Yes, if Petronet is dependent on Qatar for supplies, then it is going to be restricted a lot by the GOI; all commercial contracts wth Qatar are being reviewed across all Gov sectors. See aviation, Qatar airlines taxes issues with the Itax dept.

Posts tagged Value Pickr

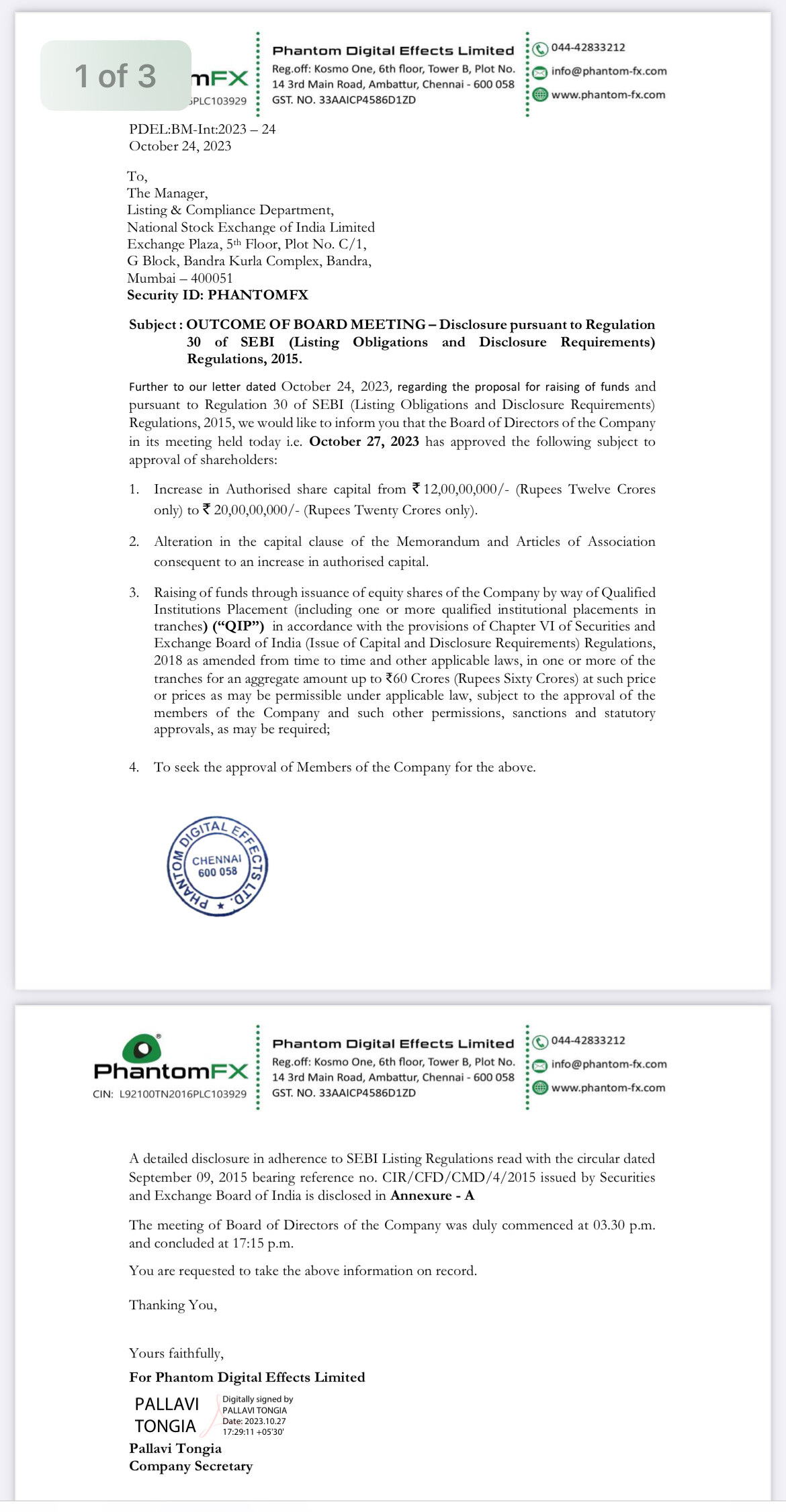

Phantom Digital Effects Limited (02-11-2023)

Fund raising of 60 cr! Looks like there is solid plan for expansion and coming up into new domain (as mentioned in the agm- it could be gaming vfx)

RACL Geartech Limited (02-11-2023)

https://twitter.com/GsinghGursharan/status/1719841312093176304

https://x.com/GsinghGursharan/status/1719841312093176304?s=20

RACL has 44 Mazak machines, the highest number of a single brand machines . First machine is 15 years old and still functional with 100% good performance.

V-guard – The passion of our early years and our quest for excellence (02-11-2023)

VGuard Q2FY24 Concall Summary

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (02-11-2023)

Central and State Govts are two important actors in this business. How will they react in election year if yield (farmer earning) goes down? Which of these or all will happen?

- Increase price for farmers!

- Direct less towards ethanol

- Allow domestic sugar price to go up (consumers=voters)!

Sadhana nitro :a Dog or a Horse? (02-11-2023)

Anybody calculated increased capacity of ODB2 and PAP will result in how much revenue increase. I do find prices and how much they may be selling approx?

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (02-11-2023)

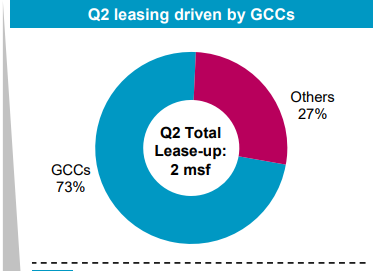

I attended earning call for Embassy REIT Q2FY24. After long time, management sound positive about prospect. They also increased leasing guideance for FY24.

Key positive factors:

Higher operating leverage from hotel business

Increased under construction area coming for completion during FY24 and FY24, signficant portion being pre leased and hence contibuting to cashflow of the company

Expected MTM gain realisation on renewal

Expeced policy decision on SEZ, which would result in higher occupancy for the trust in medium term.

Most important, GCC now being main class of tenants, with nearly 70% of leasing in Q2FY being to GCC clients.

Negatives:

Interest rate increase

Selling by sponsors

While there was no increase in guieance for FY24 distribution, I found management being confident to increase distribution in FY25 onwards. Based on my understnading, I have sold nearly 1/3 of my investment in IndiaGrid and invested in Embassy REIT in last 7 days.

Disclosure: I am not suggesting any investment action. I am not SEBI registered advisor. I have very great track record of being wrong, I was very optimistic about investment during April 2021 period. Embassy price decline from Rs 340 to Rs 300 since then. My view may be positively biased. I may change my investment (increase/decrease/exit) from Embassy REIT without informing members.

Jagran prakashan (02-11-2023)

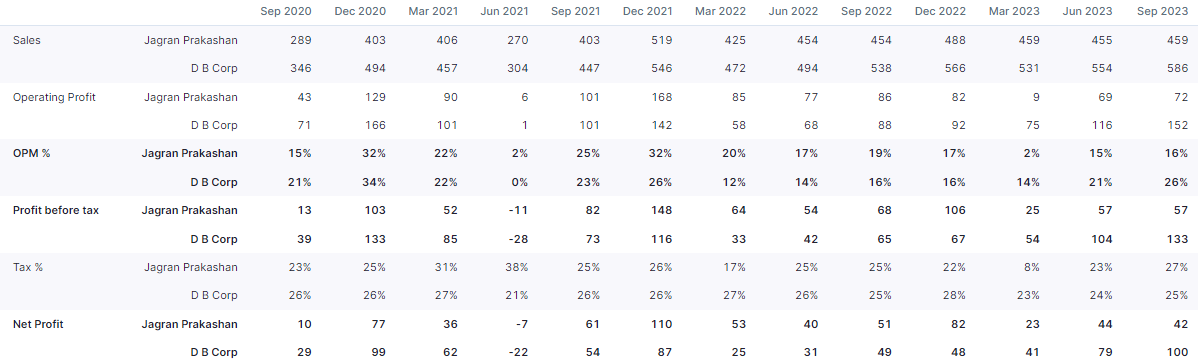

Post Q2FY2024 results of Jagran Prakashan, I find that the company performance has not improved. As per presentation of the company, performance continue to be adversely affected by limited growth in advertisement revenue and higher newsprint cost. While it expect improvement on both these factors and report improved performance during next H2FY24, I find something specific to the company which has adversely affected the performance then industry wise issue.

The rival to company in Hindi newspaper, DB Corp also reported number for Q2FY24. DB Corp continue to show superior performance due to higher advertisement revenue growth in lower newsprint cost.

Find enclosed quarterwise performance of both the companies.

In September 2022, Both DBCorp and Jagaran operating profit comparable Rs 88 cr and Rs 86 Cr respectively. In next 12 months, DB Corp Operating profit almost doubled to Rs 152 Cr same, for Jagaran declined during the period.

So, in my understanding, while the industry is doing reasonably, Jagarna Prakashan has lost market share to the peers in last 12 months. I would contribute to promoter family conflict as main factor for lackluster performance. Since, Jagaran Prakashan, was short to medium term trade (with expectation of benefit from higher ad spend in election year and lower newsprint price), I would have to exit at appropriate price. Given the family conflict situation, it is difficult for me to visualise benefit of better prospect being reflected in company performance. Hence, I have decided to exit from my holding in the company.

Disclosure: My view may be negatively biased due to my exit from the company. I am not SEBI registered advsior. I am not recommeding any investment action.

Goodluck India Ltd (02-11-2023)

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.bseindia.com/xml-data/corpfiling/AttachLive/17fe3b4f-4010-4436-abc4-cbe688ba6f41.pdf

GOODLUCK CONCALL HAS STARTED FOR TODAY

Saregama India Ltd: India’s premier music publishing label (02-11-2023)

Saregama acquires majority stake in start-up Pocket Aces – The Hindu BusinessLine

““Acquiring Pocket Aces will add on a whole new dimension of IP and a distribution network of over 95 million followers, which Saregama will leverage to further popularize its music library among the 18-35 audience segment. It will also create synergies across the artiste & influencer management and long-format video creation businesses of the two companies,” the music company added.”