does anyone know why stock corrected so much in recent time?

Posts tagged Value Pickr

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (01-11-2023)

Any idea when the bonus shares should get credited ?

Mine havent been credited yet

Wim plast (01-11-2023)

My relative saw the IPO ad and asked… “arent they already listed?”

And I said, “yes, I thought Wimplast had the Cello brand…”

It looks like another case of ‘ dont trust brands owned by holdco or promoter entity’. Interesting that nobody seems to be whining about this… But lets see how this pans out…

Kovai Medical Center and Hospital – Health and Wealth (01-11-2023)

As per an email response from the company, the company shares are listed only on BSE but not on NSE. They were traded on NSE as part of a NSE’s marketing strategy. Seems that marketing strategy period for trading of this company shares may be over and company would have to formally list its shares on NSE platform by following the procedure which may also need monetary expenses in form of listing fee etc. As of now company doesn’t have any plans to list its shares on NSE and it seems to be the case that company wants to save some cost. As such it’s not because of any kind of ‘ban’ that they’re not traded on NSE.

Seems like this is a pretty common scenario that I got to know recently. There are many such companies that are listed only on BSE and not on NSE, which explains why NSE might have a marketing strategy to temporarily trade shares that are not listed on it.

Reference: Listing Process in the Indian Stock Market | Motilal Oswal

Dreamfolks services limited( DFS) (01-11-2023)

Very transparent, clean and to the point – no manipulation or beating around the bush

Excellent Leadership !!!

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (01-11-2023)

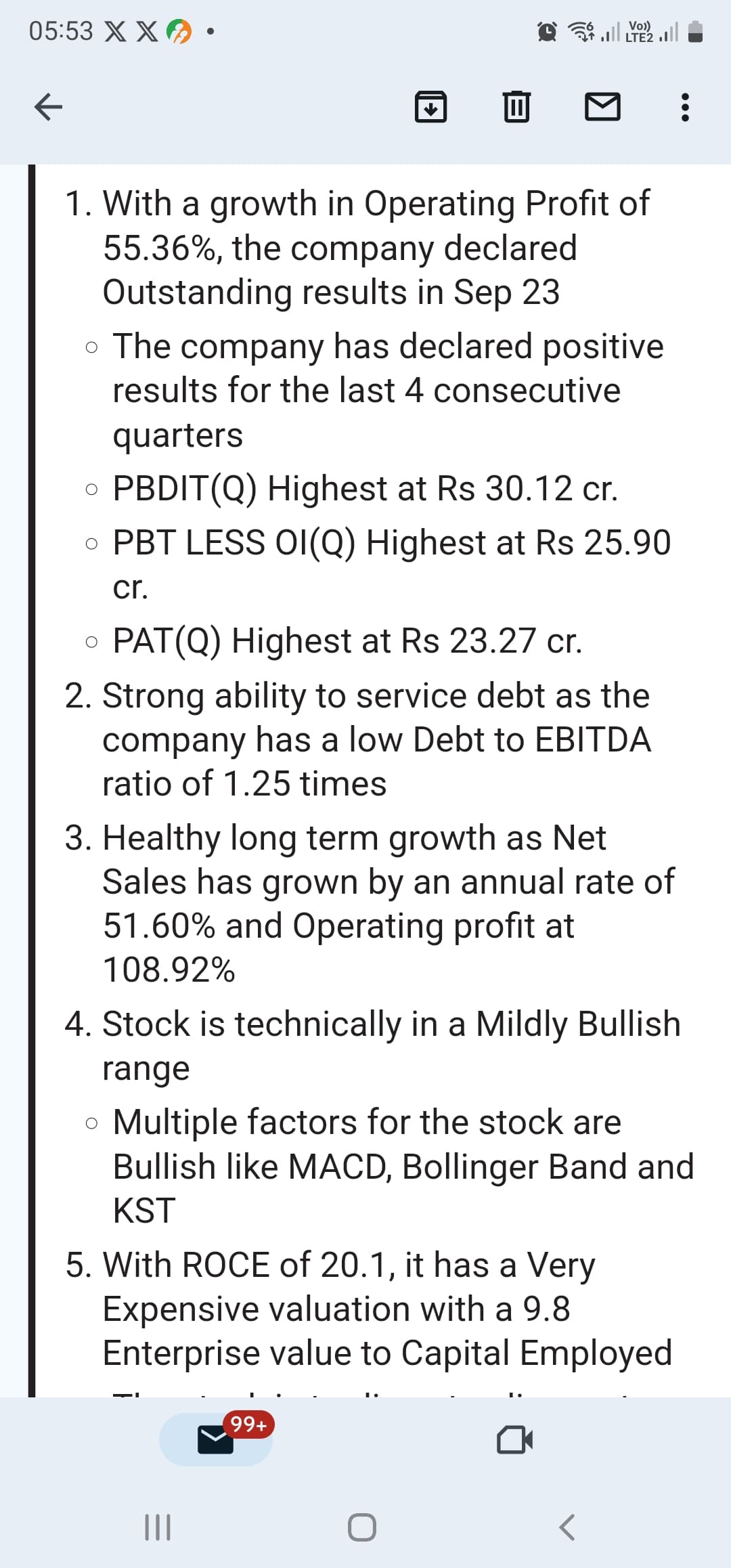

BALU FORGE DECLARES OUTSTANDING SEP 2023 RESULTS

Shiva Cement Ltd – Expanding It’s Capacity (01-11-2023)

First quarter of sales & OPM +ve!

Disc: Invested

Praveg Ltd: Play on Indian Tourism Industry! (31-10-2023)

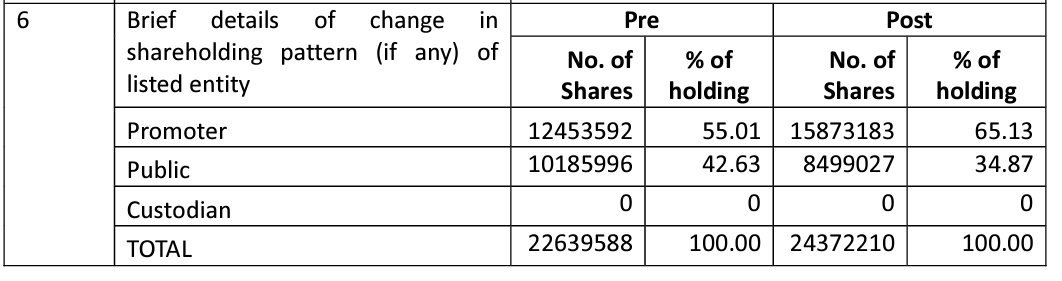

I am still trying to understand the transaction but here are my two cents. The Net worth is not representing ‘Market cap’ but the ‘Book value’ of the company. But I don’t think it makes any difference in this deal. Important point to note is the change in equity holding-

While Promoter holding has gone up by 33 lakh shares, interesting thing is that Public shareholding has gone down by 17 lakh shares too. As per my limited understanding, it should only happen if ‘Transferor’ company already had some shares of Praveg and they are now moved under ‘Promoter’ fold.

In addition, another 17 lakh shares are issued (2.43 cr post against 2.26 cr pre) which translate to an equity dilution worth roughly 90 crores at CMP of 550 INR per share. Based on remarks made by other members, I believe this is the amount Praveg is paying to the ‘Transferor’ company for buying the two properties that they own.

I don’t know yet if it bad corporate governance case, but it looks like company has not explained the deal in detail and that raises some doubts. But as we know with most small caps, they are not very good in explaining things to shareholders so I am willing to wait for more clarity to emerge.

Disc: Invested

Aarti Pharma Labs (31-10-2023)

Hi @Vinay_Garg – While the Xanthine derivative business does constitute a considerable portion, it is their API business that is the main revenue driver (more than 50% in FY23) for Aarti Pharmalabs. Furthermore, they have also recently focused on the CDMO business which I assume you are aware of. Thus it would be incorrect to label it as a consumer proxy.

Now coming to the question of whether it deserves a higher PE? I found it difficult to determine at this time. It is a stable business, no doubt. But one would think that the real area of interest from an investor’s POV is their nascent CDMO business. I will keep a close watch on how it matures and perhaps Mr. Market will too.

Disc – Not Invested (But on watchlist)

Ajanta Pharma (31-10-2023)

Company came up with a good set of nos in Q2, with sales growing by 10% and EPS by 25%. Its good to see come back to their normal EBITDA margins of 25-30% after a gap of a few quarters. A very interesting piece of commentary was their US generics business, where they are seeing much more opportunities and lower pricing erosion, leading to 20%+ growth. Concall notes below.

FY24Q2 concall

- Sales grew at 10%, Gross margin 75%, EBITDA margins ~ 28%, PAT margins ~ 19%

- Expect low teen sales growth and 26% EBITDA margins in FY24

- US:

o 28% YOY growth (1 new launch, 42 launched products, plan to launch 3-4 products in remainder)

o Growth was due to lower price erosion, market share gains in existing products and a couple of very successful new product launches

o Filed 2 ANDAs and plans to file 6-8 ANDAs during FY23

o High single digit price erosion

o Market landscape is changing, price erosion is coming down, its looking quite positive now

o Working capital requirements has not increased, instead consolidated inventory has come down to 71 days - Domestic:

o 13% YOY growth, launched 7 new products (3 was first launch in India)

o Volume growth was 6% (vs 2% for industry), Price increase: 5%, New product: 3% (Price and new product introduction was in-line with industry)

o In Q2, launched a new triple combination drug in cardiology (first time introduction) for which they undertook clinical trials. Pace of launches of such products have reduced in recent times due to tighter regulations

o Higher volume growth is due to better MR productivity and not due to geographical expansion

o Cardiac MAT growth of 9% in September 2023 (vs 11% for IPM). Growth for Ajanta was softer only in last 6-months because metXL was impacted due to NLEM price reduction

o Trade generics: 45 cr. (vs 38 cr. in Q2), 81 (vs 71 cr. in H1 FY24)

o Third fastest growing company in top 25 cos in IPM

o SGLT2 and DPP4 are being launched, along with different combinations. Since Ajanta had a late start in anti-diabetes, had some disadvantage - Emerging market (branded generics)

o Africa branded grew by 8%. Expect low to mid-teens growth in FY24

o Saw slowdown in Africa in past 4-5 months, but growth has come back recently

o Asia branded de-grew by (-8%). Saw some spillover of orders from Q2 to Q3. Expect low teen growth in FY24

o Have managed forex quite well, policy is to keep at least 50% of receivables hedged

o Launched 8 products in Q2

o Building business in countries in Central Asia, focus is changing from acute to chronic - Africa institution

o Growth of 14% YOY - CAPEX of 46 cr. in H1FY24 (full year planned capex of 150 cr. including corporate office). 60-65% capacity utilization currently. No major capex for next 18-24 months

- R&D stood at 5% of sales (scientists came down from 850+ to 800+)

- Tax rate will be 25% in FY24

- Global MR count is 4,500+ (2,800+ MRs in India)

Disclosure: Invested (position size here, sold shares in last-30 days)