This company does not pay dividend but invests in stock market and equity mutual funds! whao! why not return money to shareholders? All of us can ourselves invest in stock market and mutual funds.

Posts tagged Value Pickr

Strides_Arcolab (20-12-2015)

Not sure how fair it is to suspect FDA and/or bilateral relationship.

- Serious lapses at DRL

Source: http://www.fda.gov/ICECI/EnforcementActions/WarningLetters/2015/ucm473604.htm. - Am told Sun Halol received a lengthy Form-483 earlier, thus Warning

letter now not much of a surprise.

I think visa fee hike has lot to do with 2016 election year in U.S.

Strides_Arcolab (20-12-2015)

Unrelated but this suspicion of FDA coming after Indian firms is gaining wider prominence. Recently, it was for DRL and yday it was for Sun. Add the H1 / L1 fee hike, all the political bonhomie seems to be going nowhere

Renaissance Jewellery (20-12-2015)

Trade receivables are 237.19 Crs. Looks to be very high considering kind of business.

Does anybody have idea/details on it?

Regards

Keerthi Industries (20-12-2015)

On their website, cement capacity is written in confusing way.

On About Us page:

"Located in the Nalgonda district of Andhra Pradesh, the manufacturing facilities have an installed capacity of 297,000 MTPA cement."

http://www.keerthiindustries.com/aboutus.html

On http://www.keerthiindustries.com/cement.html

"The second phase of expansion from 900 TPD to 1600 TPD clinker and 1900 Cement grinding was successfully completed in sep 2010."

But 297,000 MTPA cement is too high figure!!!

Duke Offshore – Hidden Gem? (20-12-2015)

I believe I found the tender awarded to the company. I'll admit I got the info about the type of boat wrong - the tender is not for FICs. I didn't see any tenders for FIC issued by the DEO. Instead it is for fast passenger boats, so the question of FICs remaining idle probably does not arise. The tender mentions the minimum number as 10 boats, and similar tenders have differing quantities, so this is the most likely one.

The tender award amount is not mentioned. I'll make an educated guess based on the Earnest Money Deposit of 5.5 lakhs, because there are guidelines for the tender issuer to determine the EMD. It is around 2 to 5 percent of the estimated value (going by either Defence Procurement Manual or Ministry of Finance manual for procurement of goods), which gives me a bound of 1.10-2.75 crores as revenue. This is quite substantial IMHO, given it's effect on EPS, even if it is a one-time event.

Disclosure: invested (500 shares @ ~38)

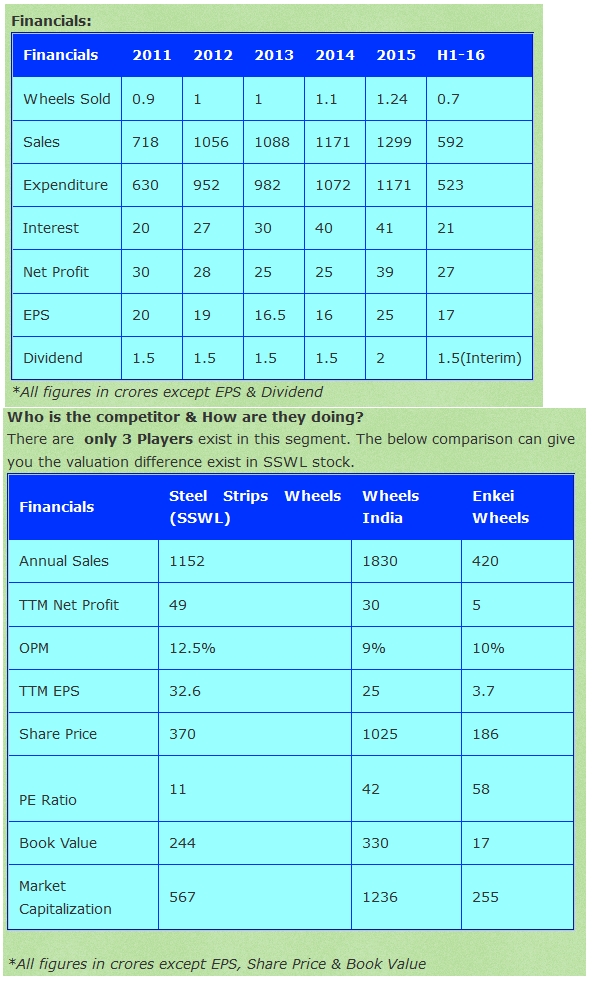

Steel Strips Wheels Limited – Attractive Valuations (20-12-2015)

Hi,

Would like to know views about Steel Strips and Wheels Limited. Why it is traded at 11 PE, Market Capitalization is 50% of Annual sales when other 2 peers trading, Wheels India @42 PE, Enkai Wheels @57 PE accordingly.

Some Inputs ..

Stock Price - 370,

Trading PE 11 Vs Industry PE 45,

EPS is increasing with margin expansion: 34 rs

2015H1 earnings 18 crores Vs 2016H1 earnings 27 crores

First Interim dividend declaration,

Higher Operating margins than peers

New allotment @640 rs, premium of 270 rs from current market price.

Tata Steel, Sumitomo(Japan), GSSC (South Korea) holds nearly 17% stake in this company.

Promoter regular purchase from Open Market

Reference: http://smallcapvaluefind.blogspot.in/

Request our VP intellectuals to share the negatives, to understand the business from my side.

Entertainment Network India Limited (ENIL) (19-12-2015)

Radio in the US is a medium where local companies dominate the advertising pie whereas in India it is the exact opposite with national companies dominating the advertising pie. With the expansion of FM licenses, this will bring in more local advertisers in to the fold.

Also advertising growth as a whole is dependent on economy growth and as an when economy picks up we will see advertising growth also coming back in. But radio has a hedge even if economy does not get back on track soon. Its rates are lower than competitive media like TV and so even in a downturn to get more bang for your ad spend companies will look towards radio as an attractive media outlet.

Disclosure: Have sold out of ENIL in last 30 days, but still interested and waiting for a decent correction to buy again.

MPS Ltd (19-12-2015)

I had a look at the Concall and also went through Management Q&A.

My question is that if budgets remain the same annually and year after year with realizations being squeezed and volumes increasing, do the two not cancel each other out. I am a bit hesitant to see where revenue growth is going to come from unless its an acquisition.

They have grown 100% with Elsevier and 40% with Macmillan but we do not know how much of a pricing cut they had to take. For quarterly results only June 2015 quarter had YOY growth of 20%. Annually too, FY 15 had revenue growth of only 11% or so.

Agreed that the penetration is low and clients are sticky, there is no threat of new player snatching away clients but unless the budget of each client grows or the company acquires new clients i.e. from among the incumbents of publishing for which it does no work currently, then growth is going to be hard to come by.

As regards having enough cash to do an acquisition and waiting for the right target valuation and complementary skills wise, would it not be better for someone like me who has no investment in MPS to actually wait for the acquisition and then decide on the merit of the investment based on how the acquisition seems at that point of time.

I thank all of you guys for providing such excellent material for us to go through in terms of MQ and BQ insights as well as the Management Q&A.

Please do let me know if my doubts do not seem valid as this is just my opinion.

Kaveri seeds company limited — kscl (19-12-2015)

Central Govt approaches CCI to probe MMB Royalty agreement.

http://www.hindustantimes.com/india/central-govt-targets-monsanto-indian-jv-for-alleged-monopoly/story-cpkCGc6rDgbw3wgovMiTTO.html