Posts tagged Value Pickr

Hitesh portfolio (20-10-2024)

then, how do you decipher that next 2-3 years of earnings are baked into prices. I mean, for entry levels this leaves them bewildered, as to whether we will ever be able to say anything with confidence about the price.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (20-10-2024)

Hey, can you give breakdown of how you see value of subsidiaries at INR 700 – INR 770 / share?

My calculations estimate subsidiaries value at more like INR 600 – INR 620 / share (after 20% holding discount).

Kiri Industries: Loan reduction and demand surge (20-10-2024)

Reminds me of Warren Buffett quote “A full wallet is like a full bladder; you may have the urge to pee it away”

![]()

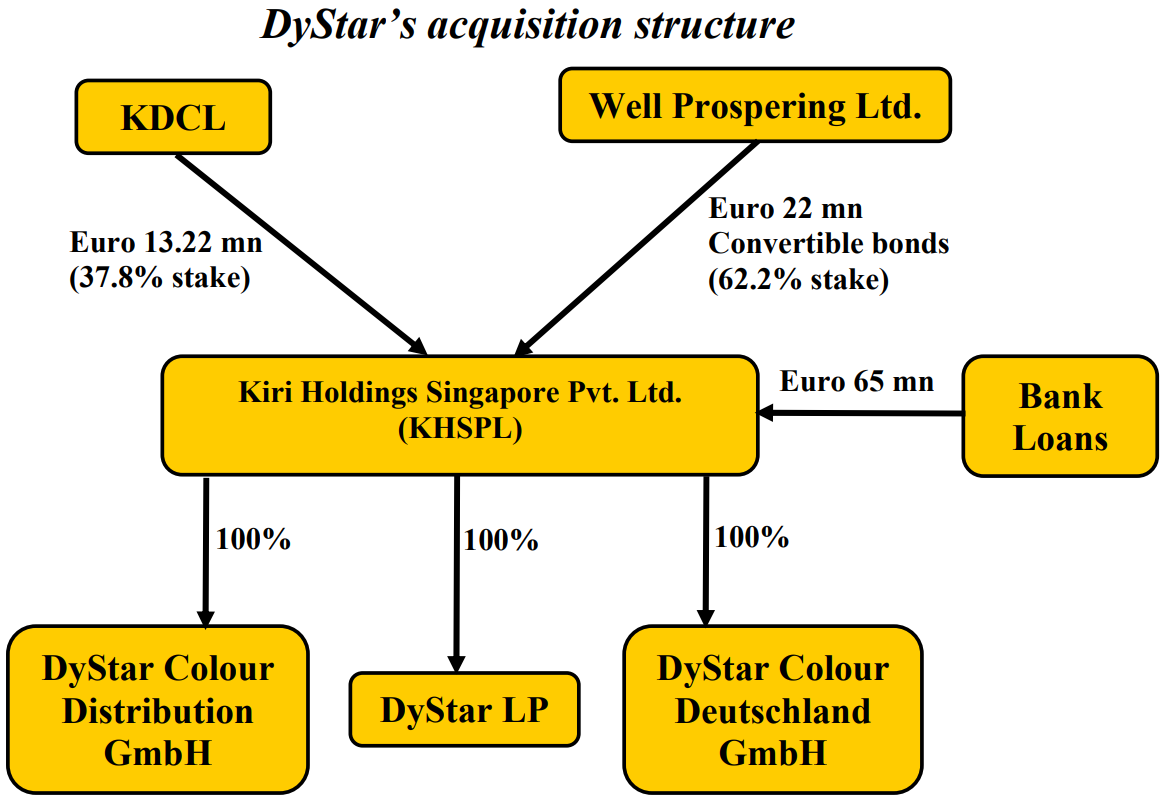

Another fun fact below folks – this is from 2010 showing the Dystar acquisition capital structure – Below structure shows that KDCL (which is Kiri Industries) put Eu 13.22 mn for 37.8% equity stake and allowed Well Prospering Ltd. (which is LongSheng or Senda) to take majority stake 62.2% as Convertible Bonds. This meant that

- Senda had option to convert into equity if things go great (and they did convert into equity and took control and started Minority Oppression on Kiri) and

- if things go south – Kiri takes all downside and Senda with its debt is superior to Kiri’s equity in capital stack. Sends was responsible and covered itself as this acquisition was from bankruptcy proceedings. But Kiri was clearly aggressive. And they still show this aggression in the latest Litigation Financing.

Again it may all work out fine but just highlighting why market is not recognizing the value and that promoter is clearly aggressive so much that in their aggression they take risky steps! The genesis of 10 years of legal case is the wrong structure which Kiri entered into in 2010. So in some way it is their own making.

Market is supreme!!!

Invested small portion of pf.

Kiri Industries: Loan reduction and demand surge (20-10-2024)

And what is more amazing is that in 2013 the promoter’s pledge was invoked wrongfully (as it was invoked despite Kiri paid all the loan) by the lenders and lenders sold them in the open market. So promoter’s stake went down. Despite this experience, promoter again went into pledge situation. And they did not learn anything basically.

Another case – betting significant money on copper project on the basis of one guy – Mr. Sarkar. Too aggressive behaviour.

Also compare this company with peers who are doing Copper project (Birla, Adani, JSW – all heavily experienced and deep pocketed players in metal/minning industry). So market will never value it till money comes. And still it should trade below cash till the 1st phase of copper gets operational in time and budget with limited bleeding in the 1st few months of operations. Basically lot of question marks so market will remain uncomfortable. This stock will not run on Hope but on Facts!

Disclaimer – invested small % of pf

Solex Energy – Undervalued Solar PV Manufacturer or Microcap Value Trap? (20-10-2024)

Anybody has idea on why promoter has decreased his shareholding in the last quarter ?

Va Tech Wabag (20-10-2024)

I feel if we take forward earnings of 2026, expecting a PAT of around 300 cr. That values it at 35 times fy26 earnings. I also feel the 15% growth will get re rated to a higher number on actuals. The management is very conservative in my view and may surprise on the positive side. Markets are factoring it now and the move last week was due to fund buying

Va Tech Wabag (20-10-2024)

Hi All,

Sharing my deep dive on Wabag. I feel from a valuation perspective it’s not very expensive currently which is why big funds are also entering at current levels. Covered my thoughts below.

The SME portfolio (20-10-2024)

What do you find interesting in Gem enviro?

Would love to hear the thesis.

The SME portfolio (20-10-2024)

below 2 tracking…

Saakshi Medtech & Panels Ltd.

Systango Technologies Ltd.