Hello everyone,

I’ve been tracking this company since it’s share price was around 250 levels, have sold most of my holdings at a good profit.

Thinking to reinvest, is this a good time to enter, considering the opportunities available in the near future?

Posts tagged Value Pickr

Mrs Bectors Food Specialities: Can it beat the industry? (27-11-2023)

ValuePickr Ahmedabad (27-11-2023)

I am forming a new whatsapp group for Valuepickr Ahmedabad as I think the admin of this thread is inactive from last many days. Anyone from Ahmedabad can ping me and we can schedule offline meets.

Shakti Pumps – solar shakti (power)! (27-11-2023)

No email, this is from the concall

My portfolio updates and investment journey (27-11-2023)

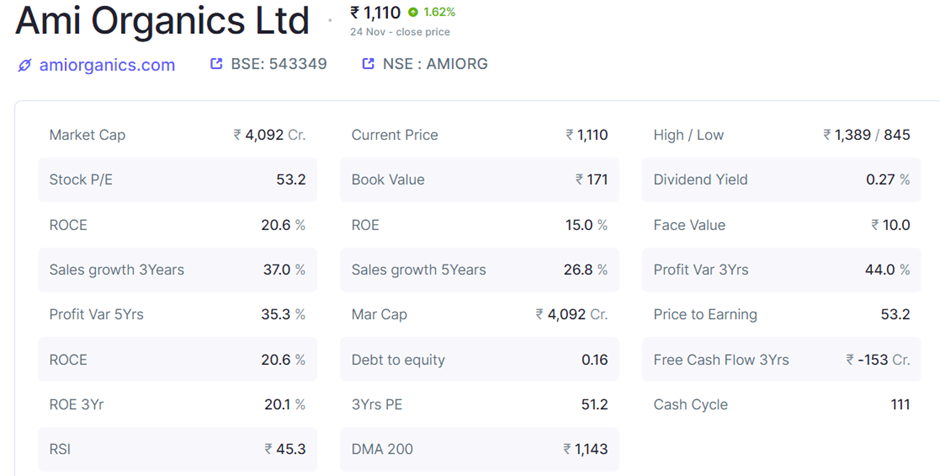

My notes on Ami Organics:

Source: screener.in

Summary rationale: I bought Ami Organics Ltd’s (AOL) just last week (24th November) making it over 5% of my portfolio. On the face of it stock looked expensive at over 50PE, however given the growth opportunities and its presence in sunrise industry (EVs and semiconductors) it looks reasonably priced.

My thesis on AOL is mainly based on three key opportunities:

- Long-term contracts with Fermion for 3 key molecules. One of the molecules Darolutamide used in Nubeqa is likely to have peak sales of over USD3 billion. AOL is the exclusive supplier for intermediates used in Darolutamide (an anti-cancerous drug) for a long-term basis. A back of the envelope calculation puts this opportunity to about 1200 crores* annually by 2030 if fully serviced by AOL. The patent for this drug expires in 2030. If we assume even other 2 molecules are as large then opportunity seems huge.

*Assuming cost of intermediate accounts for 5%. The cost of Acetaminophen which is used in paracetamol tablets like Dolo 650 is about 15%.

-

Electrolyte additives: AOL has developed electrolyte additives which are used in lithium batteries to increase the life of the batteries. Market size for this is estimated to be over USD1 billion and likely to double to USD2 billion in the next 3 to 4 years. AOL aims to garner 10% of this market which puts its revenue potential to about 1600 crores annually by end of 2030.

-

Semi-conductor chemicals business: AOL recently in Q2 FY24 acquired 55% stake in Baba Fine Chemicals (Baba) which is semiconductor chemicals. AOL aims to take Baba’s revenue to over 200 crores by FY25. This is a high margin business with EBITDA margins in 40% range vs. current AOL business in 20% range.

In addition to above, AOL continues to launch large market size products like UV absorber, and has maintained that further contracts with Fermion are in the discussions. All the new products are likely to support margins and operating leverage is likely to result in margins in 25% vicinity from current range of 20%. Currently margins are somewhat depressed as the company integrated Gujarat Organics plants over the last two years which exhibited very low margins.

I have modelled two scenarios

Opportunity based:

and,

Capex and management guidance-based scenario

In above two scenarios my worst return expectation by FY28 is likely to be 20% CAGR in scenario 2 (capex and management guidance based) with PE derating to 30. While best return expectation is likely to be at 43% CAGR in opportunity-based scenario with re-rating to 60 PE.

Right to win:

- Only company outside China to have developed Electrolyte additives

- 50-90% global market share in key molecules

- Chronic Therapy focus: ~90%

- Majorly backward integrated to Basic Chemical level

- Strong customer relationships with customers with relations lasting over a decade

- Diversified across pharma, agro, semi-conductors and electrolytes

Though some of the risks to above estimates are mitigated by first mover (outside China) advantage, exclusive agreements and India cost advantage, we still need to account for below risks:

- Regulatory risks related to Pharma Intermediates business – FDA related issues

- Product obsolescence – if a new and much more effective medicine becomes available then the expected opportunity of Fermion contract may not play out. It may similarly impact company’s existing products and pipeline.

- Competition – Electrolyte additive opportunity may not fully fructify if another competitor is able to replicate same outside of China

- EV adoption slow down

- Concentration risks – top 10 customers account for 58% of revenues.

Customers:

Company caters to major domestic and overseas MNCs.

Source: AOL Q2 24 presentation

Peers: Divis Lab (APIs), Neogen and Neuland.

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

NCC: Extremely undervalued (27-11-2023)

True. Still holding and adding small quantity once in a while. What baffles me is the way so many stocks have gone up with & without justification of fundamentals, while this one moves very slow. Makes me wonder if this is artificially done for the sake of accumulation

My portfolio updates and investment journey (27-11-2023)

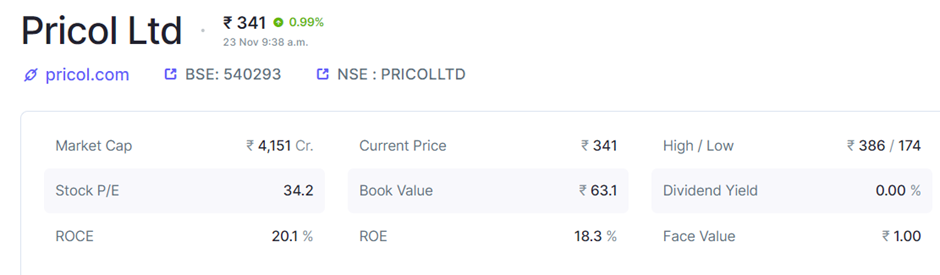

My notes on Pricol:

Source: screener.in

Summary rationale: Pricol was on my radar for last 6 months but now with about 12% correction I became interested. Price corrected post soft Q2 24 results. However, management continues to guide ~4,000 crore revenues by FY26 and some margin improvement (~200bps over next two years). Back of envelope calculation showcases about 35% revenue CAGR and profit growth well above it. LTM PE is 34 which means company is available at 1PEG*. I find companies less than 2PEG attractive.

*PEG: PE (price to earning multiple) to growth ratio.

DIS systems used to be in 200-300 rs for per vehicle now they are priced at 1200 per vehicle (2-wheeler). With increased digitisation and more sophistication these products are likely to go in 2000-2500 rs range over the next three years, as per the management.

Other triggers:

- Company has entered 4-wheeler market very recently with Tata Nexon models, previously they could not due to some anticompetitive agreements. If they can garner more share in 4-wheelers then it shall provide huge upside to the company.

- Increasing EV penetration results in high value per vehicle and higher margins.

- Beyond FY26 companies’ new product initiatives (Telematics, Battery management systems Micro Motors and Robotics and Artificial Intelligence based processes and equipment) through JVs will start bearing fruit and that will provide additional kicker beyond FY26.

- Ownership battle between promoter group and Minda Corp (15.7% stake) shall keep prices supported. Minda corp has reached out to competition commission to increase its stake in the company to ~25%.

Right to win:

- Over 50% markets share (in value terms) in 2 wheelers (2W), 70% market share in CVs and 50% market share in tractors.

- 8 of 10 2W EV models are served by Pricol

- Entry barrier for competition is moderate to high as auto ancillaries take about 2-3 years for product approval and another 6 to 12 months for production. In addition, products are customised for each model.

Risks:

- Tech disruption

- EV adoption slowdown

Products: Pricol makes driver information system (65% of revenues) and actuation, control and fluid management system (35% of revenues).

Source: Pricol Q2 24 presentation

Customers:

Company caters to all major 2wheeler, 3wheeler, commercial vehicles, tractors manufactures

Source: Pricol Q2 24 presentation

Competitor: Minda Corp

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

My portfolio updates and investment journey (27-11-2023)

Recently I have strated writing notes for my reference for stock identification and rationale: I provide below some of them:

My notes on stock identification – Garware Hitech Films (GHFL)

I was going through presentation by Ian Cassel on multi-baggers https://www.youtube.com/watch?v=trT3GmEWZPg . He talked about a business XPEL which makes Paint Protection Film (PPF) for auto companies. It has gone up over 100x in the last 10 years. I was interested in knowing if there is any such firm in India. I searched for “paint protection” in screener. First name popped up was “Garware Hitech Film”.

I went through company presentation and I was positively surprised. Exports account for 75% which means good quality products and cost advantages. It seems much more diversified across Auto, Industrial, packaging, construction etc. vs. XPEL (only Auto). Its main products are PPF (30% of revenues and 80%+ of it is exported) and Solar Control Film, SCF, (36% of revenues and 90%+ is exported).

Positive triggers ahead: SCF second line to have peak utilization by FY25, which means about 500 crores of revenues addition in two years (LTM revenue was ~1500 crores). In addition, there have been positive regulatory developments on safety glazing film (to achieve 6-8 % of revenues in next three years).

With above factors company can grow revenues at 15% CAGR for next two three years and bottom-line accretion could be in 20% range as company’s margins currently are suppressed due to aggressive investments (marketing and service centers) for PPF and safety glazing (it was banned in India but now re-launched).

Stock seems reasonably valued at 20PE with market cap of 3400 crores. It has a landbank of 1000 crores (source: Sharekhan report published on September 04, 2023).

Penetration of PPF on cars in India is below 1% vs. 10-12% in the US. PPF makes sense for cars above 20 Lakhs. This premium car market in India is growing rapidly. Hence, this can be a high growth exposure on auto growth.

Cost of PPF on per car in India including installation is 2 to 3 lakhs. ((credit to @spartan who has done some scuttlebutt)). While XPEL in its presentation shows 4000-6000 us dollars for PPF and ~1000 dollars for installation. So this puts total cost around 4 to 6 lakhs in the US.

Competitors: 3M, XPEL

Right to win (innovation, market share, cost) –

- In SCF, only company in the world with backward integration (Chip-to-films)

- Only one of 2 in dyed SCF

- Leading player in India’s shrink film (used in packaging) market with over 60% market share

- India’s first company to produce PCR grade & APR certified Ecofriendly Shrink Films

- GHFL is the only producer of professional-grade Premium paint protection film (PPF) in India.

Risks:

- Some related party transactions.

- Sitting on land of around 1000 crores (not an efficient use of resources) vs. mcap of 3400 crores

Thanks,

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

My portfolio updates and investment journey (27-11-2023)

Hi @praneet_drolia thanks for checking on.

Nuvama, Nippon life and 360 one have broadly similar themes. Nuvama and 360 One is play on India’s rich and Nippon life is bet on Indians who plan or in process to get rich. Financialisation is going to be big. I am not playing it through direct lending but through non-lending or indirect lending (Paytm and pb fintech).

Nuvama and 360 One have play on HNIs and UHNI’s through product offerings like AIFs, PMS, LAS and securities underwriting. We have noted how “play on rich” themes like Titan, Ethos and Cartrade played recently. While Nippon is play on mass market through ETFs and MFs.

Divgi Torque – this one came in a interesting to me. Someone I follow on twitter re-tweeted this article from Itus capital – Vol 13 – Survival of The Fittest – ITUS Capital . I loved the content, just amazing. Then i thought of knowing more about them. I really liked their “weekly enlightment” and “what we are reading” series. Then somehow I got to look at their portfolio and noted Divig as odd name (for me) out there. Then I researched and read annual report. Divgi Torque management is aiming for 1000 crore revenues over next 3-4 years which is about 4x of FY23 revenues. EV play, currently EV OEMs are importing the products they offer so a localisation play. Please read latest annual report – seems like a david trying to become goliath. Valuations seems high but should be seen in context.

Deepak is bit of special situation and their move on becoming specialised chemical play. PE seems reasonable at 10 but its difficult for me to understand this fully and hoping this to replicate Deepak Nitrite. I am quick to book losses if need be so please do not take action based on my thesis.

Medplus is negligible in my portfolio. But you should visit their latest presentation as it provides lot of insights – Highest ROCEs retail business is pharma, they covered only southern part with 3000 stores it can easily go to 6000+ stores in next 3 to 5 years, focus on non-branded private label medicines and OTCs can help them disrupt branded players.

Indiamart is I am trying to play a margin improvement game. Though my focus is currently on Garware Hitech, Pricol and Ami Organics. I will share detailed rationale shortly on those.

Tata Technologies (27-11-2023)

Then KPIT tech is too overvalued.

I would like to point out that when a cyclical sector is doing well, the high P/E is also justified

When the cycle ends, then stock price or p/e should decrease to reflect that