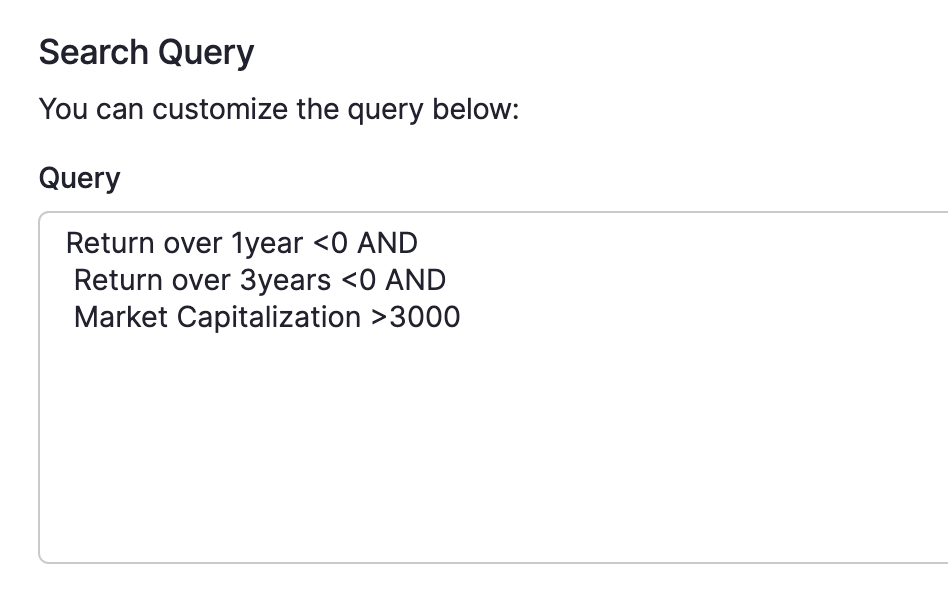

Based on the above post I’ve filtered stock that gave negative returns over 1 and 3 years timeframe.

The screen is as below

I’ve inserted all the 21 filtered stock in a Googlsheet and would be tracking the performance

Link to the Googlesheet

Disc: Not a reco to buy or sell

Business Overview

Choice International Ltd was incorporated in 1993. It is an integrated and diversified financial services group. It provides a wide range of financial services that includes Broking & Distribution, Investment Banking, Financial Services to Business Advisory, Regulatory Compliances to Government authorities & other corporate entities, Retail loan distribution, Mutual Fund distribution, technical services, and other ancillary services. The registered office of the Company is in Mumbai.

KEY POINTS

Business Segments

1. Broking and Distribution Business:

Co. offers stock broking services, insurance broking and wealth services. The stock broking business is channelized through their subsidiary M/s. Choice Equity Broking Private Limited.

The Insurance Distribution Services are provided through its subsidiary M/s. Choice Insurance Broking India Private Limited.

Wealth Services are channelized through its subsidiary M/s. Choice Wealth Private Limited.

As of Q1FY24, company has 7,21,000+ Demat Accounts out of which 207,000+ are active accounts. The company has Rs. 322 Bn Stock Broking AUM and Rs. 4,054 Mn Mutual Fund AUM and 8000+ insurance policies sold.

68% of revenues from this segment comes from Tier 3 and below cities.

2. NBFC Services: Key services under this segment include MSME Flexi Credit for Micro Enterprises, Loan against Securities, MSME Supply Chain Finance, etc. The NBFC services are routed through its wholly-owned subsidiary, Choice Finserve Private Limited, which is an RBI registered Non-deposit-taking NBFC.

As of Q1Fy24, company has Rs. 4.15 Bn

Total Loan Book out of which Rs.1484 Mn is the Retail Loan Book.

3. Advisory Services: Key services under this segment include management consulting, investment banking, infrastructure consulting and government advisory. Their Investment Banking & Merchant Banking services are catered through wholly owned subsidiary Choice Capital Advisors. Infrastructure consultancy business is offered through its wholly owned subsidiary Choice Consultancy Services Private Limited.

As of Q1FY24, company is present in 10+ states with an order book of Rs. 5.27Bn. The company serves max advisory projects in Maharashtra with 63% revenue share.

Revenue Mix – Q1FY24

Broking Services – 59%

Advisory Services – 28%

NBFC Services – 13%

Geographical Footprint

Co. has 104 offices, 150+ Inhouse Tech xperts, 32K+ Choice Business Associates, 850K+ Clientele, 3.4K+ Team Strength across India.

Choice Equity Broking Private limited (CEBPL)

In February 2022, the entire control of “M/s. Escorts Securities Limited (ESL)” was taken over by CEBPL. CEBPL contributes to 58% of the Co.’s total revenue.

Choice Consultancy Services Private limited

The subsidiary offers consultancy in sectors such as Road, Highways and Bridges Development, Water Management, Affordable Housing, etc.

Retail and Institutional Services

The Co. offers B2C services which include Stock Broking, Wealth Services and NBFC Services. The B2B services comprise of Management consulting, Investment Banking and government services like Infrastructure Consulting and Government Advisory.

Acquisition of Insurance Broking Business

In October 2021, the Co. acquired a 50% stake in M/s. Choice Insurance Broking India Private Limited, a Registered Insurance Broker with IRDAI, by acquiring 6.6 lakh shares for a consideration of ~Rs. 59 lakhs.

Acquisition of Mutual Fund Distribution Business

During FY22, the Co.’s step down subsidiary ‘M/s. Choice Wealth Private Limited’ acquired mutual fund distribution business of Centcart Money Services Private Limited.

In October 2020, the company acquired the mutual fund distribution business of “Bank Bazaar”.

Conversion of Preferential Warrants into Equity Shares

In January 2020, the Co. had allotted ~1.9 Cr Equity Warrants at a price of Rs. 51 per warrant. During FY22, ~1 Cr Warrants were converted into equivalent number of equity shares in trenches. As on the year end there are no outstanding warrants to be converted into equity.

Rights Issue

During FY22, the Co. raised ~Rs. 51 Cr through allotment of 99.5 lakh Equity Shares at a price of Rs. 51 per share on Rights Issue basis.

Bonus Issue

Co. issued a bonus issue in the ratio of 1:1 in FY23 increasing their authorised equity share capital to Rs. 108,00,00,000/- with FV of Rs. 10 /- share.

Decline in Promoters Shareholding

The promoters shareholding have decreased from ~64% in December 2021 to ~51% in September 2022.

Subsidiaries

The company has 11 subsidiaries under its portfolio as of Q1Fy24.

Stock is in expensive territory

But…

In the B2C tech space, monetization is a tough task. Mappls has started it this quarter, with the launch of the Cadbury advertisement. Unlike B2B businesses, B2C apps require regular investment in marketing to increase adoption, after which a long-term viability can be established. In this regard, Mappls has a long way to go before replacing Google Maps, which is a household name.

@moneycontrol

Hi. I wanted to dig deeper into the chemical business.

Of the Rs450cr of revenue, any idea about the contribution of the industries – How much is Pharma, how much is Agrochem etc

Any major right to win in any of the chemicals – website mentions a lot of names but not sure of the 80-20 principal here

*Is there a possibility of margin improvement in the vertical and

Any inputs on the vertical will be very helpful

GLS has signed a new CDMO deal worth $5 millions. Hopefully, the change in promoter company brings in lot more CDMO deals (as the new promoter is not a pharma company itself, at least as of now)

Folks

Ran a small and easy experiment

Hypothesis: Does stock with underperformance in short to medium term tend to outperform in future ?

To check this hypothesis I’ve used a simple screener with just 1 condition. The results below

| Screen | No, of stocks | Returns after the underperformance | |

|---|---|---|---|

| Market Cap 1 years ago < Market cap 3 years ago | 3619 | 37.21 | ← return over last 1 years |

| Market Cap 1 years ago > Market cap 3 years ago | 172 | 3.48 | ← return over last 1 years |

| Market Cap 3 years ago < Market cap 5 years ago | 2911 | 39.06 | ← return over last 3 years |

| Market Cap 3 years ago > Market cap 5 years ago | 599 | 29.06 | ← return over last 3 years |

| market cap 5 years ago < market cap 10 years ago | 624 | 25.77 | ← return over last 5 years |

| market cap 5 years ago > market cap 10 years ago | 2082 | 18.12 | ← return over last 5 years |

Remarks: The screening is for all available stocks in screener as of 19 Jan 2024. No other filter other than what’s mentioined. Median is considered instead of mean to remove bias caused by outliers

Conclusion:

Disc: Just sharing my conclusion. Not a reco to take any action based on this

After Spending Good Time Here’s My Take

Industry Overview

The global flexible packaging market, which accounts for more than 60% of the total packaging market is expected to grow at a CAGR of 4.8% from $ 249 Billion in 2022 to $ 316 Billion in 2027.

Indian BOPP Industry has been growing at almost double of the India’s GDP growth rate over long term

As per a report from Grand View Research, the global speciality chemicals market size was estimated to be $ 616.2 Billion in 2022 and expected to grow to $ 641.5 Billion in 2023. Additionally, the industry is expected to grow at a CAGR of 5.1% to reach $ 914.4 Billion by 20307.

As per KPMG, the Indian speciality chemicals market represents 22% of the country’s chemicals and petrochemicals market with a valuation of $ 32 Billion. With the industry expected to grow at a CAGR of 12% from 2020 – 2025.

The Masterbatch market was estimated to be valued at $ 11.1 Billion in 2020 and projected to grow at a CAGR of 5.1% leading up to 2025 with an estimated valuation of $ 14.3 Billion. Synthetic Paper – Durable alternate to paper. Global market 100kMT (India 6k MT) – immense potential to grow.

The Indian pet care market may be smaller compared to the global market, valued at ₹ 5,100 Crore and it is growing rapidly with a projected annual growth of 25% from 2023 to 2027

Company Profile

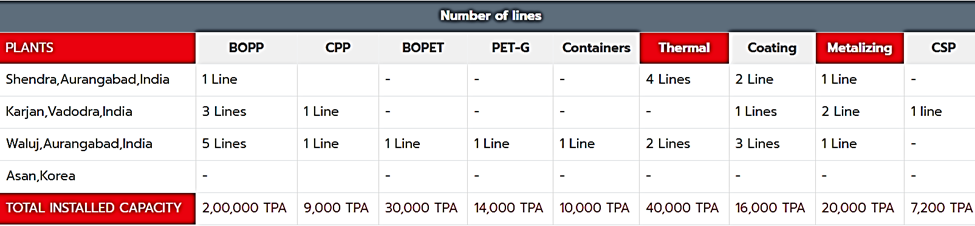

Established in 1981, Cosmo Films Ltd.is the pioneer of BOPP Films Industry in India. Promoted by Mr. Ashok Jaipuria, the company is also the largest BOPP film exporter from India.

Cosmo Films Limited produces specialty films for use in labelling, lamination, and packaging. The films that it offers are cast polypropylene (CPP), biaxially oriented polypropylene (BOPP), and soon to be available, biaxially oriented polyethylene terephthalate (BOPET).

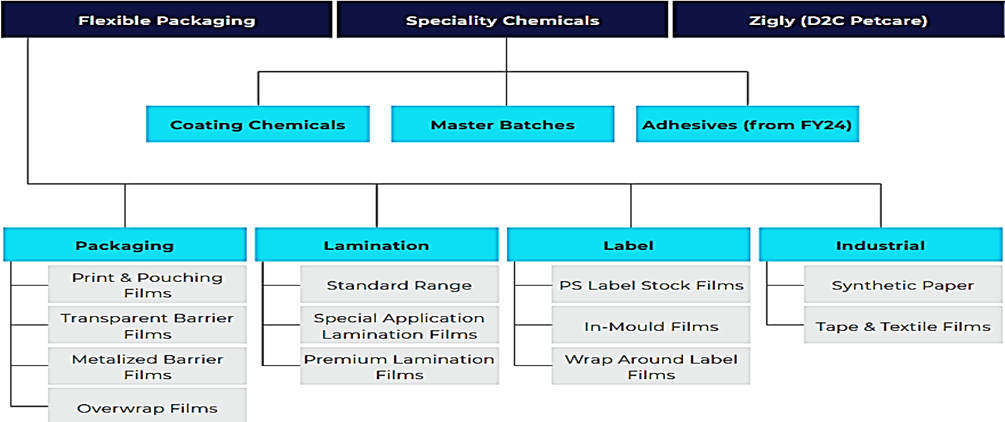

Cosmo First has expanded its portfolio to include Cosmo Speciality Chemicals having three vertical – master batch, coating chemical and adhesive and Zigly, a pet care brand that offers a full range of services and products for pets.

Company serves to 100+ countries and has 2 R&D labs with most sophisticated equipment and instruments, one in India & another one in USA.

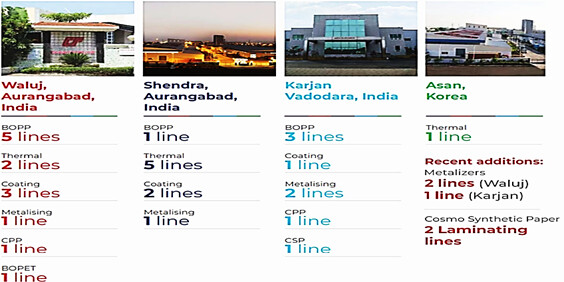

The Company has 4 state of the art manufacturing facilities – out of which 3 are located in India and 1 in Korea. The total installed capacity is as follows:

Why Fall?

Supply overhang and margin compressed across the industry leads to correction in the earnings

During FY23, the BOPP & BOPET industry faced excess supply due to bunching of several new production lines. Although demand continues to grow, the bunching of supply caused a margin drop and impacted the whole industry.

Currently India BOPP production capability is estimated at approx. 850k MT per annum. India domestic BOPP consumption is approx. 650k MT per annum and remaining is broadly exported.

Inventory loss

Fall in Volume More than Expected

Why We Are Studying?

Business Model

Cosmo First Ltd. operates a diversified business model across three segments:

Company have B2B Model and Accounts 50% Export of overall Business

Work on Cost Plus Model, Thus does not cost Benefit from lower input Cost that is Volume and Operating Leverage can only help to grow the Company

Product Portfolio

Manufacturing

Revenue Split

Geographically-45% followed by Domestic 55%

Key Clientele

Pepsi, HUL, P&G, ITC & many more

Competitive Strength

Future Outlook

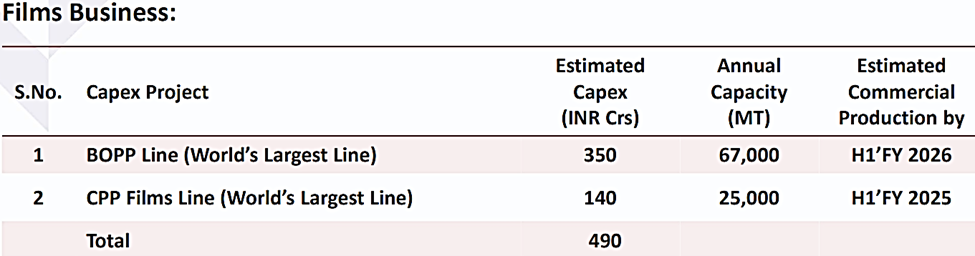

The BOPP (10th) and CPP (commissioned by 2024) line projects are moving forward according to schedule. By March 2025, both lines will be the largest in the world in terms of production capacity , and they will gradually boost the company’s production capacity by almost 50%.

The company has also started metallization of capacitor film recently which shall serve the rapidly growing electronics industry in India with Cosmo’s capacity in Phase 1 shall be 600 mtpa by Q4 of this year & revenue will be close to 40-50 Cr

Company’s New Business of rigid Packaging (Initial 40 Cr Investment) will add capacity in Phase 1 shall be 4,800 mtpa which should be able to generate between Rs.70 Cr to Rs.80 Cr of annual sales in nex 12-18 months.

Specialized Chemicals (scaling up in coming years) – Estimated INR 50 Cr Capex in next 3 years

Company with diversified businesses with target 20% CAGR topline growth in next 3 years coupled with commensurate return growth

D2C Pet Care businesses (19 nos. of experience centers as at Sept 2023 – plan to significantly increase to100+ in a couple of years beside online business)

Risk

80% of Current Liabilities is Advances from Customers.

& 80% of Inventory is of Projects in Progress.

Thanks for Providing a more points to consider.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/b6587787-b752-4b2f-8e30-9ea2452dded4.pdf